{"title":"将国际股票市场的风险状况作为功能数据进行比较:COVID-19 与全球金融危机","authors":"Ryan Liam Shackleton, Sonali Das, Rangan Gupta","doi":"10.1002/asmb.2879","DOIUrl":null,"url":null,"abstract":"<p>In this article, we aim to provide a detailed econometric analysis of the realized volatility in international stock markets of Brazil, China, Europe, India, the United Kingdom, and the United States, which represent a mix of large developing, and developed markets. For our purpose, we use the functional data analysis (FDA) framework, whence discrete volatility data were first transformed into continuous functions, and thereafter, derivatives of the continuous functions were investigated, and kinetic and potential energy associated is the volatility system were extracted. Results revealed that COVID-19 indeed had a significant effect on international financial market volatility for all the countries, with the exception of China. The realized volatility of the international financial markets did return to their pre-COVID levels in May 2020, and this recovery time was significantly faster than the 2008 financial crisis recovery period. Within the FDA framework, we further investigated the role of uncertainty on the realized volatility, specifically from an outbreak of an infectious disease (such as COVID-19) and a daily newspaper-based infectious disease index as the predictor. The regression analysis showed that the volatility of financial markets can be accurately modeled by this infectious disease index, but only for periods experiencing an epidemic or pandemic.</p>","PeriodicalId":55495,"journal":{"name":"Applied Stochastic Models in Business and Industry","volume":"40 4","pages":"1153-1181"},"PeriodicalIF":1.3000,"publicationDate":"2024-06-20","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/asmb.2879","citationCount":"0","resultStr":"{\"title\":\"Comparing risk profiles of international stock markets as functional data: COVID-19 versus the global financial crisis\",\"authors\":\"Ryan Liam Shackleton, Sonali Das, Rangan Gupta\",\"doi\":\"10.1002/asmb.2879\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In this article, we aim to provide a detailed econometric analysis of the realized volatility in international stock markets of Brazil, China, Europe, India, the United Kingdom, and the United States, which represent a mix of large developing, and developed markets. For our purpose, we use the functional data analysis (FDA) framework, whence discrete volatility data were first transformed into continuous functions, and thereafter, derivatives of the continuous functions were investigated, and kinetic and potential energy associated is the volatility system were extracted. Results revealed that COVID-19 indeed had a significant effect on international financial market volatility for all the countries, with the exception of China. The realized volatility of the international financial markets did return to their pre-COVID levels in May 2020, and this recovery time was significantly faster than the 2008 financial crisis recovery period. Within the FDA framework, we further investigated the role of uncertainty on the realized volatility, specifically from an outbreak of an infectious disease (such as COVID-19) and a daily newspaper-based infectious disease index as the predictor. The regression analysis showed that the volatility of financial markets can be accurately modeled by this infectious disease index, but only for periods experiencing an epidemic or pandemic.</p>\",\"PeriodicalId\":55495,\"journal\":{\"name\":\"Applied Stochastic Models in Business and Industry\",\"volume\":\"40 4\",\"pages\":\"1153-1181\"},\"PeriodicalIF\":1.3000,\"publicationDate\":\"2024-06-20\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/asmb.2879\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Applied Stochastic Models in Business and Industry\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/asmb.2879\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Applied Stochastic Models in Business and Industry","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/asmb.2879","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

Comparing risk profiles of international stock markets as functional data: COVID-19 versus the global financial crisis

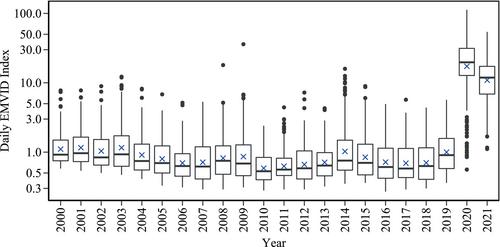

In this article, we aim to provide a detailed econometric analysis of the realized volatility in international stock markets of Brazil, China, Europe, India, the United Kingdom, and the United States, which represent a mix of large developing, and developed markets. For our purpose, we use the functional data analysis (FDA) framework, whence discrete volatility data were first transformed into continuous functions, and thereafter, derivatives of the continuous functions were investigated, and kinetic and potential energy associated is the volatility system were extracted. Results revealed that COVID-19 indeed had a significant effect on international financial market volatility for all the countries, with the exception of China. The realized volatility of the international financial markets did return to their pre-COVID levels in May 2020, and this recovery time was significantly faster than the 2008 financial crisis recovery period. Within the FDA framework, we further investigated the role of uncertainty on the realized volatility, specifically from an outbreak of an infectious disease (such as COVID-19) and a daily newspaper-based infectious disease index as the predictor. The regression analysis showed that the volatility of financial markets can be accurately modeled by this infectious disease index, but only for periods experiencing an epidemic or pandemic.

期刊介绍:

ASMBI - Applied Stochastic Models in Business and Industry (formerly Applied Stochastic Models and Data Analysis) was first published in 1985, publishing contributions in the interface between stochastic modelling, data analysis and their applications in business, finance, insurance, management and production. In 2007 ASMBI became the official journal of the International Society for Business and Industrial Statistics (www.isbis.org). The main objective is to publish papers, both technical and practical, presenting new results which solve real-life problems or have great potential in doing so. Mathematical rigour, innovative stochastic modelling and sound applications are the key ingredients of papers to be published, after a very selective review process.

The journal is very open to new ideas, like Data Science and Big Data stemming from problems in business and industry or uncertainty quantification in engineering, as well as more traditional ones, like reliability, quality control, design of experiments, managerial processes, supply chains and inventories, insurance, econometrics, financial modelling (provided the papers are related to real problems). The journal is interested also in papers addressing the effects of business and industrial decisions on the environment, healthcare, social life. State-of-the art computational methods are very welcome as well, when combined with sound applications and innovative models.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: