{"title":"CAGTRADE:利用 CNN-Attention-GRU 模型预测股市价格走势","authors":"Ibanga Kpereobong Friday, Sarada Prasanna Pati, Debahuti Mishra, Pradeep Kumar Mallick, Sachin Kumar","doi":"10.1007/s10690-024-09463-w","DOIUrl":null,"url":null,"abstract":"<div><p>Accurately predicting market direction is crucial for informed trading decisions to buy or sell stocks. This study proposes a deep learning based hybrid approach combining convolutional neural network (CNN), attention mechanism (AM), and gated recurrent unit (GRU) to predict short-term market trends (1 day, 3 days, 7 days, 10 days) across different stock indices (BSE, HSI, IXIC, NIFTY, N225, SSE). The architecture dynamically weights the input sequence with the AM model, captures local patterns through CNN and effectively models long-term dependencies with GRU thus aiming to accurately classify either \"<i>buy</i>\" or \"<i>sell</i>\" positions of stocks. The model is assessed using classification and financial evaluation metrics involving accuracy, precision, recall, f1-score, annualized returns, maximum drawdown, and return on investment. It outperforms benchmark models, and different technical indicators including average directional index, rate of change, moving average convergence divergence, and the buy-and-hold strategy, demonstrating its effectiveness in various market conditions. The proposed model achieves an average accuracy of 98% in predicting the 1 day-ahead direction, and an average accuracy of 88.53% across all prediction intervals. The model was also validated using the wilcoxon signed rank test that further supported its significance over the benchmark models. The CAG model presents a comprehensive and intuitive approach to stock market trend prediction, with potential applications in real-world asset decision-making.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"32 2","pages":"583 - 608"},"PeriodicalIF":2.6000,"publicationDate":"2024-06-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"CAGTRADE: Predicting Stock Market Price Movement with a CNN-Attention-GRU Model\",\"authors\":\"Ibanga Kpereobong Friday, Sarada Prasanna Pati, Debahuti Mishra, Pradeep Kumar Mallick, Sachin Kumar\",\"doi\":\"10.1007/s10690-024-09463-w\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>Accurately predicting market direction is crucial for informed trading decisions to buy or sell stocks. This study proposes a deep learning based hybrid approach combining convolutional neural network (CNN), attention mechanism (AM), and gated recurrent unit (GRU) to predict short-term market trends (1 day, 3 days, 7 days, 10 days) across different stock indices (BSE, HSI, IXIC, NIFTY, N225, SSE). The architecture dynamically weights the input sequence with the AM model, captures local patterns through CNN and effectively models long-term dependencies with GRU thus aiming to accurately classify either \\\"<i>buy</i>\\\" or \\\"<i>sell</i>\\\" positions of stocks. The model is assessed using classification and financial evaluation metrics involving accuracy, precision, recall, f1-score, annualized returns, maximum drawdown, and return on investment. It outperforms benchmark models, and different technical indicators including average directional index, rate of change, moving average convergence divergence, and the buy-and-hold strategy, demonstrating its effectiveness in various market conditions. The proposed model achieves an average accuracy of 98% in predicting the 1 day-ahead direction, and an average accuracy of 88.53% across all prediction intervals. The model was also validated using the wilcoxon signed rank test that further supported its significance over the benchmark models. The CAG model presents a comprehensive and intuitive approach to stock market trend prediction, with potential applications in real-world asset decision-making.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"32 2\",\"pages\":\"583 - 608\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2024-06-17\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-024-09463-w\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-024-09463-w","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

CAGTRADE: Predicting Stock Market Price Movement with a CNN-Attention-GRU Model

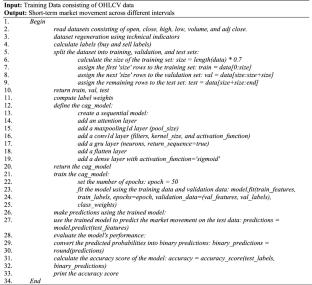

Accurately predicting market direction is crucial for informed trading decisions to buy or sell stocks. This study proposes a deep learning based hybrid approach combining convolutional neural network (CNN), attention mechanism (AM), and gated recurrent unit (GRU) to predict short-term market trends (1 day, 3 days, 7 days, 10 days) across different stock indices (BSE, HSI, IXIC, NIFTY, N225, SSE). The architecture dynamically weights the input sequence with the AM model, captures local patterns through CNN and effectively models long-term dependencies with GRU thus aiming to accurately classify either "buy" or "sell" positions of stocks. The model is assessed using classification and financial evaluation metrics involving accuracy, precision, recall, f1-score, annualized returns, maximum drawdown, and return on investment. It outperforms benchmark models, and different technical indicators including average directional index, rate of change, moving average convergence divergence, and the buy-and-hold strategy, demonstrating its effectiveness in various market conditions. The proposed model achieves an average accuracy of 98% in predicting the 1 day-ahead direction, and an average accuracy of 88.53% across all prediction intervals. The model was also validated using the wilcoxon signed rank test that further supported its significance over the benchmark models. The CAG model presents a comprehensive and intuitive approach to stock market trend prediction, with potential applications in real-world asset decision-making.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: