OptionMetrics IvyDB 数据库中指数和股票期权隐含波动率的质量问题

IF 1.8

4区 经济学

Q2 BUSINESS, FINANCE

引用次数: 0

摘要

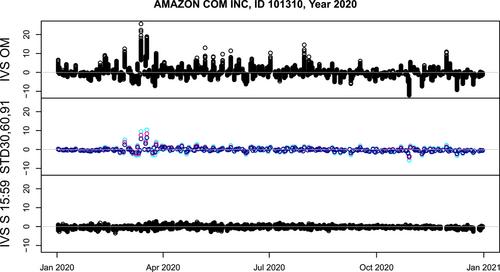

对于美国的股票和指数期权,OptionMetrics 记录的价格是下午 3:59,而不是之前文献中假设的下午 4:00。由此产生的与收盘价 1 分钟的时间差造成了隐含波动率价差的人为变化,并对整个市场的价差产生了强烈影响。这导致 COVID-19 大流行开始时的扭曲特别大。对于欧洲的指数期权,OptionMetrics 数据显示,即使原始期权价格与平价完全吻合,看跌-看涨平价的偏差也很大。最后,欧洲股票期权的隐含波动率显示出由于股息信息不正确而导致的特殊偏差群。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Quality issues of implied volatilities of index and stock options in the OptionMetrics IvyDB database

For stock and index options in the United States, OptionMetrics records prices at 3:59 p.m., not 4:00 p.m. as assumed in previous literature. The resulting 1-min time discrepancy with closing share prices creates artificial variability in implied volatility spreads and strongly affects market-wide spreads. It leads to particularly large distortions at the onset of the COVID-19 pandemic. For index options in Europe, OptionMetrics data show large deviations from put-call parity even though the original option prices match the parity exactly. Finally, the implied volatilities of stock options in Europe show clusters of exceptional deviations due to incorrect dividend information.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Journal of Futures Markets

BUSINESS, FINANCE-

CiteScore

3.70

自引率

15.80%

发文量

91

期刊介绍:

The Journal of Futures Markets chronicles the latest developments in financial futures and derivatives. It publishes timely, innovative articles written by leading finance academics and professionals. Coverage ranges from the highly practical to theoretical topics that include futures, derivatives, risk management and control, financial engineering, new financial instruments, hedging strategies, analysis of trading systems, legal, accounting, and regulatory issues, and portfolio optimization. This publication contains the very latest research from the top experts.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: