Douglas J Cumming, Andrea Martinez-Salgueiro, Robert S Reardon, Ahmed Sewaid

{"title":"新冠疫情爆发、政策应对和反弹:股权众筹和P2P与银行。","authors":"Douglas J Cumming, Andrea Martinez-Salgueiro, Robert S Reardon, Ahmed Sewaid","doi":"10.1007/s10961-021-09899-6","DOIUrl":null,"url":null,"abstract":"<p><p>Traditional intermediaries have the ability and the incentive to intertemporarily smooth outcomes. Fintechs, such as peer-to-peer (P2P) lending platforms and equity crowdfunding (ECF) platforms, enable riskier projects without regard to intertemporal smoothing. U.S. data from May 2016 to June 2020 show that COVID-19 had an adverse impact on bank consumer lending. However, counter to our expectations, ECF and P2P are much more stable, timely, and resilient in the COVID-19 crisis compared to bank consumer lending. Moreover, the data indicate that P2P lending is a leading indicator for bank consumer lending and that bank consumer lending substitutes ECF. The policy response-CARES Act-caused: (1) a significant increase in ECF volumes, (2) a substantial rebound to bank consumer lending, and iii) at best, neutralized an already-stabilized level of P2P lending.</p>","PeriodicalId":515902,"journal":{"name":"The Journal of Technology Transfer","volume":"47 6","pages":"1825-1846"},"PeriodicalIF":0.0000,"publicationDate":"2022-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8520110/pdf/","citationCount":"18","resultStr":"{\"title\":\"COVID-19 bust, policy response, and rebound: equity crowdfunding and P2P versus banks.\",\"authors\":\"Douglas J Cumming, Andrea Martinez-Salgueiro, Robert S Reardon, Ahmed Sewaid\",\"doi\":\"10.1007/s10961-021-09899-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>Traditional intermediaries have the ability and the incentive to intertemporarily smooth outcomes. Fintechs, such as peer-to-peer (P2P) lending platforms and equity crowdfunding (ECF) platforms, enable riskier projects without regard to intertemporal smoothing. U.S. data from May 2016 to June 2020 show that COVID-19 had an adverse impact on bank consumer lending. However, counter to our expectations, ECF and P2P are much more stable, timely, and resilient in the COVID-19 crisis compared to bank consumer lending. Moreover, the data indicate that P2P lending is a leading indicator for bank consumer lending and that bank consumer lending substitutes ECF. The policy response-CARES Act-caused: (1) a significant increase in ECF volumes, (2) a substantial rebound to bank consumer lending, and iii) at best, neutralized an already-stabilized level of P2P lending.</p>\",\"PeriodicalId\":515902,\"journal\":{\"name\":\"The Journal of Technology Transfer\",\"volume\":\"47 6\",\"pages\":\"1825-1846\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2022-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8520110/pdf/\",\"citationCount\":\"18\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"The Journal of Technology Transfer\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://doi.org/10.1007/s10961-021-09899-6\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2021/10/16 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"The Journal of Technology Transfer","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s10961-021-09899-6","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2021/10/16 0:00:00","PubModel":"Epub","JCR":"","JCRName":"","Score":null,"Total":0}

COVID-19 bust, policy response, and rebound: equity crowdfunding and P2P versus banks.

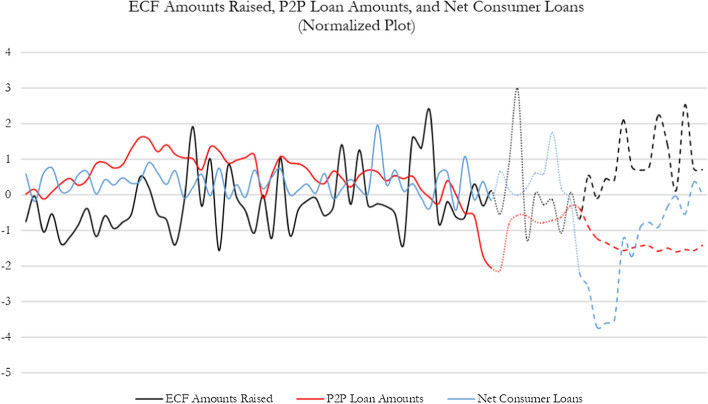

Traditional intermediaries have the ability and the incentive to intertemporarily smooth outcomes. Fintechs, such as peer-to-peer (P2P) lending platforms and equity crowdfunding (ECF) platforms, enable riskier projects without regard to intertemporal smoothing. U.S. data from May 2016 to June 2020 show that COVID-19 had an adverse impact on bank consumer lending. However, counter to our expectations, ECF and P2P are much more stable, timely, and resilient in the COVID-19 crisis compared to bank consumer lending. Moreover, the data indicate that P2P lending is a leading indicator for bank consumer lending and that bank consumer lending substitutes ECF. The policy response-CARES Act-caused: (1) a significant increase in ECF volumes, (2) a substantial rebound to bank consumer lending, and iii) at best, neutralized an already-stabilized level of P2P lending.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: