{"title":"老问题的新预测方法:预测 147 年的系统性金融危机","authors":"Emile du Plessis, Ulrich Fritsche","doi":"10.1002/for.3184","DOIUrl":null,"url":null,"abstract":"<p>This paper develops new forecasting methods for an old and ongoing problem by employing 13 machine learning algorithms to study 147 years of systemic financial crises across 17 countries. Findings suggest that fixed capital formation is the most important variable. GDP per capita and consumer inflation have increased in prominence whereas debt-to-GDP, stock market, and consumption were dominant at the turn of the 20th century. A lag structure and rolling window both improve on optimized contemporaneous and individual country formats. Through a lag structure, banking sector predictors on average describe 28% of the variation in crisis prevalence, the real sector 64%, and the external sector 8%. Nearly half of all algorithms reach peak performance through a lag structure. As measured through AUC, \n<span></span><math>\n <msub>\n <mi>F</mi>\n <mn>1</mn>\n </msub></math> and Brier scores, top-performing machine learning methods consistently produce high accuracy rates, with both random forests and gradient boosting in front with 77% correct forecasts, and consistently outperform traditional regression algorithms. Learning from other countries improves predictive strength, and non-linear models generally deliver higher accuracy rates than linear models. Algorithms retaining all variables perform better than those minimizing the influence of variables.</p>","PeriodicalId":47835,"journal":{"name":"Journal of Forecasting","volume":"44 1","pages":"3-40"},"PeriodicalIF":3.4000,"publicationDate":"2024-08-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3184","citationCount":"0","resultStr":"{\"title\":\"New forecasting methods for an old problem: Predicting 147 years of systemic financial crises\",\"authors\":\"Emile du Plessis, Ulrich Fritsche\",\"doi\":\"10.1002/for.3184\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper develops new forecasting methods for an old and ongoing problem by employing 13 machine learning algorithms to study 147 years of systemic financial crises across 17 countries. Findings suggest that fixed capital formation is the most important variable. GDP per capita and consumer inflation have increased in prominence whereas debt-to-GDP, stock market, and consumption were dominant at the turn of the 20th century. A lag structure and rolling window both improve on optimized contemporaneous and individual country formats. Through a lag structure, banking sector predictors on average describe 28% of the variation in crisis prevalence, the real sector 64%, and the external sector 8%. Nearly half of all algorithms reach peak performance through a lag structure. As measured through AUC, \\n<span></span><math>\\n <msub>\\n <mi>F</mi>\\n <mn>1</mn>\\n </msub></math> and Brier scores, top-performing machine learning methods consistently produce high accuracy rates, with both random forests and gradient boosting in front with 77% correct forecasts, and consistently outperform traditional regression algorithms. Learning from other countries improves predictive strength, and non-linear models generally deliver higher accuracy rates than linear models. Algorithms retaining all variables perform better than those minimizing the influence of variables.</p>\",\"PeriodicalId\":47835,\"journal\":{\"name\":\"Journal of Forecasting\",\"volume\":\"44 1\",\"pages\":\"3-40\"},\"PeriodicalIF\":3.4000,\"publicationDate\":\"2024-08-07\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3184\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Forecasting\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/for.3184\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Forecasting","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/for.3184","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

New forecasting methods for an old problem: Predicting 147 years of systemic financial crises

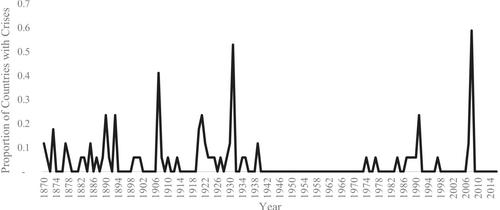

This paper develops new forecasting methods for an old and ongoing problem by employing 13 machine learning algorithms to study 147 years of systemic financial crises across 17 countries. Findings suggest that fixed capital formation is the most important variable. GDP per capita and consumer inflation have increased in prominence whereas debt-to-GDP, stock market, and consumption were dominant at the turn of the 20th century. A lag structure and rolling window both improve on optimized contemporaneous and individual country formats. Through a lag structure, banking sector predictors on average describe 28% of the variation in crisis prevalence, the real sector 64%, and the external sector 8%. Nearly half of all algorithms reach peak performance through a lag structure. As measured through AUC,

and Brier scores, top-performing machine learning methods consistently produce high accuracy rates, with both random forests and gradient boosting in front with 77% correct forecasts, and consistently outperform traditional regression algorithms. Learning from other countries improves predictive strength, and non-linear models generally deliver higher accuracy rates than linear models. Algorithms retaining all variables perform better than those minimizing the influence of variables.

期刊介绍:

The Journal of Forecasting is an international journal that publishes refereed papers on forecasting. It is multidisciplinary, welcoming papers dealing with any aspect of forecasting: theoretical, practical, computational and methodological. A broad interpretation of the topic is taken with approaches from various subject areas, such as statistics, economics, psychology, systems engineering and social sciences, all encouraged. Furthermore, the Journal welcomes a wide diversity of applications in such fields as business, government, technology and the environment. Of particular interest are papers dealing with modelling issues and the relationship of forecasting systems to decision-making processes.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: