{"title":"自激索赔模式下的最佳索赔比例再保险","authors":"Fan Wu, Yang Shen, Xin Zhang, Kai Ding","doi":"10.1007/s10957-024-02429-y","DOIUrl":null,"url":null,"abstract":"<p>This paper investigates an optimal reinsurance problem for an insurance company with self-exciting claims, where the insurer’s historical claims affect the claim intensity itself. We focus on a claim-dependent proportional reinsurance contact, where the term “claim-dependent” signifies that the insurer’s risk retention ratio is allowed to depend on claim size. The insurer aims to maximize the expected utility of terminal wealth. By utilizing the dynamic programming principle and verification theorem, we obtain the optimal reinsurance strategy and corresponding value function in closed-form from the Hamilton–Jacobi–Bellman equation under an exponential utility function. We show that the claim-dependent proportional reinsurance is optimal among all types of reinsurance under the exponential utility maximization criterion. In addition, we present several analytical properties and numerical examples of the derived optimal strategy and provide economic insights through analytical and numerical analyses. In particular, we show the optimal claim-dependent proportional reinsurance can be considered as a continuous approximation of the step-wise risk sharing rule between the insurer and the reinsurer.</p>","PeriodicalId":50100,"journal":{"name":"Journal of Optimization Theory and Applications","volume":"42 1","pages":""},"PeriodicalIF":1.5000,"publicationDate":"2024-04-10","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Optimal Claim-Dependent Proportional Reinsurance Under a Self-Exciting Claim Model\",\"authors\":\"Fan Wu, Yang Shen, Xin Zhang, Kai Ding\",\"doi\":\"10.1007/s10957-024-02429-y\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper investigates an optimal reinsurance problem for an insurance company with self-exciting claims, where the insurer’s historical claims affect the claim intensity itself. We focus on a claim-dependent proportional reinsurance contact, where the term “claim-dependent” signifies that the insurer’s risk retention ratio is allowed to depend on claim size. The insurer aims to maximize the expected utility of terminal wealth. By utilizing the dynamic programming principle and verification theorem, we obtain the optimal reinsurance strategy and corresponding value function in closed-form from the Hamilton–Jacobi–Bellman equation under an exponential utility function. We show that the claim-dependent proportional reinsurance is optimal among all types of reinsurance under the exponential utility maximization criterion. In addition, we present several analytical properties and numerical examples of the derived optimal strategy and provide economic insights through analytical and numerical analyses. In particular, we show the optimal claim-dependent proportional reinsurance can be considered as a continuous approximation of the step-wise risk sharing rule between the insurer and the reinsurer.</p>\",\"PeriodicalId\":50100,\"journal\":{\"name\":\"Journal of Optimization Theory and Applications\",\"volume\":\"42 1\",\"pages\":\"\"},\"PeriodicalIF\":1.5000,\"publicationDate\":\"2024-04-10\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Optimization Theory and Applications\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://doi.org/10.1007/s10957-024-02429-y\",\"RegionNum\":3,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"MATHEMATICS, APPLIED\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Optimization Theory and Applications","FirstCategoryId":"100","ListUrlMain":"https://doi.org/10.1007/s10957-024-02429-y","RegionNum":3,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"MATHEMATICS, APPLIED","Score":null,"Total":0}

Optimal Claim-Dependent Proportional Reinsurance Under a Self-Exciting Claim Model

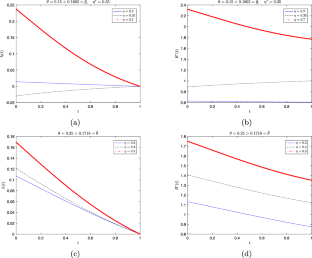

This paper investigates an optimal reinsurance problem for an insurance company with self-exciting claims, where the insurer’s historical claims affect the claim intensity itself. We focus on a claim-dependent proportional reinsurance contact, where the term “claim-dependent” signifies that the insurer’s risk retention ratio is allowed to depend on claim size. The insurer aims to maximize the expected utility of terminal wealth. By utilizing the dynamic programming principle and verification theorem, we obtain the optimal reinsurance strategy and corresponding value function in closed-form from the Hamilton–Jacobi–Bellman equation under an exponential utility function. We show that the claim-dependent proportional reinsurance is optimal among all types of reinsurance under the exponential utility maximization criterion. In addition, we present several analytical properties and numerical examples of the derived optimal strategy and provide economic insights through analytical and numerical analyses. In particular, we show the optimal claim-dependent proportional reinsurance can be considered as a continuous approximation of the step-wise risk sharing rule between the insurer and the reinsurer.

期刊介绍:

The Journal of Optimization Theory and Applications is devoted to the publication of carefully selected regular papers, invited papers, survey papers, technical notes, book notices, and forums that cover mathematical optimization techniques and their applications to science and engineering. Typical theoretical areas include linear, nonlinear, mathematical, and dynamic programming. Among the areas of application covered are mathematical economics, mathematical physics and biology, and aerospace, chemical, civil, electrical, and mechanical engineering.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: