Harold Edward Groce, Dennis Wayne Ashley, Joe Sam Robinson

{"title":"减少国家创伤死亡率对终身个人收入和国家税收收入的经济影响。","authors":"Harold Edward Groce, Dennis Wayne Ashley, Joe Sam Robinson","doi":"10.1136/tsaco-2024-001698","DOIUrl":null,"url":null,"abstract":"<p><strong>Background: </strong>In 2003, Georgia's trauma mortality rate was 16% above the national average. By 2020, mortality had decreased to 6% below the national average, translating to 1,803 fewer lives lost than might have been expected if 2003 trends had continued. The purpose of this study is to assess the state-wide economic impact of reduced mortality and disability measured in the amount of lifetime personal income and state tax revenue preserved.</p><p><strong>Methods: </strong>Using the Centers for Disease Control and Prevention's Web-Based Injury Statistics Query and Reporting System database, state/national trauma mortality rates for 2020 were compared with 2003. Years of potential life lost (YPLL) for trauma victims up to 65 were calculated for the same time period. Rates of severe disability were calculated based on the average results of four studies (1992-2022) and used to estimate additional YPLL. The per-capita personal income for Georgia and the average percent of personal income paid in state taxes were calculated using federal and state data. These numbers were then multiplied by state YPLL rates to calculate lifetime personal income and state tax revenue lost due to trauma.</p><p><strong>Results: </strong>$4.3 billion in lifetime personal income preserved (averted death $1.3 billion and averted disability $2.9 billion). $508 million in lifetime tax revenue preserved (averted death $158 million and averted disability $349 million).</p><p><strong>Conclusions: </strong>Reduced state trauma mortality and disability substantially benefitted lifetime potential personal income and lifetime potential state and local tax revenue. This study provides states with a template to evaluate the economic impact of reducing trauma mortality. While the causes of reduced mortality are manifold, anything that can be done to reduce trauma mortality is a worthwhile investment. Accordingly, state trauma system funding should be considered an <i>investment</i>, not a cost.</p><p><strong>Level of evidence: </strong>Economic and value-based evaluations, Level III.</p>","PeriodicalId":23307,"journal":{"name":"Trauma Surgery & Acute Care Open","volume":"10 3","pages":"e001698"},"PeriodicalIF":2.2000,"publicationDate":"2025-07-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12265832/pdf/","citationCount":"0","resultStr":"{\"title\":\"Economic impact of reduced state trauma mortality on lifetime personal income and state tax revenue.\",\"authors\":\"Harold Edward Groce, Dennis Wayne Ashley, Joe Sam Robinson\",\"doi\":\"10.1136/tsaco-2024-001698\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><strong>Background: </strong>In 2003, Georgia's trauma mortality rate was 16% above the national average. By 2020, mortality had decreased to 6% below the national average, translating to 1,803 fewer lives lost than might have been expected if 2003 trends had continued. The purpose of this study is to assess the state-wide economic impact of reduced mortality and disability measured in the amount of lifetime personal income and state tax revenue preserved.</p><p><strong>Methods: </strong>Using the Centers for Disease Control and Prevention's Web-Based Injury Statistics Query and Reporting System database, state/national trauma mortality rates for 2020 were compared with 2003. Years of potential life lost (YPLL) for trauma victims up to 65 were calculated for the same time period. Rates of severe disability were calculated based on the average results of four studies (1992-2022) and used to estimate additional YPLL. The per-capita personal income for Georgia and the average percent of personal income paid in state taxes were calculated using federal and state data. These numbers were then multiplied by state YPLL rates to calculate lifetime personal income and state tax revenue lost due to trauma.</p><p><strong>Results: </strong>$4.3 billion in lifetime personal income preserved (averted death $1.3 billion and averted disability $2.9 billion). $508 million in lifetime tax revenue preserved (averted death $158 million and averted disability $349 million).</p><p><strong>Conclusions: </strong>Reduced state trauma mortality and disability substantially benefitted lifetime potential personal income and lifetime potential state and local tax revenue. This study provides states with a template to evaluate the economic impact of reducing trauma mortality. While the causes of reduced mortality are manifold, anything that can be done to reduce trauma mortality is a worthwhile investment. Accordingly, state trauma system funding should be considered an <i>investment</i>, not a cost.</p><p><strong>Level of evidence: </strong>Economic and value-based evaluations, Level III.</p>\",\"PeriodicalId\":23307,\"journal\":{\"name\":\"Trauma Surgery & Acute Care Open\",\"volume\":\"10 3\",\"pages\":\"e001698\"},\"PeriodicalIF\":2.2000,\"publicationDate\":\"2025-07-15\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12265832/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Trauma Surgery & Acute Care Open\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1136/tsaco-2024-001698\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2025/1/1 0:00:00\",\"PubModel\":\"eCollection\",\"JCR\":\"Q3\",\"JCRName\":\"CRITICAL CARE MEDICINE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Trauma Surgery & Acute Care Open","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1136/tsaco-2024-001698","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2025/1/1 0:00:00","PubModel":"eCollection","JCR":"Q3","JCRName":"CRITICAL CARE MEDICINE","Score":null,"Total":0}

Economic impact of reduced state trauma mortality on lifetime personal income and state tax revenue.

Background: In 2003, Georgia's trauma mortality rate was 16% above the national average. By 2020, mortality had decreased to 6% below the national average, translating to 1,803 fewer lives lost than might have been expected if 2003 trends had continued. The purpose of this study is to assess the state-wide economic impact of reduced mortality and disability measured in the amount of lifetime personal income and state tax revenue preserved.

Methods: Using the Centers for Disease Control and Prevention's Web-Based Injury Statistics Query and Reporting System database, state/national trauma mortality rates for 2020 were compared with 2003. Years of potential life lost (YPLL) for trauma victims up to 65 were calculated for the same time period. Rates of severe disability were calculated based on the average results of four studies (1992-2022) and used to estimate additional YPLL. The per-capita personal income for Georgia and the average percent of personal income paid in state taxes were calculated using federal and state data. These numbers were then multiplied by state YPLL rates to calculate lifetime personal income and state tax revenue lost due to trauma.

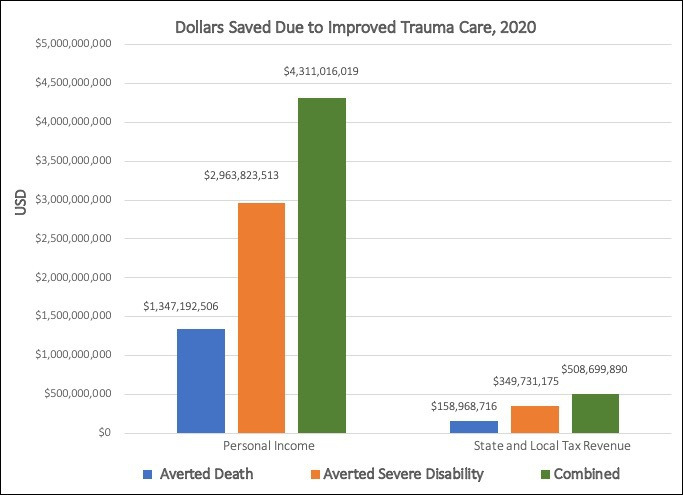

Results: $4.3 billion in lifetime personal income preserved (averted death $1.3 billion and averted disability $2.9 billion). $508 million in lifetime tax revenue preserved (averted death $158 million and averted disability $349 million).

Conclusions: Reduced state trauma mortality and disability substantially benefitted lifetime potential personal income and lifetime potential state and local tax revenue. This study provides states with a template to evaluate the economic impact of reducing trauma mortality. While the causes of reduced mortality are manifold, anything that can be done to reduce trauma mortality is a worthwhile investment. Accordingly, state trauma system funding should be considered an investment, not a cost.

Level of evidence: Economic and value-based evaluations, Level III.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: