{"title":"美国对银行的审计:金融危机后是否有所改变?","authors":"Paul Tanyi, Jack Cathey","doi":"10.1057/s41261-024-00234-1","DOIUrl":null,"url":null,"abstract":"<p>The most recent financial crisis exposed to the auditors the risk associated with the audit engagement of their banking clients. Because many banking clients failed and investors suffered trillions of dollars in losses, auditors are now defendants in numerous shareholder and regulatory lawsuits. There is consensus that the financial crisis was created by an abundance of credit, excessive risk taking through complex financial instruments, weak corporate structures, and ineffective regulatory mechanisms. In this study, we examine how the financial crisis has affected the audit engagements of banking clients. We examine audit fees, audit report lag, and auditor changes before and after the financial crisis with respect to specific bank risks like credit risk, interest rate risk, and liquidity. Overall, we find that auditors are more responsive to bank risks in the post-financial crisis period compared to the pre-financial crisis period.</p>","PeriodicalId":15105,"journal":{"name":"Journal of Banking Regulation","volume":"56 1","pages":""},"PeriodicalIF":1.5000,"publicationDate":"2024-03-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"The audit of banks in the USA: Has it changed since the financial crisis?\",\"authors\":\"Paul Tanyi, Jack Cathey\",\"doi\":\"10.1057/s41261-024-00234-1\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The most recent financial crisis exposed to the auditors the risk associated with the audit engagement of their banking clients. Because many banking clients failed and investors suffered trillions of dollars in losses, auditors are now defendants in numerous shareholder and regulatory lawsuits. There is consensus that the financial crisis was created by an abundance of credit, excessive risk taking through complex financial instruments, weak corporate structures, and ineffective regulatory mechanisms. In this study, we examine how the financial crisis has affected the audit engagements of banking clients. We examine audit fees, audit report lag, and auditor changes before and after the financial crisis with respect to specific bank risks like credit risk, interest rate risk, and liquidity. Overall, we find that auditors are more responsive to bank risks in the post-financial crisis period compared to the pre-financial crisis period.</p>\",\"PeriodicalId\":15105,\"journal\":{\"name\":\"Journal of Banking Regulation\",\"volume\":\"56 1\",\"pages\":\"\"},\"PeriodicalIF\":1.5000,\"publicationDate\":\"2024-03-07\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Banking Regulation\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1057/s41261-024-00234-1\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Banking Regulation","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41261-024-00234-1","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

The audit of banks in the USA: Has it changed since the financial crisis?

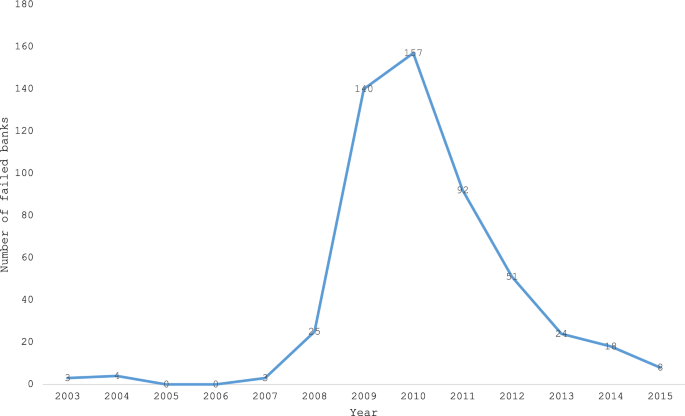

The most recent financial crisis exposed to the auditors the risk associated with the audit engagement of their banking clients. Because many banking clients failed and investors suffered trillions of dollars in losses, auditors are now defendants in numerous shareholder and regulatory lawsuits. There is consensus that the financial crisis was created by an abundance of credit, excessive risk taking through complex financial instruments, weak corporate structures, and ineffective regulatory mechanisms. In this study, we examine how the financial crisis has affected the audit engagements of banking clients. We examine audit fees, audit report lag, and auditor changes before and after the financial crisis with respect to specific bank risks like credit risk, interest rate risk, and liquidity. Overall, we find that auditors are more responsive to bank risks in the post-financial crisis period compared to the pre-financial crisis period.

期刊介绍:

Under the guidance of its highly respected Editors and an eminent and truly international Editorial Board?Journal of Banking Regulation?has established itself as one of the leading sources of authoritative and detailed information on all aspects of law and regulation affecting banking institutions.Journal of Banking Regulation?publishes in each quarterly issue detailed briefings analyses and updates which are of direct relevance to practitioners working in the field while meeting the highest intellectual standards.Journal of Banking Regulation?publishes the latest thinking and best practice on:Basel I II and IIIModels for banking supervisionInternational accounting standardsDeposit protectionEnforcement decisions in banking regulation and supervisionCross-border competition in banking servicesCorporate governance in banksHarmonisation in banking marketsSupervising credit riskAnti-money laundering legislation and regulationsMonetary integrationRisk capital and capital adequacySystemic risk in banking operationsCross-border regulationCross-border bank insolvencyModels for banking riskEssential reading for:central bankersbanking supervisorsfinancial regulatorsbankerscompliance officersheads of risk managementpolicy makersbank associationslawyers specialising in banking lawaccountantsinternal and external bank auditorsacademics and researchers

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: