保形预测用于日前和实时均衡市场的电价预测

IF 9.6

Q1 COMPUTER SCIENCE, ARTIFICIAL INTELLIGENCE

引用次数: 0

摘要

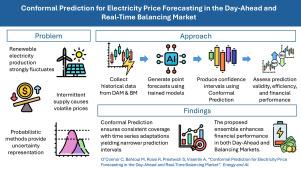

将可再生能源纳入电力市场对价格稳定构成重大挑战,并增加了市场运作的复杂性。准确可靠的电价预测对于有效的市场参与至关重要,因为价格动态的预测可能更具挑战性。概率预测通过预测区间有效地量化电价的内在不确定性,为市场参与者提供更好的决策支持。本研究探讨了使用共形预测(CP)技术增强概率价格预测,特别是集成批预测区间和顺序预测共形推理。这些方法提供了精确可靠的预测区间,在有效性度量上优于传统模型。我们提出了一种集成方法,将分位数回归模型的效率与时间序列适应CP技术的鲁棒覆盖特性相结合。该集合提供了较窄的预测间隔和高覆盖率,从而导致更可靠和准确的预测。我们通过应用于电池存储系统的模拟交易算法进一步评估CP技术的实际意义。综合方法表明,在日前市场和平衡市场中,能源交易的财务回报都有所提高,突出了其对市场参与者的实际好处。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Conformal Prediction for electricity price forecasting in the day-ahead and real-time balancing market

The integration of renewable energy into electricity markets poses significant challenges to price stability and increases the complexity of market operations. Accurate and reliable electricity price forecasting is crucial for effective market participation, where price dynamics can be significantly more challenging to predict. Probabilistic forecasting, through prediction intervals, efficiently quantifies the inherent uncertainties in electricity prices, supporting better decision-making for market participants. This study explores the enhancement of probabilistic price prediction using Conformal Prediction (CP) techniques, specifically Ensemble Batch Prediction Intervals and Sequential Predictive Conformal Inference. These methods provide precise and reliable prediction intervals, outperforming traditional models in validity metrics. We propose an ensemble approach that combines the efficiency of quantile regression models with the robust coverage properties of time series adapted CP techniques. This ensemble delivers both narrow prediction intervals and high coverage, leading to more reliable and accurate forecasts. We further evaluate the practical implications of CP techniques through a simulated trading algorithm applied to a battery storage system. The ensemble approach demonstrates improved financial returns in energy trading in both the Day-Ahead and Balancing Markets, highlighting its practical benefits for market participants.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Energy and AI

Engineering-Engineering (miscellaneous)

CiteScore

16.50

自引率

0.00%

发文量

64

审稿时长

56 days

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: