{"title":"合成 GIC 的风险评估:资产负债管理的量化框架","authors":"Behzad Alimoradian, Jeffrey Jakubiak, Stéphane Loisel, Yahia Salhi","doi":"10.1007/s10203-024-00443-3","DOIUrl":null,"url":null,"abstract":"<p>This study addresses a research gap in quantitative modeling framework and scenario analysis for the risk management of stable value fund wraps, a crucial segment of the U.S. financial market with over USD $400 billion in assets. In this paper, we present an asset–liability model that encompasses an innovative approach to modeling the assets of fixed-income funds coupled with a liability model backed by empirical analysis on a unique data set covering 80% of the stand-alone plan sponsor market, contrasting with models based solely on regular deterministic cash flows and interest rate differences. Our model identifies and analyzes two critical risk scenarios from the insurer’s perspective: inflationary and yield spike. Our approach demonstrates that the tail risk of wraps, used as an economic capital measure, is sensitive to characteristic parameters of the fund, such as the duration, portfolio composition and credit quality of assets. This finding significantly differs from U.S. regulatory approaches like the NAIC’s, which often result in a zero capital requirement. These findings reveal limitations in current actuarial risk and profitability metrics for U.S. insurers and argue that a more sophisticated risk model reproducing the two critical scenarios is necessary.\n</p>","PeriodicalId":43711,"journal":{"name":"Decisions in Economics and Finance","volume":"6 1","pages":""},"PeriodicalIF":0.7000,"publicationDate":"2024-04-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Risk assessment for synthetic GICs: a quantitative framework for asset–liability management\",\"authors\":\"Behzad Alimoradian, Jeffrey Jakubiak, Stéphane Loisel, Yahia Salhi\",\"doi\":\"10.1007/s10203-024-00443-3\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study addresses a research gap in quantitative modeling framework and scenario analysis for the risk management of stable value fund wraps, a crucial segment of the U.S. financial market with over USD $400 billion in assets. In this paper, we present an asset–liability model that encompasses an innovative approach to modeling the assets of fixed-income funds coupled with a liability model backed by empirical analysis on a unique data set covering 80% of the stand-alone plan sponsor market, contrasting with models based solely on regular deterministic cash flows and interest rate differences. Our model identifies and analyzes two critical risk scenarios from the insurer’s perspective: inflationary and yield spike. Our approach demonstrates that the tail risk of wraps, used as an economic capital measure, is sensitive to characteristic parameters of the fund, such as the duration, portfolio composition and credit quality of assets. This finding significantly differs from U.S. regulatory approaches like the NAIC’s, which often result in a zero capital requirement. These findings reveal limitations in current actuarial risk and profitability metrics for U.S. insurers and argue that a more sophisticated risk model reproducing the two critical scenarios is necessary.\\n</p>\",\"PeriodicalId\":43711,\"journal\":{\"name\":\"Decisions in Economics and Finance\",\"volume\":\"6 1\",\"pages\":\"\"},\"PeriodicalIF\":0.7000,\"publicationDate\":\"2024-04-11\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Decisions in Economics and Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s10203-024-00443-3\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"SOCIAL SCIENCES, MATHEMATICAL METHODS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Decisions in Economics and Finance","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s10203-024-00443-3","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"SOCIAL SCIENCES, MATHEMATICAL METHODS","Score":null,"Total":0}

Risk assessment for synthetic GICs: a quantitative framework for asset–liability management

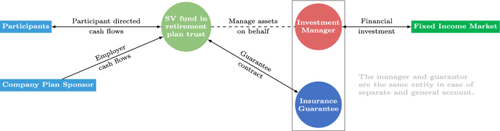

This study addresses a research gap in quantitative modeling framework and scenario analysis for the risk management of stable value fund wraps, a crucial segment of the U.S. financial market with over USD $400 billion in assets. In this paper, we present an asset–liability model that encompasses an innovative approach to modeling the assets of fixed-income funds coupled with a liability model backed by empirical analysis on a unique data set covering 80% of the stand-alone plan sponsor market, contrasting with models based solely on regular deterministic cash flows and interest rate differences. Our model identifies and analyzes two critical risk scenarios from the insurer’s perspective: inflationary and yield spike. Our approach demonstrates that the tail risk of wraps, used as an economic capital measure, is sensitive to characteristic parameters of the fund, such as the duration, portfolio composition and credit quality of assets. This finding significantly differs from U.S. regulatory approaches like the NAIC’s, which often result in a zero capital requirement. These findings reveal limitations in current actuarial risk and profitability metrics for U.S. insurers and argue that a more sophisticated risk model reproducing the two critical scenarios is necessary.

期刊介绍:

Decisions in Economics and Finance: A Journal of Applied Mathematics is the official publication of the Association for Mathematics Applied to Social and Economic Sciences (AMASES). It provides a specialised forum for the publication of research in all areas of mathematics as applied to economics, finance, insurance, management and social sciences. Primary emphasis is placed on original research concerning topics in mathematics or computational techniques which are explicitly motivated by or contribute to the analysis of economic or financial problems.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: