{"title":"医院预算制度对医师行政人员预算认知意识及医疗决策的影响。","authors":"Wen-Hsin Huang, Cheng-Tsung Lu","doi":"10.1186/s12962-025-00629-5","DOIUrl":null,"url":null,"abstract":"<p><strong>Background and objective: </strong>This study adopts social cognitive theory to comprehensively explore how hospital budgeting systems influence physician-executives' budget cognitions (budget usefulness, relevance, and cost control consciousness) and how these cognitions subsequently affect medical decision-making within the context of a global budget payment system.</p><p><strong>Methods: </strong>Data was collected through questionnaire survey method. Before distributing the formal questionnaire, researchers interviewed the hospital director to discuss the questionnaire items that matched the current medical organization situation. Subsequently, the formal questionnaire was mailed directly to physician-executives in teaching hospitals (National Health Insurance contracted). We used the Structural Equation Model to examine the causal relationships among research variables.</p><p><strong>Results: </strong>Hospital budgeting systems with communication, control, and forecasting characteristics positively impact physician-executives' cognitions of the relevance and usefulness of budget information. Both physician-executives' cognition of budget quality (relevance and usefulness) and budgeting systems characteristics positively impact the establishment of physician-executives' cost control consciousness. This heightened cost control consciousness significantly influences physician-executives' subsequent medical decisions. This study confirmed that when considerations of limited medical resources and costs under a global budget payment system, physician-executives tend to adopt cost control medical decision-making behaviors.</p><p><strong>Conclusions: </strong>The empirical findings of this study indicate that when physician-executives possess cost control consciousness or budget-related cognitive concepts, it may influence their adoption of cost control medical decisions. Therefore, in a highly competitive medical environment with limited resources under a global budget payment system, striking a balance between the rational allocation of budgetary resources and ensuring adequate medical care for the public becomes a critical issue. These findings provide valuable insights for both the medical industry and government in formulating future health insurance policies. Moreover, they offer hospitals useful references for designing and implementing effective budgeting systems.</p>","PeriodicalId":47054,"journal":{"name":"Cost Effectiveness and Resource Allocation","volume":"23 1","pages":"22"},"PeriodicalIF":2.5000,"publicationDate":"2025-05-21","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12093828/pdf/","citationCount":"0","resultStr":"{\"title\":\"The effect of hospital budgeting system on physician-executives' budget cognitive consciousness and medical decision making.\",\"authors\":\"Wen-Hsin Huang, Cheng-Tsung Lu\",\"doi\":\"10.1186/s12962-025-00629-5\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><strong>Background and objective: </strong>This study adopts social cognitive theory to comprehensively explore how hospital budgeting systems influence physician-executives' budget cognitions (budget usefulness, relevance, and cost control consciousness) and how these cognitions subsequently affect medical decision-making within the context of a global budget payment system.</p><p><strong>Methods: </strong>Data was collected through questionnaire survey method. Before distributing the formal questionnaire, researchers interviewed the hospital director to discuss the questionnaire items that matched the current medical organization situation. Subsequently, the formal questionnaire was mailed directly to physician-executives in teaching hospitals (National Health Insurance contracted). We used the Structural Equation Model to examine the causal relationships among research variables.</p><p><strong>Results: </strong>Hospital budgeting systems with communication, control, and forecasting characteristics positively impact physician-executives' cognitions of the relevance and usefulness of budget information. Both physician-executives' cognition of budget quality (relevance and usefulness) and budgeting systems characteristics positively impact the establishment of physician-executives' cost control consciousness. This heightened cost control consciousness significantly influences physician-executives' subsequent medical decisions. This study confirmed that when considerations of limited medical resources and costs under a global budget payment system, physician-executives tend to adopt cost control medical decision-making behaviors.</p><p><strong>Conclusions: </strong>The empirical findings of this study indicate that when physician-executives possess cost control consciousness or budget-related cognitive concepts, it may influence their adoption of cost control medical decisions. Therefore, in a highly competitive medical environment with limited resources under a global budget payment system, striking a balance between the rational allocation of budgetary resources and ensuring adequate medical care for the public becomes a critical issue. These findings provide valuable insights for both the medical industry and government in formulating future health insurance policies. Moreover, they offer hospitals useful references for designing and implementing effective budgeting systems.</p>\",\"PeriodicalId\":47054,\"journal\":{\"name\":\"Cost Effectiveness and Resource Allocation\",\"volume\":\"23 1\",\"pages\":\"22\"},\"PeriodicalIF\":2.5000,\"publicationDate\":\"2025-05-21\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12093828/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Cost Effectiveness and Resource Allocation\",\"FirstCategoryId\":\"3\",\"ListUrlMain\":\"https://doi.org/10.1186/s12962-025-00629-5\",\"RegionNum\":4,\"RegionCategory\":\"医学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"HEALTH POLICY & SERVICES\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Cost Effectiveness and Resource Allocation","FirstCategoryId":"3","ListUrlMain":"https://doi.org/10.1186/s12962-025-00629-5","RegionNum":4,"RegionCategory":"医学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"HEALTH POLICY & SERVICES","Score":null,"Total":0}

The effect of hospital budgeting system on physician-executives' budget cognitive consciousness and medical decision making.

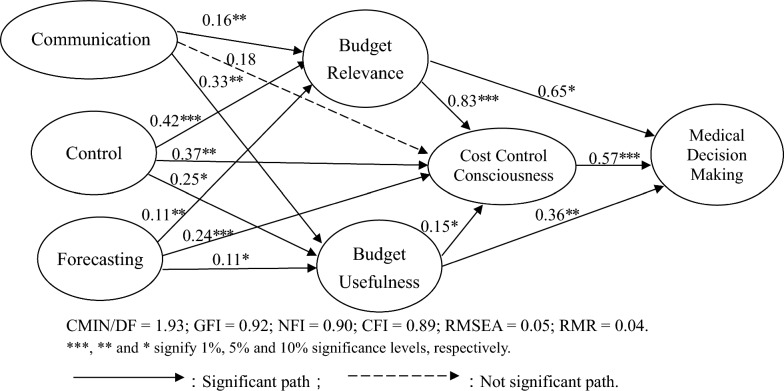

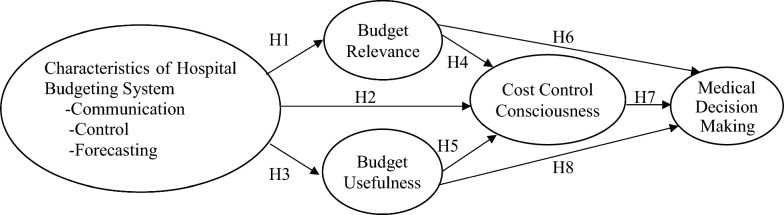

Background and objective: This study adopts social cognitive theory to comprehensively explore how hospital budgeting systems influence physician-executives' budget cognitions (budget usefulness, relevance, and cost control consciousness) and how these cognitions subsequently affect medical decision-making within the context of a global budget payment system.

Methods: Data was collected through questionnaire survey method. Before distributing the formal questionnaire, researchers interviewed the hospital director to discuss the questionnaire items that matched the current medical organization situation. Subsequently, the formal questionnaire was mailed directly to physician-executives in teaching hospitals (National Health Insurance contracted). We used the Structural Equation Model to examine the causal relationships among research variables.

Results: Hospital budgeting systems with communication, control, and forecasting characteristics positively impact physician-executives' cognitions of the relevance and usefulness of budget information. Both physician-executives' cognition of budget quality (relevance and usefulness) and budgeting systems characteristics positively impact the establishment of physician-executives' cost control consciousness. This heightened cost control consciousness significantly influences physician-executives' subsequent medical decisions. This study confirmed that when considerations of limited medical resources and costs under a global budget payment system, physician-executives tend to adopt cost control medical decision-making behaviors.

Conclusions: The empirical findings of this study indicate that when physician-executives possess cost control consciousness or budget-related cognitive concepts, it may influence their adoption of cost control medical decisions. Therefore, in a highly competitive medical environment with limited resources under a global budget payment system, striking a balance between the rational allocation of budgetary resources and ensuring adequate medical care for the public becomes a critical issue. These findings provide valuable insights for both the medical industry and government in formulating future health insurance policies. Moreover, they offer hospitals useful references for designing and implementing effective budgeting systems.

期刊介绍:

Cost Effectiveness and Resource Allocation is an Open Access, peer-reviewed, online journal that considers manuscripts on all aspects of cost-effectiveness analysis, including conceptual or methodological work, economic evaluations, and policy analysis related to resource allocation at a national or international level. Cost Effectiveness and Resource Allocation is aimed at health economists, health services researchers, and policy-makers with an interest in enhancing the flow and transfer of knowledge relating to efficiency in the health sector. Manuscripts are encouraged from researchers based in low- and middle-income countries, with a view to increasing the international economic evidence base for health.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: