Oktay Ozkan, Salah Abosedra, Arshian Sharif, Andrew Adewale Alola

{"title":"化石能源、清洁能源和主要资产之间的动态波动性:来自新型 DCC-GARCH 的证据","authors":"Oktay Ozkan, Salah Abosedra, Arshian Sharif, Andrew Adewale Alola","doi":"10.1007/s10644-024-09696-9","DOIUrl":null,"url":null,"abstract":"<p>The objective of this paper is to assess the dynamic volatility connectedness between fossil energy, clean energy, and major assets i.e., Bonds, Bitcoin, Dollar index, Gold, and Standard and Poor's 500 from September 17, 2014 to October 11, 2022. The main motivation of the study relates to examining the dynamic volatility connectedness mentioned during periods of important events such as the recent coronavirus pandemic and the Russia–Ukraine conflict which has shown the vulnerability of economic and financial assets, energy commodities, and clean energy. The novel Dynamic Conditional Correlation-Generalized Autoregressive Conditional Heteroskedasticity (DCC-GARCH) approach is employed for the investigation of the sample period mentioned. Empirical analysis reveals that both the total and net volatility connectedness between assets is time-varying. The highest connectedness among the assets is observed with the onset of the coronavirus (COVID-19) pandemic, and it increases with some important international events, such as the Russia–Ukraine conflict, the referendum of Brexit, China–US trade war, and Brexit day. On average, the result shows that 32.8% of the volatility in one asset spills over to all other assets. The DCC-GARCH results also indicate that crude oil, bonds, and Bitcoin act as almost pure volatility transmitters, whereas the Dollar index, gold, and S&P500 act as volatility receivers. On the other hand, clean energy is found neutral to external shocks until the first quarter of 2020 and after that time, it starts to behave as a volatility transmitter. Based on the obtained results, we offer some specific policy implications that are beneficial to the US economy and other countries.</p><h3 data-test=\"abstract-sub-heading\">Graphical Abstract</h3><p>Dynamic volatility connectedness between fossil energy, clean energy, and major assets (Bonds, Bitcoin, Dollar index, Gold, and Standard and Poor's 500)\n</p>","PeriodicalId":46127,"journal":{"name":"Economic Change and Restructuring","volume":"119 1","pages":""},"PeriodicalIF":4.3000,"publicationDate":"2024-04-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Dynamic volatility among fossil energy, clean energy and major assets: evidence from the novel DCC-GARCH\",\"authors\":\"Oktay Ozkan, Salah Abosedra, Arshian Sharif, Andrew Adewale Alola\",\"doi\":\"10.1007/s10644-024-09696-9\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The objective of this paper is to assess the dynamic volatility connectedness between fossil energy, clean energy, and major assets i.e., Bonds, Bitcoin, Dollar index, Gold, and Standard and Poor's 500 from September 17, 2014 to October 11, 2022. The main motivation of the study relates to examining the dynamic volatility connectedness mentioned during periods of important events such as the recent coronavirus pandemic and the Russia–Ukraine conflict which has shown the vulnerability of economic and financial assets, energy commodities, and clean energy. The novel Dynamic Conditional Correlation-Generalized Autoregressive Conditional Heteroskedasticity (DCC-GARCH) approach is employed for the investigation of the sample period mentioned. Empirical analysis reveals that both the total and net volatility connectedness between assets is time-varying. The highest connectedness among the assets is observed with the onset of the coronavirus (COVID-19) pandemic, and it increases with some important international events, such as the Russia–Ukraine conflict, the referendum of Brexit, China–US trade war, and Brexit day. On average, the result shows that 32.8% of the volatility in one asset spills over to all other assets. The DCC-GARCH results also indicate that crude oil, bonds, and Bitcoin act as almost pure volatility transmitters, whereas the Dollar index, gold, and S&P500 act as volatility receivers. On the other hand, clean energy is found neutral to external shocks until the first quarter of 2020 and after that time, it starts to behave as a volatility transmitter. Based on the obtained results, we offer some specific policy implications that are beneficial to the US economy and other countries.</p><h3 data-test=\\\"abstract-sub-heading\\\">Graphical Abstract</h3><p>Dynamic volatility connectedness between fossil energy, clean energy, and major assets (Bonds, Bitcoin, Dollar index, Gold, and Standard and Poor's 500)\\n</p>\",\"PeriodicalId\":46127,\"journal\":{\"name\":\"Economic Change and Restructuring\",\"volume\":\"119 1\",\"pages\":\"\"},\"PeriodicalIF\":4.3000,\"publicationDate\":\"2024-04-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Economic Change and Restructuring\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10644-024-09696-9\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Economic Change and Restructuring","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10644-024-09696-9","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

Dynamic volatility among fossil energy, clean energy and major assets: evidence from the novel DCC-GARCH

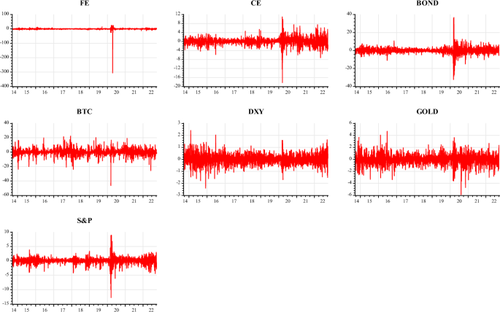

The objective of this paper is to assess the dynamic volatility connectedness between fossil energy, clean energy, and major assets i.e., Bonds, Bitcoin, Dollar index, Gold, and Standard and Poor's 500 from September 17, 2014 to October 11, 2022. The main motivation of the study relates to examining the dynamic volatility connectedness mentioned during periods of important events such as the recent coronavirus pandemic and the Russia–Ukraine conflict which has shown the vulnerability of economic and financial assets, energy commodities, and clean energy. The novel Dynamic Conditional Correlation-Generalized Autoregressive Conditional Heteroskedasticity (DCC-GARCH) approach is employed for the investigation of the sample period mentioned. Empirical analysis reveals that both the total and net volatility connectedness between assets is time-varying. The highest connectedness among the assets is observed with the onset of the coronavirus (COVID-19) pandemic, and it increases with some important international events, such as the Russia–Ukraine conflict, the referendum of Brexit, China–US trade war, and Brexit day. On average, the result shows that 32.8% of the volatility in one asset spills over to all other assets. The DCC-GARCH results also indicate that crude oil, bonds, and Bitcoin act as almost pure volatility transmitters, whereas the Dollar index, gold, and S&P500 act as volatility receivers. On the other hand, clean energy is found neutral to external shocks until the first quarter of 2020 and after that time, it starts to behave as a volatility transmitter. Based on the obtained results, we offer some specific policy implications that are beneficial to the US economy and other countries.

Graphical Abstract

Dynamic volatility connectedness between fossil energy, clean energy, and major assets (Bonds, Bitcoin, Dollar index, Gold, and Standard and Poor's 500)

期刊介绍:

Economic Change and Restructuring has been accepted for SSCI and will get its first Impact Factor in 2020!Since the early 1990s fundamental changes in the world economy, under the auspices of increasing globalisation, have taken place

On one hand, the disappearance of the centrally planned economies and the progressive formation of market-oriented economies, have brought about countless systematic changes, where new economic structures, institutions, competences and skills involve complex processes, changes which are still underway and which necessitate adaptation and restructuring to form competitive market economies.

On the other hand, many developing economies are making great strides as regards economic reform and liberalisation, and are emerging as new global players. They show an innovative capacity to position themselves in the global economy and to compete with industrialised countries, which are generally believed to be witnessing the rapid erosion of their established positions. These developments are accompanied by the exacerbation of the world competition.

Both processes involve transition and the emerging economies, in searching for a new role and scope for public policies and for a new balance between public and private partnership, seem to currently be converging, especially with respect to the policies needed to create appropriate and effective market institutions and integrated reform policies, and to increase the standards of the population''s education levels.

Thus, liberalisation and development policies, in attempting to strike a difficult balance between social and environmental needs, must be integrated more coherently. This complexity calls for new analytical and empirical approaches that can explain these new phenomena, which often go beyond the over-simplified facts and conventional ''wisdom'' that emerged at the start of the transition in the early 1990s.

Economic Change and Restructuring (formerly ''Economics of Planning''), by keeping abreast of developments affecting both transitional and emerging economies, is aimed to attract original empirical and policy analysis contributions that are focused on various issues, including macroeconomic analysis, fiscal issues, finance and banking, industrial and trade development, and regional and local development issues.

The journal aspires to publish cutting edge research and to serve as a forum for economists and policymakers working in these fields.Officially cited as: Econ Change Restruct

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: