{"title":"数据泄露通知法的意外成本:管理者囤积坏消息的证据","authors":"Ivan Obaydin, Limin Xu, Ralf Zurbruegg","doi":"10.1111/jbfa.12794","DOIUrl":null,"url":null,"abstract":"<p>We investigate how nonfinancial disclosure laws exacerbate agency issues in firms. Our analysis focuses on the staggered adoption of state-level notification laws that require firms to disclose data breaches. Our findings reveal that the introduction of these laws increases the risk of stock price crashes. Managers appear motivated to accumulate unfavorable news in an effort to prevent market overreactions associated with the mandatory disclosure of data breaches. Cross-sectional analyses also reveal that the impact is stronger when managers have a greater incentive, or greater ability, to hoard information. Our results highlight that nonfinancial disclosures can have unintended consequences for firm information asymmetries and potentially adverse market impacts in cases where the regulation is unable to consider all stakeholders.</p>","PeriodicalId":48106,"journal":{"name":"Journal of Business Finance & Accounting","volume":"51 9-10","pages":"2709-2736"},"PeriodicalIF":2.2000,"publicationDate":"2024-03-06","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12794","citationCount":"0","resultStr":"{\"title\":\"The unintended cost of data breach notification laws: Evidence from managerial bad news hoarding\",\"authors\":\"Ivan Obaydin, Limin Xu, Ralf Zurbruegg\",\"doi\":\"10.1111/jbfa.12794\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We investigate how nonfinancial disclosure laws exacerbate agency issues in firms. Our analysis focuses on the staggered adoption of state-level notification laws that require firms to disclose data breaches. Our findings reveal that the introduction of these laws increases the risk of stock price crashes. Managers appear motivated to accumulate unfavorable news in an effort to prevent market overreactions associated with the mandatory disclosure of data breaches. Cross-sectional analyses also reveal that the impact is stronger when managers have a greater incentive, or greater ability, to hoard information. Our results highlight that nonfinancial disclosures can have unintended consequences for firm information asymmetries and potentially adverse market impacts in cases where the regulation is unable to consider all stakeholders.</p>\",\"PeriodicalId\":48106,\"journal\":{\"name\":\"Journal of Business Finance & Accounting\",\"volume\":\"51 9-10\",\"pages\":\"2709-2736\"},\"PeriodicalIF\":2.2000,\"publicationDate\":\"2024-03-06\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12794\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Business Finance & Accounting\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12794\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Business Finance & Accounting","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12794","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

The unintended cost of data breach notification laws: Evidence from managerial bad news hoarding

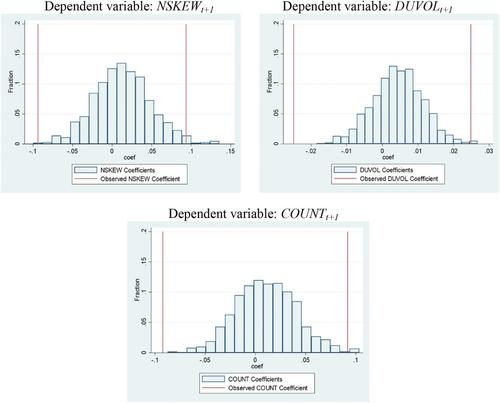

We investigate how nonfinancial disclosure laws exacerbate agency issues in firms. Our analysis focuses on the staggered adoption of state-level notification laws that require firms to disclose data breaches. Our findings reveal that the introduction of these laws increases the risk of stock price crashes. Managers appear motivated to accumulate unfavorable news in an effort to prevent market overreactions associated with the mandatory disclosure of data breaches. Cross-sectional analyses also reveal that the impact is stronger when managers have a greater incentive, or greater ability, to hoard information. Our results highlight that nonfinancial disclosures can have unintended consequences for firm information asymmetries and potentially adverse market impacts in cases where the regulation is unable to consider all stakeholders.

期刊介绍:

Journal of Business Finance and Accounting exists to publish high quality research papers in accounting, corporate finance, corporate governance and their interfaces. The interfaces are relevant in many areas such as financial reporting and communication, valuation, financial performance measurement and managerial reward and control structures. A feature of JBFA is that it recognises that informational problems are pervasive in financial markets and business organisations, and that accounting plays an important role in resolving such problems. JBFA welcomes both theoretical and empirical contributions. Nonetheless, theoretical papers should yield novel testable implications, and empirical papers should be theoretically well-motivated. The Editors view accounting and finance as being closely related to economics and, as a consequence, papers submitted will often have theoretical motivations that are grounded in economics. JBFA, however, also seeks papers that complement economics-based theorising with theoretical developments originating in other social science disciplines or traditions. While many papers in JBFA use econometric or related empirical methods, the Editors also welcome contributions that use other empirical research methods. Although the scope of JBFA is broad, it is not a suitable outlet for highly abstract mathematical papers, or empirical papers with inadequate theoretical motivation. Also, papers that study asset pricing, or the operations of financial markets, should have direct implications for one or more of preparers, regulators, users of financial statements, and corporate financial decision makers, or at least should have implications for the development of future research relevant to such users.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: