通过傅立叶变换估计制度切换扩散

IF 1.6

2区 数学

Q2 COMPUTER SCIENCE, THEORY & METHODS

引用次数: 0

摘要

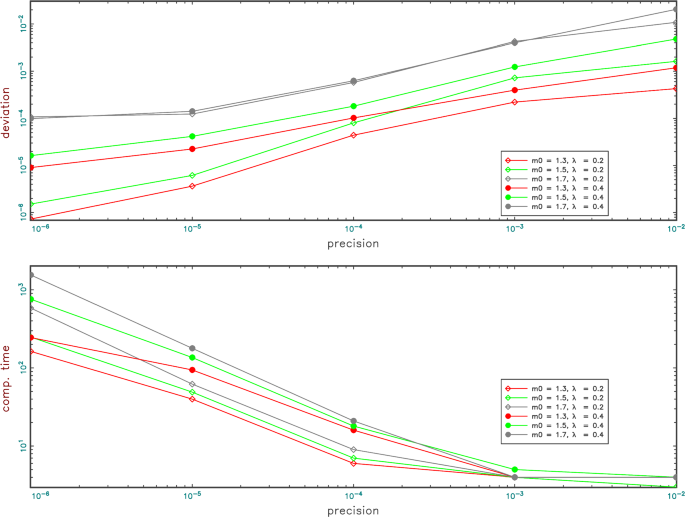

本文提出了一种对制度切换扩散进行最大似然估计的算法。该方法利用傅立叶变换对状态密度时间演化的福克-普朗克方程或前向科尔莫格罗方程组进行数值求解。蒙特卡罗模拟证实了这种方法在中等样本量时的理论预期一致性,以及它在经济学和生物学中某些具有中等数量状态和参数的制度转换扩散的实际可行性。对动物运动数据的应用是对所提算法的一个说明。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Estimation of regime-switching diffusions via Fourier transforms

In this article, an algorithm for maximum-likelihood estimation of regime-switching diffusions is proposed. The proposed approach uses a Fourier transform to numerically solve the system of Fokker–Planck or forward Kolmogorow equations for the temporal evolution of the state densities. Monte Carlo simulations confirm the theoretically expected consistency of this approach for moderate sample sizes and its practical feasibility for certain regime-switching diffusions used in economics and biology with moderate numbers of states and parameters. An application to animal movement data serves as an illustration of the proposed algorithm.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Statistics and Computing

数学-计算机:理论方法

CiteScore

3.20

自引率

4.50%

发文量

93

审稿时长

6-12 weeks

期刊介绍:

Statistics and Computing is a bi-monthly refereed journal which publishes papers covering the range of the interface between the statistical and computing sciences.

In particular, it addresses the use of statistical concepts in computing science, for example in machine learning, computer vision and data analytics, as well as the use of computers in data modelling, prediction and analysis. Specific topics which are covered include: techniques for evaluating analytically intractable problems such as bootstrap resampling, Markov chain Monte Carlo, sequential Monte Carlo, approximate Bayesian computation, search and optimization methods, stochastic simulation and Monte Carlo, graphics, computer environments, statistical approaches to software errors, information retrieval, machine learning, statistics of databases and database technology, huge data sets and big data analytics, computer algebra, graphical models, image processing, tomography, inverse problems and uncertainty quantification.

In addition, the journal contains original research reports, authoritative review papers, discussed papers, and occasional special issues on particular topics or carrying proceedings of relevant conferences. Statistics and Computing also publishes book review and software review sections.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: