{"title":"在股价预测问题中,我们是否能从新闻流的分类中获益?","authors":"T. D. Kulikova, E. Yu. Kovtun, S. A. Budennyy","doi":"10.1134/S1064562423701648","DOIUrl":null,"url":null,"abstract":"<p>The power of machine learning is widely leveraged in the task of company stock price prediction. It is essential to incorporate historical stock prices and relevant external world information for constructing a more accurate predictive model. The sentiments of the financial news connected with the company can become such valuable knowledge. However, financial news has different topics, such as <i>Macro</i>, <i>Markets</i>, or <i>Product news</i>. The adoption of such categorization is usually out of scope in a market research. In this work, we aim to close this gap and explore the effect of capturing the news topic differentiation in the stock price prediction problem. Initially, we classify the financial news stream into 20 pre-defined topics with the pre-trained model. Then, we get sentiments and explore the topic of news group sentiment labeling. Moreover, we conduct the experiments with the several well-proved models for time series forecasting, including the Temporal Convolutional Network (TCN), the D-Linear, the Transformer, and the Temporal Fusion Transformer (TFT). In the results of our research, utilizing the information from separate topic groups contributes to a better performance of deep learning models compared to the approach when we consider all news sentiments without any division.</p>","PeriodicalId":531,"journal":{"name":"Doklady Mathematics","volume":"108 2 supplement","pages":"S503 - S510"},"PeriodicalIF":0.5000,"publicationDate":"2024-03-25","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Do we Benefit from the Categorization of the News Flow in the Stock Price Prediction Problem?\",\"authors\":\"T. D. Kulikova, E. Yu. Kovtun, S. A. Budennyy\",\"doi\":\"10.1134/S1064562423701648\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The power of machine learning is widely leveraged in the task of company stock price prediction. It is essential to incorporate historical stock prices and relevant external world information for constructing a more accurate predictive model. The sentiments of the financial news connected with the company can become such valuable knowledge. However, financial news has different topics, such as <i>Macro</i>, <i>Markets</i>, or <i>Product news</i>. The adoption of such categorization is usually out of scope in a market research. In this work, we aim to close this gap and explore the effect of capturing the news topic differentiation in the stock price prediction problem. Initially, we classify the financial news stream into 20 pre-defined topics with the pre-trained model. Then, we get sentiments and explore the topic of news group sentiment labeling. Moreover, we conduct the experiments with the several well-proved models for time series forecasting, including the Temporal Convolutional Network (TCN), the D-Linear, the Transformer, and the Temporal Fusion Transformer (TFT). In the results of our research, utilizing the information from separate topic groups contributes to a better performance of deep learning models compared to the approach when we consider all news sentiments without any division.</p>\",\"PeriodicalId\":531,\"journal\":{\"name\":\"Doklady Mathematics\",\"volume\":\"108 2 supplement\",\"pages\":\"S503 - S510\"},\"PeriodicalIF\":0.5000,\"publicationDate\":\"2024-03-25\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Doklady Mathematics\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://link.springer.com/article/10.1134/S1064562423701648\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Doklady Mathematics","FirstCategoryId":"100","ListUrlMain":"https://link.springer.com/article/10.1134/S1064562423701648","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS","Score":null,"Total":0}

Do we Benefit from the Categorization of the News Flow in the Stock Price Prediction Problem?

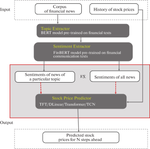

The power of machine learning is widely leveraged in the task of company stock price prediction. It is essential to incorporate historical stock prices and relevant external world information for constructing a more accurate predictive model. The sentiments of the financial news connected with the company can become such valuable knowledge. However, financial news has different topics, such as Macro, Markets, or Product news. The adoption of such categorization is usually out of scope in a market research. In this work, we aim to close this gap and explore the effect of capturing the news topic differentiation in the stock price prediction problem. Initially, we classify the financial news stream into 20 pre-defined topics with the pre-trained model. Then, we get sentiments and explore the topic of news group sentiment labeling. Moreover, we conduct the experiments with the several well-proved models for time series forecasting, including the Temporal Convolutional Network (TCN), the D-Linear, the Transformer, and the Temporal Fusion Transformer (TFT). In the results of our research, utilizing the information from separate topic groups contributes to a better performance of deep learning models compared to the approach when we consider all news sentiments without any division.

期刊介绍:

Doklady Mathematics is a journal of the Presidium of the Russian Academy of Sciences. It contains English translations of papers published in Doklady Akademii Nauk (Proceedings of the Russian Academy of Sciences), which was founded in 1933 and is published 36 times a year. Doklady Mathematics includes the materials from the following areas: mathematics, mathematical physics, computer science, control theory, and computers. It publishes brief scientific reports on previously unpublished significant new research in mathematics and its applications. The main contributors to the journal are Members of the RAS, Corresponding Members of the RAS, and scientists from the former Soviet Union and other foreign countries. Among the contributors are the outstanding Russian mathematicians.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: