{"title":"自恋型首席执行官的诱人行为:来自回购公告的证据","authors":"Evans O. Boamah, Shantanu Banerjee","doi":"10.1111/jbfa.12796","DOIUrl":null,"url":null,"abstract":"<p>We study whether Chief Executive Officer (CEO) narcissism affects a firm's share repurchase announcements and their implementations. Using signature characteristics as a measure of narcissism, we find that US firms with narcissist CEOs are more likely to make repurchase announcements and announce higher repurchase dollar amounts. However, these firms are less likely to follow through. Actual repurchases by these firms are less frequent, and they use a smaller amount of cash for share buyback because they have a higher cashflow sensitivity of cash. Narcissist CEOs’ repurchase announcements are less driven by market timing and have a lower announcement effect compared to those by other CEOs. The higher rate and amount of repurchase announcements are more pronounced in poorly governed firms with narcissistic CEOs. These results are robust to various specifications including a difference-in-difference set-up using CEOs’ exogenous turnover, controlling for other CEO traits and using an alternative measure of narcissism based on pronoun usage in CEO communications. Collectively, the results presented in this study demonstrate that narcissist CEOs play a critical role in the intensity of share repurchase announcements and their executions, particularly for firms with weaker governance structures.</p>","PeriodicalId":48106,"journal":{"name":"Journal of Business Finance & Accounting","volume":"51 3-4","pages":"717-755"},"PeriodicalIF":2.2000,"publicationDate":"2024-03-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12796","citationCount":"0","resultStr":"{\"title\":\"The beguiling behaviour of narcissistic CEOs: Evidence from repurchase announcements\",\"authors\":\"Evans O. Boamah, Shantanu Banerjee\",\"doi\":\"10.1111/jbfa.12796\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We study whether Chief Executive Officer (CEO) narcissism affects a firm's share repurchase announcements and their implementations. Using signature characteristics as a measure of narcissism, we find that US firms with narcissist CEOs are more likely to make repurchase announcements and announce higher repurchase dollar amounts. However, these firms are less likely to follow through. Actual repurchases by these firms are less frequent, and they use a smaller amount of cash for share buyback because they have a higher cashflow sensitivity of cash. Narcissist CEOs’ repurchase announcements are less driven by market timing and have a lower announcement effect compared to those by other CEOs. The higher rate and amount of repurchase announcements are more pronounced in poorly governed firms with narcissistic CEOs. These results are robust to various specifications including a difference-in-difference set-up using CEOs’ exogenous turnover, controlling for other CEO traits and using an alternative measure of narcissism based on pronoun usage in CEO communications. Collectively, the results presented in this study demonstrate that narcissist CEOs play a critical role in the intensity of share repurchase announcements and their executions, particularly for firms with weaker governance structures.</p>\",\"PeriodicalId\":48106,\"journal\":{\"name\":\"Journal of Business Finance & Accounting\",\"volume\":\"51 3-4\",\"pages\":\"717-755\"},\"PeriodicalIF\":2.2000,\"publicationDate\":\"2024-03-26\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12796\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Business Finance & Accounting\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12796\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Business Finance & Accounting","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12796","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

The beguiling behaviour of narcissistic CEOs: Evidence from repurchase announcements

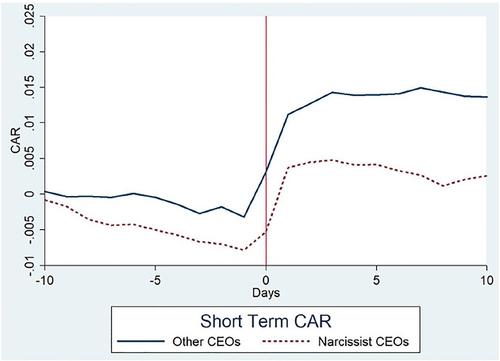

We study whether Chief Executive Officer (CEO) narcissism affects a firm's share repurchase announcements and their implementations. Using signature characteristics as a measure of narcissism, we find that US firms with narcissist CEOs are more likely to make repurchase announcements and announce higher repurchase dollar amounts. However, these firms are less likely to follow through. Actual repurchases by these firms are less frequent, and they use a smaller amount of cash for share buyback because they have a higher cashflow sensitivity of cash. Narcissist CEOs’ repurchase announcements are less driven by market timing and have a lower announcement effect compared to those by other CEOs. The higher rate and amount of repurchase announcements are more pronounced in poorly governed firms with narcissistic CEOs. These results are robust to various specifications including a difference-in-difference set-up using CEOs’ exogenous turnover, controlling for other CEO traits and using an alternative measure of narcissism based on pronoun usage in CEO communications. Collectively, the results presented in this study demonstrate that narcissist CEOs play a critical role in the intensity of share repurchase announcements and their executions, particularly for firms with weaker governance structures.

期刊介绍:

Journal of Business Finance and Accounting exists to publish high quality research papers in accounting, corporate finance, corporate governance and their interfaces. The interfaces are relevant in many areas such as financial reporting and communication, valuation, financial performance measurement and managerial reward and control structures. A feature of JBFA is that it recognises that informational problems are pervasive in financial markets and business organisations, and that accounting plays an important role in resolving such problems. JBFA welcomes both theoretical and empirical contributions. Nonetheless, theoretical papers should yield novel testable implications, and empirical papers should be theoretically well-motivated. The Editors view accounting and finance as being closely related to economics and, as a consequence, papers submitted will often have theoretical motivations that are grounded in economics. JBFA, however, also seeks papers that complement economics-based theorising with theoretical developments originating in other social science disciplines or traditions. While many papers in JBFA use econometric or related empirical methods, the Editors also welcome contributions that use other empirical research methods. Although the scope of JBFA is broad, it is not a suitable outlet for highly abstract mathematical papers, or empirical papers with inadequate theoretical motivation. Also, papers that study asset pricing, or the operations of financial markets, should have direct implications for one or more of preparers, regulators, users of financial statements, and corporate financial decision makers, or at least should have implications for the development of future research relevant to such users.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: