Guglielmo Maria Caporale, Silvia García Tapia, Luis Alberiko Gil-Alana

{"title":"税收收入的持续性:一些经合组织国家的证据","authors":"Guglielmo Maria Caporale, Silvia García Tapia, Luis Alberiko Gil-Alana","doi":"10.1007/s40953-024-00386-x","DOIUrl":null,"url":null,"abstract":"<p>This paper examines persistence in tax revenues in a set of 21 OECD countries over the period 1965–2021 using long-range dependence techniques based on fractional integration. The results imply that there are only a few cases of mean reversion: one for total revenue (Switzerland); three for VAT (Belgium, Italy, and Spain), and six for tax on income (Austria, Belgium, Finland, Spain, Sweden and USA). The analysis is also carried out for inflation in the same set of countries. Again the I(1) hypothesis cannot be rejected in most cases, mean reversion only occurring in Korea, Iceland, Norway and Sweden. However, stronger evidence of mean reversion is found for the differences between the three original tax series and inflation compared to the tax series themselves, which points to the existence of a linkage between taxation and inflation, especially in the case of VAT and tax on income.</p>","PeriodicalId":42219,"journal":{"name":"JOURNAL OF QUANTITATIVE ECONOMICS","volume":"32 1","pages":""},"PeriodicalIF":0.7000,"publicationDate":"2024-02-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Persistence in Tax Revenues: Evidence from Some OECD Countries\",\"authors\":\"Guglielmo Maria Caporale, Silvia García Tapia, Luis Alberiko Gil-Alana\",\"doi\":\"10.1007/s40953-024-00386-x\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper examines persistence in tax revenues in a set of 21 OECD countries over the period 1965–2021 using long-range dependence techniques based on fractional integration. The results imply that there are only a few cases of mean reversion: one for total revenue (Switzerland); three for VAT (Belgium, Italy, and Spain), and six for tax on income (Austria, Belgium, Finland, Spain, Sweden and USA). The analysis is also carried out for inflation in the same set of countries. Again the I(1) hypothesis cannot be rejected in most cases, mean reversion only occurring in Korea, Iceland, Norway and Sweden. However, stronger evidence of mean reversion is found for the differences between the three original tax series and inflation compared to the tax series themselves, which points to the existence of a linkage between taxation and inflation, especially in the case of VAT and tax on income.</p>\",\"PeriodicalId\":42219,\"journal\":{\"name\":\"JOURNAL OF QUANTITATIVE ECONOMICS\",\"volume\":\"32 1\",\"pages\":\"\"},\"PeriodicalIF\":0.7000,\"publicationDate\":\"2024-02-19\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"JOURNAL OF QUANTITATIVE ECONOMICS\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://doi.org/10.1007/s40953-024-00386-x\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"JOURNAL OF QUANTITATIVE ECONOMICS","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s40953-024-00386-x","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Persistence in Tax Revenues: Evidence from Some OECD Countries

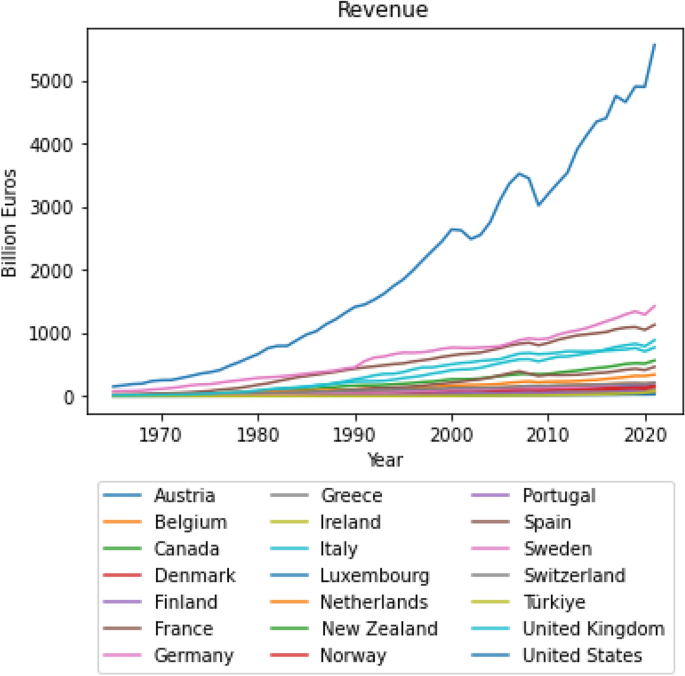

This paper examines persistence in tax revenues in a set of 21 OECD countries over the period 1965–2021 using long-range dependence techniques based on fractional integration. The results imply that there are only a few cases of mean reversion: one for total revenue (Switzerland); three for VAT (Belgium, Italy, and Spain), and six for tax on income (Austria, Belgium, Finland, Spain, Sweden and USA). The analysis is also carried out for inflation in the same set of countries. Again the I(1) hypothesis cannot be rejected in most cases, mean reversion only occurring in Korea, Iceland, Norway and Sweden. However, stronger evidence of mean reversion is found for the differences between the three original tax series and inflation compared to the tax series themselves, which points to the existence of a linkage between taxation and inflation, especially in the case of VAT and tax on income.

期刊介绍:

The Journal of Quantitative Economics (JQEC) is a refereed journal of the Indian Econometric Society (TIES). It solicits quantitative papers with basic or applied research orientation in all sub-fields of Economics that employ rigorous theoretical, empirical and experimental methods. The Journal also encourages Short Papers and Review Articles. Innovative and fundamental papers that focus on various facets of Economics of the Emerging Market and Developing Economies are particularly welcome. With the help of an international Editorial board and carefully selected referees, it aims to minimize the time taken to complete the review process while preserving the quality of the articles published.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: