{"title":"瞬时价格乘数影响下的实物或现金结算套期保值","authors":"Dirk Becherer, Todor Bilarev","doi":"10.1007/s00780-024-00531-7","DOIUrl":null,"url":null,"abstract":"<p>We solve the superhedging problem for European options in an illiquid extension of the Black–Scholes model, in which transactions have transient price impact and the costs and strategies for hedging are affected by physical or cash settlement requirements at maturity. Our analysis is based on a convenient choice of reduced effective coordinates of magnitudes at liquidation for geometric dynamic programming. The price impact is transient over time and multiplicative, ensuring nonnegativity of underlying asset prices while maintaining an arbitrage-free model. The basic (log-)linear example is a Black–Scholes model with a relative price impact proportional to the volume of shares traded, where the transience for impact on log-prices is modelled like in Obizhaeva and Wang (J. Financ. Mark. 16:1–32, 2013) for nominal prices. More generally, we allow nonlinear price impact and resilience functions. The viscosity solutions describing the minimal superhedging price are governed by the transient character of the price impact and by the physical or cash settlement specifications. The pricing equations under illiquidity extend no-arbitrage pricing à la Black–Scholes for complete markets in a non-paradoxical way (cf. Çetin et al. (Finance Stoch. 14:317–341, 2010)) even without additional frictions, and can recover it in base cases.</p>","PeriodicalId":50447,"journal":{"name":"Finance and Stochastics","volume":"2 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2024-03-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Hedging with physical or cash settlement under transient multiplicative price impact\",\"authors\":\"Dirk Becherer, Todor Bilarev\",\"doi\":\"10.1007/s00780-024-00531-7\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We solve the superhedging problem for European options in an illiquid extension of the Black–Scholes model, in which transactions have transient price impact and the costs and strategies for hedging are affected by physical or cash settlement requirements at maturity. Our analysis is based on a convenient choice of reduced effective coordinates of magnitudes at liquidation for geometric dynamic programming. The price impact is transient over time and multiplicative, ensuring nonnegativity of underlying asset prices while maintaining an arbitrage-free model. The basic (log-)linear example is a Black–Scholes model with a relative price impact proportional to the volume of shares traded, where the transience for impact on log-prices is modelled like in Obizhaeva and Wang (J. Financ. Mark. 16:1–32, 2013) for nominal prices. More generally, we allow nonlinear price impact and resilience functions. The viscosity solutions describing the minimal superhedging price are governed by the transient character of the price impact and by the physical or cash settlement specifications. The pricing equations under illiquidity extend no-arbitrage pricing à la Black–Scholes for complete markets in a non-paradoxical way (cf. Çetin et al. (Finance Stoch. 14:317–341, 2010)) even without additional frictions, and can recover it in base cases.</p>\",\"PeriodicalId\":50447,\"journal\":{\"name\":\"Finance and Stochastics\",\"volume\":\"2 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2024-03-15\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Finance and Stochastics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s00780-024-00531-7\",\"RegionNum\":2,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Finance and Stochastics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s00780-024-00531-7","RegionNum":2,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Hedging with physical or cash settlement under transient multiplicative price impact

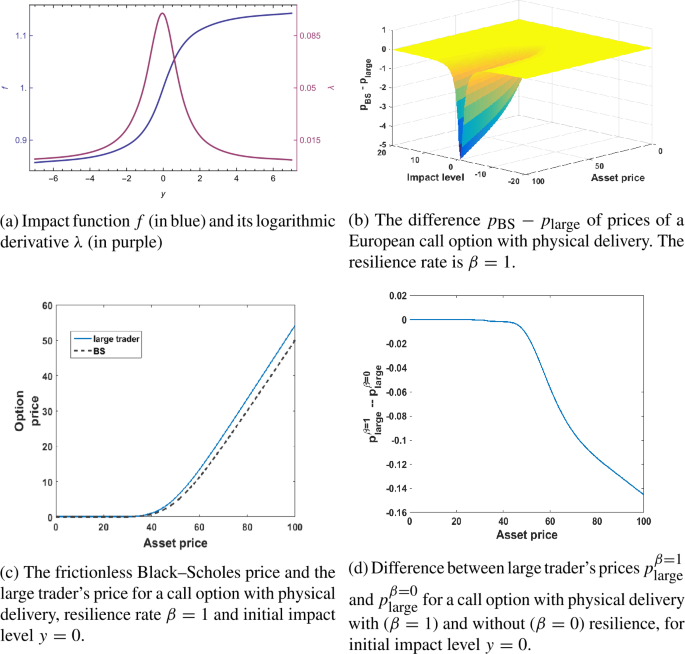

We solve the superhedging problem for European options in an illiquid extension of the Black–Scholes model, in which transactions have transient price impact and the costs and strategies for hedging are affected by physical or cash settlement requirements at maturity. Our analysis is based on a convenient choice of reduced effective coordinates of magnitudes at liquidation for geometric dynamic programming. The price impact is transient over time and multiplicative, ensuring nonnegativity of underlying asset prices while maintaining an arbitrage-free model. The basic (log-)linear example is a Black–Scholes model with a relative price impact proportional to the volume of shares traded, where the transience for impact on log-prices is modelled like in Obizhaeva and Wang (J. Financ. Mark. 16:1–32, 2013) for nominal prices. More generally, we allow nonlinear price impact and resilience functions. The viscosity solutions describing the minimal superhedging price are governed by the transient character of the price impact and by the physical or cash settlement specifications. The pricing equations under illiquidity extend no-arbitrage pricing à la Black–Scholes for complete markets in a non-paradoxical way (cf. Çetin et al. (Finance Stoch. 14:317–341, 2010)) even without additional frictions, and can recover it in base cases.

期刊介绍:

The purpose of Finance and Stochastics is to provide a high standard publication forum for research

- in all areas of finance based on stochastic methods

- on specific topics in mathematics (in particular probability theory, statistics and stochastic analysis) motivated by the analysis of problems in finance.

Finance and Stochastics encompasses - but is not limited to - the following fields:

- theory and analysis of financial markets

- continuous time finance

- derivatives research

- insurance in relation to finance

- portfolio selection

- credit and market risks

- term structure models

- statistical and empirical financial studies based on advanced stochastic methods

- numerical and stochastic solution techniques for problems in finance

- intertemporal economics, uncertainty and information in relation to finance.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: