{"title":"自我建构在声誉判断中的作用:盈余管理的实验研究","authors":"Ida Nur Aeni, Supriyadi, Heri Yanto","doi":"10.1007/s13520-021-00127-w","DOIUrl":null,"url":null,"abstract":"<div><p>This study aims to investigate the role of self-construal in sharpening reputation judgment on earnings management cases. This study involves a personality variable that can provide sharper insights into individual assessments, namely self-construal. The study uses an experimental case with involved participants to judge the ethics of earnings management done by other managers (the target managers). Participants of this study consist of 109 master’s degree students majoring in accounting and management who acts as fellow managers. Participants provide ethical judgment and reputation judgment of the target managers. This study indicates that ethical judgment on earnings management behavior differs depending on the target managers’ self-construal. In addition, ethical judgment has a positive and significant effect on reputation judgment. The following analysis showed that ethical judgment mediates the effect of earnings management behavior that self-construal moderates on reputation judgment. Studies that highlight the impact of managers’ reputation engaging in earnings management are still limited. This study used a behavioral approach, especially involving self-construal, to scrutinize the behavior of individuals within the organization, which is previous studies have not yet involved that personality factor. This research’s results imply that a manager’s response to peer’s behavior is helpful to design an appropriate management control system for organizations. This study only used earnings management scenarios in order to increase earnings. Earnings management can be in the form of actions to increase or decrease earnings.</p></div>","PeriodicalId":54051,"journal":{"name":"Asian Journal of Business Ethics","volume":"10 2","pages":"183 - 204"},"PeriodicalIF":1.9000,"publicationDate":"2021-06-22","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1007/s13520-021-00127-w","citationCount":"0","resultStr":"{\"title\":\"The roles of self-construal in sharpening reputation judgment: an experimental study on earnings management\",\"authors\":\"Ida Nur Aeni, Supriyadi, Heri Yanto\",\"doi\":\"10.1007/s13520-021-00127-w\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This study aims to investigate the role of self-construal in sharpening reputation judgment on earnings management cases. This study involves a personality variable that can provide sharper insights into individual assessments, namely self-construal. The study uses an experimental case with involved participants to judge the ethics of earnings management done by other managers (the target managers). Participants of this study consist of 109 master’s degree students majoring in accounting and management who acts as fellow managers. Participants provide ethical judgment and reputation judgment of the target managers. This study indicates that ethical judgment on earnings management behavior differs depending on the target managers’ self-construal. In addition, ethical judgment has a positive and significant effect on reputation judgment. The following analysis showed that ethical judgment mediates the effect of earnings management behavior that self-construal moderates on reputation judgment. Studies that highlight the impact of managers’ reputation engaging in earnings management are still limited. This study used a behavioral approach, especially involving self-construal, to scrutinize the behavior of individuals within the organization, which is previous studies have not yet involved that personality factor. This research’s results imply that a manager’s response to peer’s behavior is helpful to design an appropriate management control system for organizations. This study only used earnings management scenarios in order to increase earnings. Earnings management can be in the form of actions to increase or decrease earnings.</p></div>\",\"PeriodicalId\":54051,\"journal\":{\"name\":\"Asian Journal of Business Ethics\",\"volume\":\"10 2\",\"pages\":\"183 - 204\"},\"PeriodicalIF\":1.9000,\"publicationDate\":\"2021-06-22\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1007/s13520-021-00127-w\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asian Journal of Business Ethics\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s13520-021-00127-w\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ETHICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asian Journal of Business Ethics","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s13520-021-00127-w","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ETHICS","Score":null,"Total":0}

The roles of self-construal in sharpening reputation judgment: an experimental study on earnings management

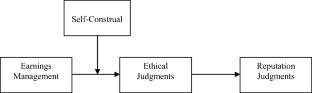

This study aims to investigate the role of self-construal in sharpening reputation judgment on earnings management cases. This study involves a personality variable that can provide sharper insights into individual assessments, namely self-construal. The study uses an experimental case with involved participants to judge the ethics of earnings management done by other managers (the target managers). Participants of this study consist of 109 master’s degree students majoring in accounting and management who acts as fellow managers. Participants provide ethical judgment and reputation judgment of the target managers. This study indicates that ethical judgment on earnings management behavior differs depending on the target managers’ self-construal. In addition, ethical judgment has a positive and significant effect on reputation judgment. The following analysis showed that ethical judgment mediates the effect of earnings management behavior that self-construal moderates on reputation judgment. Studies that highlight the impact of managers’ reputation engaging in earnings management are still limited. This study used a behavioral approach, especially involving self-construal, to scrutinize the behavior of individuals within the organization, which is previous studies have not yet involved that personality factor. This research’s results imply that a manager’s response to peer’s behavior is helpful to design an appropriate management control system for organizations. This study only used earnings management scenarios in order to increase earnings. Earnings management can be in the form of actions to increase or decrease earnings.

期刊介绍:

The Asian Journal of Business Ethics (AJBE) publishes original articles from a wide variety of methodological and disciplinary perspectives concerning ethical issues related to business in Asia, including East, Southeast and South-central Asia. Like its well-known sister publication Journal of Business Ethics, AJBE examines the moral dimensions of production, consumption, labour relations, and organizational behavior, while taking into account the unique societal and ethical perspectives of the Asian region. The term ''business'' is understood in a wide sense to include all systems involved in the exchange of goods and services, while ''ethics'' is understood as applying to all human action aimed at securing a good life. We believe that issues concerning corporate responsibility are within the scope of ethics broadly construed. Systems of production, consumption, marketing, advertising, social and economic accounting, labour relations, public relations and organizational behaviour will be analyzed from a moral or ethical point of view. The style and level of dialogue involve all who are interested in business ethics - the business community, universities, government agencies, non-government organizations and consumer groups.The AJBE viewpoint is especially relevant today, as global business initiatives bring eastern and western companies together in new and ever more complex patterns of cooperation and competition.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: