{"title":"小企业对增值税激励措施的反应:来自韩国的证据","authors":"Dawoon Jung","doi":"10.1007/s10663-024-09607-1","DOIUrl":null,"url":null,"abstract":"<p>Using a comprehensive dataset of firm-level administrative value added tax (VAT) filings, this study investigates the behavioral responses of small firms to tax incentives. In South Korea, the standard VAT rate has remained at 10% since the introduction of the VAT system in 1977. However, small firms with a total annual revenue below 48 million KRW (approximately $46,000) benefit from a reduced VAT rate under the simplified VAT regime. This study uncovers an excess mass of firms in the revenue distribution precisely at the 48 million KRW threshold. Importantly, this response pattern varies depending on factors such as business sectors, the geographic location of firms and the year of their establishment. The disparities in tax liabilities at the threshold are identified as one of the potential factors driving these results.</p>","PeriodicalId":46526,"journal":{"name":"Empirica","volume":"111 1","pages":""},"PeriodicalIF":1.8000,"publicationDate":"2024-03-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"The response of small firms to VAT incentive: evidence from South Korea\",\"authors\":\"Dawoon Jung\",\"doi\":\"10.1007/s10663-024-09607-1\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Using a comprehensive dataset of firm-level administrative value added tax (VAT) filings, this study investigates the behavioral responses of small firms to tax incentives. In South Korea, the standard VAT rate has remained at 10% since the introduction of the VAT system in 1977. However, small firms with a total annual revenue below 48 million KRW (approximately $46,000) benefit from a reduced VAT rate under the simplified VAT regime. This study uncovers an excess mass of firms in the revenue distribution precisely at the 48 million KRW threshold. Importantly, this response pattern varies depending on factors such as business sectors, the geographic location of firms and the year of their establishment. The disparities in tax liabilities at the threshold are identified as one of the potential factors driving these results.</p>\",\"PeriodicalId\":46526,\"journal\":{\"name\":\"Empirica\",\"volume\":\"111 1\",\"pages\":\"\"},\"PeriodicalIF\":1.8000,\"publicationDate\":\"2024-03-05\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Empirica\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10663-024-09607-1\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Empirica","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10663-024-09607-1","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

The response of small firms to VAT incentive: evidence from South Korea

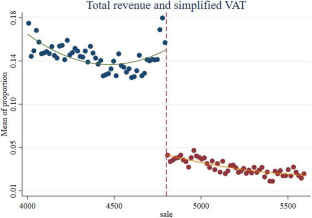

Using a comprehensive dataset of firm-level administrative value added tax (VAT) filings, this study investigates the behavioral responses of small firms to tax incentives. In South Korea, the standard VAT rate has remained at 10% since the introduction of the VAT system in 1977. However, small firms with a total annual revenue below 48 million KRW (approximately $46,000) benefit from a reduced VAT rate under the simplified VAT regime. This study uncovers an excess mass of firms in the revenue distribution precisely at the 48 million KRW threshold. Importantly, this response pattern varies depending on factors such as business sectors, the geographic location of firms and the year of their establishment. The disparities in tax liabilities at the threshold are identified as one of the potential factors driving these results.

期刊介绍:

Empirica is a peer-reviewed journal, which publishes original research of general interest to an international audience. Authors are invited to submit empirical papers in all areas of economics with a particular focus on European economies. Per January 2021, the editors also solicit descriptive papers on current or unexplored topics.

Founded in 1974, Empirica is the official journal of the Nationalökonomische Gesellschaft (Austrian Economic Association) and is published in cooperation with Austrian Institute of Economic Research (WIFO). The journal aims at a wide international audience and invites submissions from economists around the world.

Officially cited as: Empirica

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: