Philip T. Fliers, Abe de Jong, Bert S. van Stiphout-Kramer

{"title":"公司税、杠杆和投资:纳粹占领时期荷兰的证据","authors":"Philip T. Fliers, Abe de Jong, Bert S. van Stiphout-Kramer","doi":"10.1111/ehr.13331","DOIUrl":null,"url":null,"abstract":"<p>We examine the Netherlands around the Second World War, where the occupying Nazi regime overhauled the country's corporate tax regime and introduced a profit tax of 55 per cent. We estimate that the new tax regime cost investors at least 300 million guilders, an amount equivalent to 5 per cent of Dutch GDP in 1940. We demonstrate that the tax introduction changed the financing of Dutch businesses. In particular, we find strong evidence that debt financing increased because it provides a tax shelter. The changes in taxation also led to an after-tax reduction in the cost of debt, which had large real effects on firm investment. After the end of the war, firms with more leverage had higher capital expenditures.</p>","PeriodicalId":47868,"journal":{"name":"Economic History Review","volume":"77 4","pages":"1477-1508"},"PeriodicalIF":1.6000,"publicationDate":"2024-03-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ehr.13331","citationCount":"0","resultStr":"{\"title\":\"Corporate taxes, leverage, and investment: Evidence from Nazi-occupied Netherlands\",\"authors\":\"Philip T. Fliers, Abe de Jong, Bert S. van Stiphout-Kramer\",\"doi\":\"10.1111/ehr.13331\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We examine the Netherlands around the Second World War, where the occupying Nazi regime overhauled the country's corporate tax regime and introduced a profit tax of 55 per cent. We estimate that the new tax regime cost investors at least 300 million guilders, an amount equivalent to 5 per cent of Dutch GDP in 1940. We demonstrate that the tax introduction changed the financing of Dutch businesses. In particular, we find strong evidence that debt financing increased because it provides a tax shelter. The changes in taxation also led to an after-tax reduction in the cost of debt, which had large real effects on firm investment. After the end of the war, firms with more leverage had higher capital expenditures.</p>\",\"PeriodicalId\":47868,\"journal\":{\"name\":\"Economic History Review\",\"volume\":\"77 4\",\"pages\":\"1477-1508\"},\"PeriodicalIF\":1.6000,\"publicationDate\":\"2024-03-07\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ehr.13331\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Economic History Review\",\"FirstCategoryId\":\"98\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ehr.13331\",\"RegionNum\":1,\"RegionCategory\":\"历史学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Economic History Review","FirstCategoryId":"98","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ehr.13331","RegionNum":1,"RegionCategory":"历史学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Corporate taxes, leverage, and investment: Evidence from Nazi-occupied Netherlands

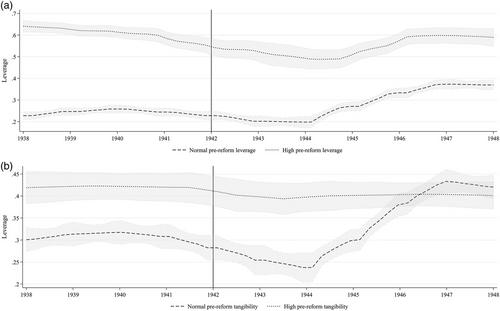

We examine the Netherlands around the Second World War, where the occupying Nazi regime overhauled the country's corporate tax regime and introduced a profit tax of 55 per cent. We estimate that the new tax regime cost investors at least 300 million guilders, an amount equivalent to 5 per cent of Dutch GDP in 1940. We demonstrate that the tax introduction changed the financing of Dutch businesses. In particular, we find strong evidence that debt financing increased because it provides a tax shelter. The changes in taxation also led to an after-tax reduction in the cost of debt, which had large real effects on firm investment. After the end of the war, firms with more leverage had higher capital expenditures.

期刊介绍:

The Economic History Review is published quarterly and each volume contains over 800 pages. It is an invaluable source of information and is available free to members of the Economic History Society. Publishing reviews of books, periodicals and information technology, The Review will keep anyone interested in economic and social history abreast of current developments in the subject. It aims at broad coverage of themes of economic and social change, including the intellectual, political and cultural implications of these changes.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: