风险时代:商品的季节性和事件风险

IF 2.3

4区 经济学

Q2 BUSINESS, FINANCE

引用次数: 0

摘要

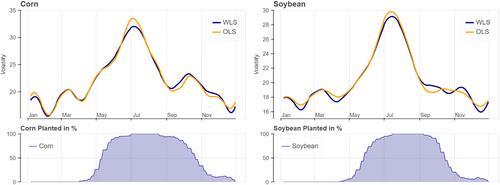

小麦、玉米和大豆的季节性风险是通过基于广义脊回归的新型季节性滤波器来建模的。然后,利用分量 GARCH 模型,将季节性风险与事件风险和短期风险动态结合起来。由此产生的模型是稳健的,能生成与作物周期相关的季节性模式,在样本外风险预测方面明显优于标准 GARCH(1,1)。研究结果与风险管理和投资组合构建相关。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Risky times: Seasonality and event risk of commodities

The seasonal risk of wheat, corn, and soybean is modeled by a novel seasonality filter based on a generalized ridge regression. Then, using a component GARCH model, seasonal risk is combined with event risk and a short-term risk dynamics. The resulting model is robust, generates seasonal patterns related to the crop cycle, and significantly outperforms the standard GARCH(1,1) in terms of out-of-sample risk prediction. Results are relevant for risk management and portfolio construction.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Journal of Futures Markets

BUSINESS, FINANCE-

CiteScore

3.70

自引率

15.80%

发文量

91

期刊介绍:

The Journal of Futures Markets chronicles the latest developments in financial futures and derivatives. It publishes timely, innovative articles written by leading finance academics and professionals. Coverage ranges from the highly practical to theoretical topics that include futures, derivatives, risk management and control, financial engineering, new financial instruments, hedging strategies, analysis of trading systems, legal, accounting, and regulatory issues, and portfolio optimization. This publication contains the very latest research from the top experts.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: