{"title":"ESG基金经理是否会在其投资组合中抽空抛售股票?欧洲证据","authors":"Spyros Papathanasiou, Dimitris Kenourgios, Drosos Koutsokostas","doi":"10.1057/s41260-024-00351-6","DOIUrl":null,"url":null,"abstract":"<p>We investigate portfolio pumping around quarter-ends by ESG equity mutual funds domiciled in the largest European markets in sustainable investments, i.e., the UK, France and Germany, for the period from January 2010 to December 2022. We find strong evidence that the UK funds inflate quarter-end returns, with price spikes being stronger at year-ends; nevertheless, the magnitude of price inflation is less than that of their conventional counterparts. On the contrary, results indicate that German and French funds do not engage in portfolio pumping. The COVID-19 pandemic strengthened the propensity of fund managers to cause a profound artificial enhancement to the performance of the investment portfolio. Further analysis shows that portfolio pumping is more prominent among the worst-performing funds, funds that charge investors with lower fees and achieve a poor ESG rating. However, managers that pump fund returns do not attract significantly more flows. Our results have produced valuable insights for regulators and investors participating in ESG markets, highlighting the necessity for a rigorous surveillance of the UK ESG equity market.</p>","PeriodicalId":45953,"journal":{"name":"Journal of Asset Management","volume":"159 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2024-03-20","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Do ESG fund managers pump and dump the stocks in their portfolios? European evidence\",\"authors\":\"Spyros Papathanasiou, Dimitris Kenourgios, Drosos Koutsokostas\",\"doi\":\"10.1057/s41260-024-00351-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We investigate portfolio pumping around quarter-ends by ESG equity mutual funds domiciled in the largest European markets in sustainable investments, i.e., the UK, France and Germany, for the period from January 2010 to December 2022. We find strong evidence that the UK funds inflate quarter-end returns, with price spikes being stronger at year-ends; nevertheless, the magnitude of price inflation is less than that of their conventional counterparts. On the contrary, results indicate that German and French funds do not engage in portfolio pumping. The COVID-19 pandemic strengthened the propensity of fund managers to cause a profound artificial enhancement to the performance of the investment portfolio. Further analysis shows that portfolio pumping is more prominent among the worst-performing funds, funds that charge investors with lower fees and achieve a poor ESG rating. However, managers that pump fund returns do not attract significantly more flows. Our results have produced valuable insights for regulators and investors participating in ESG markets, highlighting the necessity for a rigorous surveillance of the UK ESG equity market.</p>\",\"PeriodicalId\":45953,\"journal\":{\"name\":\"Journal of Asset Management\",\"volume\":\"159 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2024-03-20\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Asset Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1057/s41260-024-00351-6\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Asset Management","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41260-024-00351-6","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Do ESG fund managers pump and dump the stocks in their portfolios? European evidence

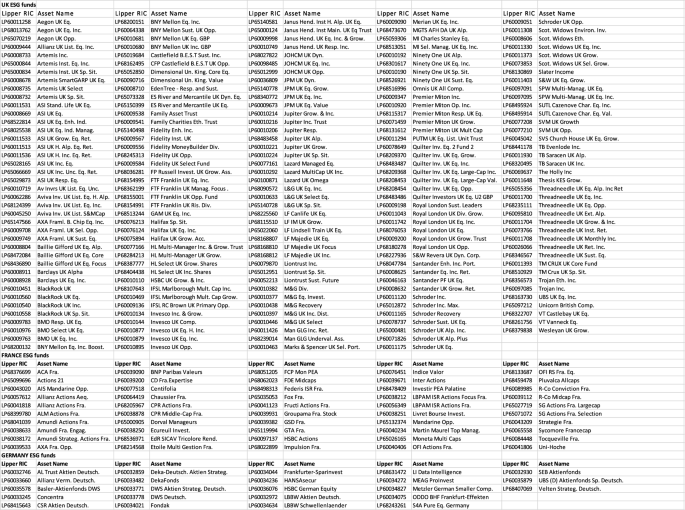

We investigate portfolio pumping around quarter-ends by ESG equity mutual funds domiciled in the largest European markets in sustainable investments, i.e., the UK, France and Germany, for the period from January 2010 to December 2022. We find strong evidence that the UK funds inflate quarter-end returns, with price spikes being stronger at year-ends; nevertheless, the magnitude of price inflation is less than that of their conventional counterparts. On the contrary, results indicate that German and French funds do not engage in portfolio pumping. The COVID-19 pandemic strengthened the propensity of fund managers to cause a profound artificial enhancement to the performance of the investment portfolio. Further analysis shows that portfolio pumping is more prominent among the worst-performing funds, funds that charge investors with lower fees and achieve a poor ESG rating. However, managers that pump fund returns do not attract significantly more flows. Our results have produced valuable insights for regulators and investors participating in ESG markets, highlighting the necessity for a rigorous surveillance of the UK ESG equity market.

期刊介绍:

The Journal of Asset Management covers:new investment strategies, methodologies and techniquesnew products and trading developmentsimportant regulatory and legal developmentsemerging trends in asset managementUnder the guidance of its expert Editors and an eminent international Editorial Board, Journal of Asset Management has developed to provide an international forum for latest thinking, techniques and developments for the Fund Management Industry, from high-growth investment strategies to modelling and managing risk, from active management to index tracking. The Journal has established itself as a key bridge between applied academic research, commercial best practice and regulatory interests, globally.Each issue of Journal of Asset Management publishes detailed, authoritative briefings, analysis, research and reviews by leading experts in the field, to keep subscribers up to date with the latest developments and thinking in asset management.Journal of Asset Management covers:asset allocation hedge fund strategies risk definition and management index tracking performance measurement stock selection investment methodologies and techniques portfolio management and weighting product development and innovation active asset management style analysis strategies to match client profiles time horizons emerging markets alternative investments derivatives and hedging instruments pensions economics

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: