{"title":"投资者异质性和相互作用对期货市场价格发现的影响:基于动态系统和稳定性分析","authors":"Qingbin Gong, Zhe Yang, Xundi Diao","doi":"10.1007/s10479-025-06676-8","DOIUrl":null,"url":null,"abstract":"<div><p>This paper investigates the impacts of trading behaviors on price discovery in futures markets. A dynamical model with difference equations is proposed to depict the interactions of heterogenous investors and the spot-futures coevolution. The system equilibrium and its stability conditions are mathematically analyzed. In the equilibrium, the futures price and the spot price converge to the fundamental value simultaneously. Stability conditions are necessary for the convergence process as well as the price discovery function. To ensure stability conditions, factors such as investor bounded rationality, risk appetites and market liquidity need to satisfy specific relationships. As the findings show, the arbitrage is not always beneficial to market stability and price discovery. It may increase price fluctuations in some cases. If investors have high degree of rationality, they tend to switch trading strategies with high intensity, which may destabilize the market. The simulations suggest the occurrence of complicated dynamics when stability conditions are violated. It provides theoretical insights into complicated phenomena in futures markets.</p></div>","PeriodicalId":8215,"journal":{"name":"Annals of Operations Research","volume":"350 3","pages":"957 - 977"},"PeriodicalIF":4.5000,"publicationDate":"2025-05-27","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Impacts of investor heterogeneity and interactions on price discovery in futures markets: Based on dynamical system and stability analysis\",\"authors\":\"Qingbin Gong, Zhe Yang, Xundi Diao\",\"doi\":\"10.1007/s10479-025-06676-8\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This paper investigates the impacts of trading behaviors on price discovery in futures markets. A dynamical model with difference equations is proposed to depict the interactions of heterogenous investors and the spot-futures coevolution. The system equilibrium and its stability conditions are mathematically analyzed. In the equilibrium, the futures price and the spot price converge to the fundamental value simultaneously. Stability conditions are necessary for the convergence process as well as the price discovery function. To ensure stability conditions, factors such as investor bounded rationality, risk appetites and market liquidity need to satisfy specific relationships. As the findings show, the arbitrage is not always beneficial to market stability and price discovery. It may increase price fluctuations in some cases. If investors have high degree of rationality, they tend to switch trading strategies with high intensity, which may destabilize the market. The simulations suggest the occurrence of complicated dynamics when stability conditions are violated. It provides theoretical insights into complicated phenomena in futures markets.</p></div>\",\"PeriodicalId\":8215,\"journal\":{\"name\":\"Annals of Operations Research\",\"volume\":\"350 3\",\"pages\":\"957 - 977\"},\"PeriodicalIF\":4.5000,\"publicationDate\":\"2025-05-27\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Annals of Operations Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10479-025-06676-8\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"OPERATIONS RESEARCH & MANAGEMENT SCIENCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Operations Research","FirstCategoryId":"91","ListUrlMain":"https://link.springer.com/article/10.1007/s10479-025-06676-8","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"OPERATIONS RESEARCH & MANAGEMENT SCIENCE","Score":null,"Total":0}

Impacts of investor heterogeneity and interactions on price discovery in futures markets: Based on dynamical system and stability analysis

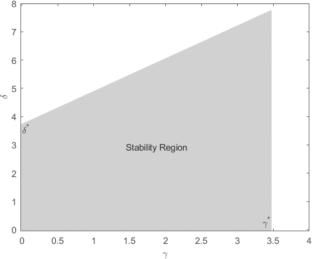

This paper investigates the impacts of trading behaviors on price discovery in futures markets. A dynamical model with difference equations is proposed to depict the interactions of heterogenous investors and the spot-futures coevolution. The system equilibrium and its stability conditions are mathematically analyzed. In the equilibrium, the futures price and the spot price converge to the fundamental value simultaneously. Stability conditions are necessary for the convergence process as well as the price discovery function. To ensure stability conditions, factors such as investor bounded rationality, risk appetites and market liquidity need to satisfy specific relationships. As the findings show, the arbitrage is not always beneficial to market stability and price discovery. It may increase price fluctuations in some cases. If investors have high degree of rationality, they tend to switch trading strategies with high intensity, which may destabilize the market. The simulations suggest the occurrence of complicated dynamics when stability conditions are violated. It provides theoretical insights into complicated phenomena in futures markets.

期刊介绍:

The Annals of Operations Research publishes peer-reviewed original articles dealing with key aspects of operations research, including theory, practice, and computation. The journal publishes full-length research articles, short notes, expositions and surveys, reports on computational studies, and case studies that present new and innovative practical applications.

In addition to regular issues, the journal publishes periodic special volumes that focus on defined fields of operations research, ranging from the highly theoretical to the algorithmic and the applied. These volumes have one or more Guest Editors who are responsible for collecting the papers and overseeing the refereeing process.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: