{"title":"不确定情况下的风险度量框架","authors":"Tolulope Fadina, Yang Liu, Ruodu Wang","doi":"10.1007/s00780-024-00528-2","DOIUrl":null,"url":null,"abstract":"<p>A risk analyst assesses potential financial losses based on multiple sources of information. Often, the assessment does not only depend on the specification of the loss random variable, but also on various economic scenarios. Motivated by this observation, we design a unified axiomatic framework for risk evaluation principles which quantify jointly a loss random variable and a set of plausible probabilities. We call such an evaluation principle a generalised risk measure. We present a series of relevant theoretical results. The worst-case, coherent and robust generalised risk measures are characterised via different sets of intuitive axioms. We establish the equivalence between a few natural forms of law-invariance in our framework, and the technical subtlety therein reveals a sharp contrast between our framework and the traditional one. Moreover, coherence and strong law-invariance are derived from a combination of other conditions, which provides additional support for coherent risk measures such as expected shortfall over value-at-risk, a relevant issue for risk management practice.</p>","PeriodicalId":50447,"journal":{"name":"Finance and Stochastics","volume":"255 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2024-02-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"A framework for measures of risk under uncertainty\",\"authors\":\"Tolulope Fadina, Yang Liu, Ruodu Wang\",\"doi\":\"10.1007/s00780-024-00528-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>A risk analyst assesses potential financial losses based on multiple sources of information. Often, the assessment does not only depend on the specification of the loss random variable, but also on various economic scenarios. Motivated by this observation, we design a unified axiomatic framework for risk evaluation principles which quantify jointly a loss random variable and a set of plausible probabilities. We call such an evaluation principle a generalised risk measure. We present a series of relevant theoretical results. The worst-case, coherent and robust generalised risk measures are characterised via different sets of intuitive axioms. We establish the equivalence between a few natural forms of law-invariance in our framework, and the technical subtlety therein reveals a sharp contrast between our framework and the traditional one. Moreover, coherence and strong law-invariance are derived from a combination of other conditions, which provides additional support for coherent risk measures such as expected shortfall over value-at-risk, a relevant issue for risk management practice.</p>\",\"PeriodicalId\":50447,\"journal\":{\"name\":\"Finance and Stochastics\",\"volume\":\"255 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2024-02-07\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Finance and Stochastics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s00780-024-00528-2\",\"RegionNum\":2,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Finance and Stochastics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s00780-024-00528-2","RegionNum":2,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

A framework for measures of risk under uncertainty

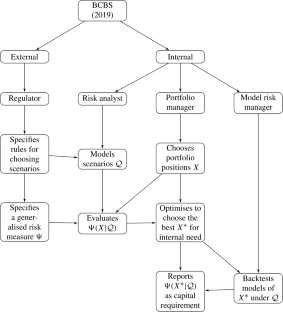

A risk analyst assesses potential financial losses based on multiple sources of information. Often, the assessment does not only depend on the specification of the loss random variable, but also on various economic scenarios. Motivated by this observation, we design a unified axiomatic framework for risk evaluation principles which quantify jointly a loss random variable and a set of plausible probabilities. We call such an evaluation principle a generalised risk measure. We present a series of relevant theoretical results. The worst-case, coherent and robust generalised risk measures are characterised via different sets of intuitive axioms. We establish the equivalence between a few natural forms of law-invariance in our framework, and the technical subtlety therein reveals a sharp contrast between our framework and the traditional one. Moreover, coherence and strong law-invariance are derived from a combination of other conditions, which provides additional support for coherent risk measures such as expected shortfall over value-at-risk, a relevant issue for risk management practice.

期刊介绍:

The purpose of Finance and Stochastics is to provide a high standard publication forum for research

- in all areas of finance based on stochastic methods

- on specific topics in mathematics (in particular probability theory, statistics and stochastic analysis) motivated by the analysis of problems in finance.

Finance and Stochastics encompasses - but is not limited to - the following fields:

- theory and analysis of financial markets

- continuous time finance

- derivatives research

- insurance in relation to finance

- portfolio selection

- credit and market risks

- term structure models

- statistical and empirical financial studies based on advanced stochastic methods

- numerical and stochastic solution techniques for problems in finance

- intertemporal economics, uncertainty and information in relation to finance.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: