{"title":"利用量子条件生成对抗网络和振幅估计进行碳市场风险估计","authors":"Xiyuan Zhou, Huan Zhao, Yuji Cao, Xiang Fei, Gaoqi Liang, Junhua Zhao","doi":"10.1049/enc2.12122","DOIUrl":null,"url":null,"abstract":"<p>Accurately and efficiently estimating the carbon market risk is paramount for ensuring financial stability, promoting environmental sustainability, and facilitating informed decision-making. Although classical risk estimation methods are extensively utilized, the implicit pre-assumptions regarding distribution are predominantly contained and challenging to balance accuracy and computational efficiency. A quantum computing-based carbon market risk estimation framework is proposed to address this problem with the quantum conditional generative adversarial network-quantum amplitude estimation (QCGAN-QAE) algorithm. Specifically, quantum conditional generative adversarial network (QCGAN) is employed to simulate the future distribution of the generated return rate, whereas quantum amplitude estimation (QAE) is employed to measure the distribution. Moreover, the quantum circuit of the QCGAN improved by reordering the data interaction layer and data simulation layer is coupled with the introduction of the quantum fully connected layer. The binary search method is incorporated into the QAE to bolster the computational efficiency. The simulation results based on the European Union Emissions Trading System reveals that the proposed framework markedly enhances the efficiency and precision of value-at-risk and conditional value-at-risk compared to original methods.</p>","PeriodicalId":100467,"journal":{"name":"Energy Conversion and Economics","volume":"5 4","pages":"193-210"},"PeriodicalIF":0.0000,"publicationDate":"2024-08-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1049/enc2.12122","citationCount":"0","resultStr":"{\"title\":\"Carbon market risk estimation using quantum conditional generative adversarial network and amplitude estimation\",\"authors\":\"Xiyuan Zhou, Huan Zhao, Yuji Cao, Xiang Fei, Gaoqi Liang, Junhua Zhao\",\"doi\":\"10.1049/enc2.12122\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Accurately and efficiently estimating the carbon market risk is paramount for ensuring financial stability, promoting environmental sustainability, and facilitating informed decision-making. Although classical risk estimation methods are extensively utilized, the implicit pre-assumptions regarding distribution are predominantly contained and challenging to balance accuracy and computational efficiency. A quantum computing-based carbon market risk estimation framework is proposed to address this problem with the quantum conditional generative adversarial network-quantum amplitude estimation (QCGAN-QAE) algorithm. Specifically, quantum conditional generative adversarial network (QCGAN) is employed to simulate the future distribution of the generated return rate, whereas quantum amplitude estimation (QAE) is employed to measure the distribution. Moreover, the quantum circuit of the QCGAN improved by reordering the data interaction layer and data simulation layer is coupled with the introduction of the quantum fully connected layer. The binary search method is incorporated into the QAE to bolster the computational efficiency. The simulation results based on the European Union Emissions Trading System reveals that the proposed framework markedly enhances the efficiency and precision of value-at-risk and conditional value-at-risk compared to original methods.</p>\",\"PeriodicalId\":100467,\"journal\":{\"name\":\"Energy Conversion and Economics\",\"volume\":\"5 4\",\"pages\":\"193-210\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2024-08-08\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1049/enc2.12122\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Energy Conversion and Economics\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://ietresearch.onlinelibrary.wiley.com/doi/10.1049/enc2.12122\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Energy Conversion and Economics","FirstCategoryId":"1085","ListUrlMain":"https://ietresearch.onlinelibrary.wiley.com/doi/10.1049/enc2.12122","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

Carbon market risk estimation using quantum conditional generative adversarial network and amplitude estimation

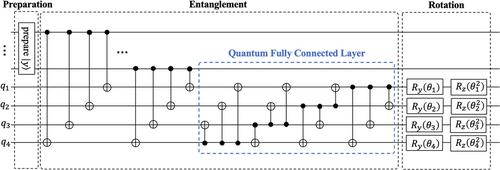

Accurately and efficiently estimating the carbon market risk is paramount for ensuring financial stability, promoting environmental sustainability, and facilitating informed decision-making. Although classical risk estimation methods are extensively utilized, the implicit pre-assumptions regarding distribution are predominantly contained and challenging to balance accuracy and computational efficiency. A quantum computing-based carbon market risk estimation framework is proposed to address this problem with the quantum conditional generative adversarial network-quantum amplitude estimation (QCGAN-QAE) algorithm. Specifically, quantum conditional generative adversarial network (QCGAN) is employed to simulate the future distribution of the generated return rate, whereas quantum amplitude estimation (QAE) is employed to measure the distribution. Moreover, the quantum circuit of the QCGAN improved by reordering the data interaction layer and data simulation layer is coupled with the introduction of the quantum fully connected layer. The binary search method is incorporated into the QAE to bolster the computational efficiency. The simulation results based on the European Union Emissions Trading System reveals that the proposed framework markedly enhances the efficiency and precision of value-at-risk and conditional value-at-risk compared to original methods.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: