Jungmin Shin, Seunghyun Gwak, Seung Jun Shin, Sungwan Bang

{"title":"利用深度神经网络实现非交叉多元量级回归的同步估计和变量选择","authors":"Jungmin Shin, Seunghyun Gwak, Seung Jun Shin, Sungwan Bang","doi":"10.1007/s11222-024-10418-4","DOIUrl":null,"url":null,"abstract":"<p>In this paper, we present the DNN-NMQR estimator, an approach that utilizes a deep neural network structure to solve multiple quantile regression problems. When estimating multiple quantiles, our approach leverages the structural characteristics of DNN to enhance estimation results by encouraging shared learning across different quantiles through DNN-NMQR. Also, this method effectively addresses quantile crossing issues through the penalization method. To refine our methodology, we introduce a convolution-type quadratic smoothing function, ensuring that the objective function remains differentiable throughout. Furthermore, we provide a brief discussion on the convergence analysis of DNN-NMQR, drawing on the concept of the neural tangent kernel. For a high-dimensional case, we propose the (A)GDNN-NMQR estimator, which applies group-wise <span>\\(L_1\\)</span>-type regularization methods and enjoys the advantages of quantile estimation and variable selection simultaneously. We extensively validate all of our proposed methods through numerical experiments and real data analysis.</p>","PeriodicalId":22058,"journal":{"name":"Statistics and Computing","volume":"22 1","pages":""},"PeriodicalIF":1.6000,"publicationDate":"2024-03-22","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Simultaneous estimation and variable selection for a non-crossing multiple quantile regression using deep neural networks\",\"authors\":\"Jungmin Shin, Seunghyun Gwak, Seung Jun Shin, Sungwan Bang\",\"doi\":\"10.1007/s11222-024-10418-4\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In this paper, we present the DNN-NMQR estimator, an approach that utilizes a deep neural network structure to solve multiple quantile regression problems. When estimating multiple quantiles, our approach leverages the structural characteristics of DNN to enhance estimation results by encouraging shared learning across different quantiles through DNN-NMQR. Also, this method effectively addresses quantile crossing issues through the penalization method. To refine our methodology, we introduce a convolution-type quadratic smoothing function, ensuring that the objective function remains differentiable throughout. Furthermore, we provide a brief discussion on the convergence analysis of DNN-NMQR, drawing on the concept of the neural tangent kernel. For a high-dimensional case, we propose the (A)GDNN-NMQR estimator, which applies group-wise <span>\\\\(L_1\\\\)</span>-type regularization methods and enjoys the advantages of quantile estimation and variable selection simultaneously. We extensively validate all of our proposed methods through numerical experiments and real data analysis.</p>\",\"PeriodicalId\":22058,\"journal\":{\"name\":\"Statistics and Computing\",\"volume\":\"22 1\",\"pages\":\"\"},\"PeriodicalIF\":1.6000,\"publicationDate\":\"2024-03-22\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Statistics and Computing\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://doi.org/10.1007/s11222-024-10418-4\",\"RegionNum\":2,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"COMPUTER SCIENCE, THEORY & METHODS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Statistics and Computing","FirstCategoryId":"100","ListUrlMain":"https://doi.org/10.1007/s11222-024-10418-4","RegionNum":2,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"COMPUTER SCIENCE, THEORY & METHODS","Score":null,"Total":0}

Simultaneous estimation and variable selection for a non-crossing multiple quantile regression using deep neural networks

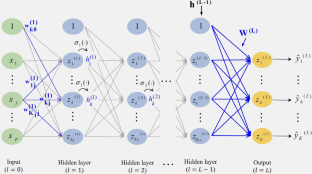

In this paper, we present the DNN-NMQR estimator, an approach that utilizes a deep neural network structure to solve multiple quantile regression problems. When estimating multiple quantiles, our approach leverages the structural characteristics of DNN to enhance estimation results by encouraging shared learning across different quantiles through DNN-NMQR. Also, this method effectively addresses quantile crossing issues through the penalization method. To refine our methodology, we introduce a convolution-type quadratic smoothing function, ensuring that the objective function remains differentiable throughout. Furthermore, we provide a brief discussion on the convergence analysis of DNN-NMQR, drawing on the concept of the neural tangent kernel. For a high-dimensional case, we propose the (A)GDNN-NMQR estimator, which applies group-wise \(L_1\)-type regularization methods and enjoys the advantages of quantile estimation and variable selection simultaneously. We extensively validate all of our proposed methods through numerical experiments and real data analysis.

期刊介绍:

Statistics and Computing is a bi-monthly refereed journal which publishes papers covering the range of the interface between the statistical and computing sciences.

In particular, it addresses the use of statistical concepts in computing science, for example in machine learning, computer vision and data analytics, as well as the use of computers in data modelling, prediction and analysis. Specific topics which are covered include: techniques for evaluating analytically intractable problems such as bootstrap resampling, Markov chain Monte Carlo, sequential Monte Carlo, approximate Bayesian computation, search and optimization methods, stochastic simulation and Monte Carlo, graphics, computer environments, statistical approaches to software errors, information retrieval, machine learning, statistics of databases and database technology, huge data sets and big data analytics, computer algebra, graphical models, image processing, tomography, inverse problems and uncertainty quantification.

In addition, the journal contains original research reports, authoritative review papers, discussed papers, and occasional special issues on particular topics or carrying proceedings of relevant conferences. Statistics and Computing also publishes book review and software review sections.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: