{"title":"从中国企业层面数据估算往返FDI","authors":"Zeyi Qian, Junfu Zhang, Qiangyuan Chen","doi":"10.1002/ise3.102","DOIUrl":null,"url":null,"abstract":"<p>When capital leaves a country and then flows back as foreign direct investment (FDI), we call it round-tripping FDI. It is widely suspected that China's official FDI statistics contain a substantial amount of round-tripping FDI. However, it is difficult to quantify the round-tripping FDI due to the lack of data. In this paper, we propose two methods to identify round-tripping FDI. The first one tracks capital flows at the firm level. If a firm in China invests in a foreign firm and this foreign firm makes an investment back to China shortly after, then we consider this investment to China as round-tripping FDI. Our second measure of round-tripping FDI adds to the first measure by including investments in China made by Chinese investors registered in tax havens. The first estimate of round-tripping FDI accounts for up to 3% of China's total FDI from 1999 to 2015, whereas the second estimate accounts for up to 70% in the period. Our firm-level analysis shows that industrial firms facing higher tax burdens are more likely to make round-tripping FDI. We also show that at the city level, adjusted FDI statistics by subtracting the estimated round-tripping FDI are better predictors of imports and exports. Finally, we show that provinces receiving higher shares of round-tripping FDI are more likely to be punished for illegal financial activities. Taken together, these findings suggest that our measures of round-tripping FDI, although noisy, are indicative of real transactions.</p>","PeriodicalId":29662,"journal":{"name":"International Studies of Economics","volume":"20 2","pages":"138-152"},"PeriodicalIF":0.5000,"publicationDate":"2024-11-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ise3.102","citationCount":"0","resultStr":"{\"title\":\"Estimating Round-Tripping FDI from Firm-Level Data in China\",\"authors\":\"Zeyi Qian, Junfu Zhang, Qiangyuan Chen\",\"doi\":\"10.1002/ise3.102\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>When capital leaves a country and then flows back as foreign direct investment (FDI), we call it round-tripping FDI. It is widely suspected that China's official FDI statistics contain a substantial amount of round-tripping FDI. However, it is difficult to quantify the round-tripping FDI due to the lack of data. In this paper, we propose two methods to identify round-tripping FDI. The first one tracks capital flows at the firm level. If a firm in China invests in a foreign firm and this foreign firm makes an investment back to China shortly after, then we consider this investment to China as round-tripping FDI. Our second measure of round-tripping FDI adds to the first measure by including investments in China made by Chinese investors registered in tax havens. The first estimate of round-tripping FDI accounts for up to 3% of China's total FDI from 1999 to 2015, whereas the second estimate accounts for up to 70% in the period. Our firm-level analysis shows that industrial firms facing higher tax burdens are more likely to make round-tripping FDI. We also show that at the city level, adjusted FDI statistics by subtracting the estimated round-tripping FDI are better predictors of imports and exports. Finally, we show that provinces receiving higher shares of round-tripping FDI are more likely to be punished for illegal financial activities. Taken together, these findings suggest that our measures of round-tripping FDI, although noisy, are indicative of real transactions.</p>\",\"PeriodicalId\":29662,\"journal\":{\"name\":\"International Studies of Economics\",\"volume\":\"20 2\",\"pages\":\"138-152\"},\"PeriodicalIF\":0.5000,\"publicationDate\":\"2024-11-17\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ise3.102\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Studies of Economics\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/ise3.102\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q4\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Studies of Economics","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/ise3.102","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"ECONOMICS","Score":null,"Total":0}

Estimating Round-Tripping FDI from Firm-Level Data in China

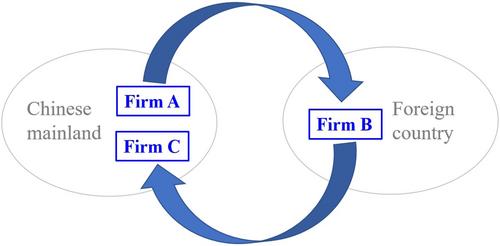

When capital leaves a country and then flows back as foreign direct investment (FDI), we call it round-tripping FDI. It is widely suspected that China's official FDI statistics contain a substantial amount of round-tripping FDI. However, it is difficult to quantify the round-tripping FDI due to the lack of data. In this paper, we propose two methods to identify round-tripping FDI. The first one tracks capital flows at the firm level. If a firm in China invests in a foreign firm and this foreign firm makes an investment back to China shortly after, then we consider this investment to China as round-tripping FDI. Our second measure of round-tripping FDI adds to the first measure by including investments in China made by Chinese investors registered in tax havens. The first estimate of round-tripping FDI accounts for up to 3% of China's total FDI from 1999 to 2015, whereas the second estimate accounts for up to 70% in the period. Our firm-level analysis shows that industrial firms facing higher tax burdens are more likely to make round-tripping FDI. We also show that at the city level, adjusted FDI statistics by subtracting the estimated round-tripping FDI are better predictors of imports and exports. Finally, we show that provinces receiving higher shares of round-tripping FDI are more likely to be punished for illegal financial activities. Taken together, these findings suggest that our measures of round-tripping FDI, although noisy, are indicative of real transactions.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: