{"title":"首次公开募股后主导风险投资公司的参与、与合并相关的诉讼和目标公司的估值","authors":"Anup Basnet, Thomas Walker","doi":"10.1111/1467-8551.12803","DOIUrl":null,"url":null,"abstract":"<p>Venture capital firms (VCs) provide certification and monitoring services to the initial public offering (IPO) companies they finance, as has been well documented in the academic literature. Yet, there are few studies that explore what role – if any – VCs play when an IPO company is subsequently acquired, particularly if that acquisition is legally contested. Using a sample of 721 merger and acquisition (M&A) offers for US VC-backed IPO companies, announced between 1996 and 2018, we find that a takeover bid that occurs in the presence of the lead VC commands a higher target firm valuation and is less likely to be legally contested than a bid for a company from which the lead VC has already exited. In addition, companies in which the lead VC is present enjoy higher stock-price returns in response to M&A announcements. Our results provide new evidence regarding VC certification and monitoring – including its role as a litigation deterrent – long after the IPO.</p>","PeriodicalId":48342,"journal":{"name":"British Journal of Management","volume":"35 4","pages":"1961-1979"},"PeriodicalIF":4.5000,"publicationDate":"2024-02-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1467-8551.12803","citationCount":"0","resultStr":"{\"title\":\"Post-IPO lead venture capital firm involvement, merger-related litigation and target firm valuation\",\"authors\":\"Anup Basnet, Thomas Walker\",\"doi\":\"10.1111/1467-8551.12803\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Venture capital firms (VCs) provide certification and monitoring services to the initial public offering (IPO) companies they finance, as has been well documented in the academic literature. Yet, there are few studies that explore what role – if any – VCs play when an IPO company is subsequently acquired, particularly if that acquisition is legally contested. Using a sample of 721 merger and acquisition (M&A) offers for US VC-backed IPO companies, announced between 1996 and 2018, we find that a takeover bid that occurs in the presence of the lead VC commands a higher target firm valuation and is less likely to be legally contested than a bid for a company from which the lead VC has already exited. In addition, companies in which the lead VC is present enjoy higher stock-price returns in response to M&A announcements. Our results provide new evidence regarding VC certification and monitoring – including its role as a litigation deterrent – long after the IPO.</p>\",\"PeriodicalId\":48342,\"journal\":{\"name\":\"British Journal of Management\",\"volume\":\"35 4\",\"pages\":\"1961-1979\"},\"PeriodicalIF\":4.5000,\"publicationDate\":\"2024-02-08\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1467-8551.12803\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"British Journal of Management\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1467-8551.12803\",\"RegionNum\":2,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"British Journal of Management","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1467-8551.12803","RegionNum":2,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS","Score":null,"Total":0}

Post-IPO lead venture capital firm involvement, merger-related litigation and target firm valuation

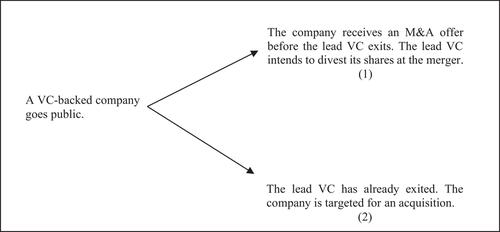

Venture capital firms (VCs) provide certification and monitoring services to the initial public offering (IPO) companies they finance, as has been well documented in the academic literature. Yet, there are few studies that explore what role – if any – VCs play when an IPO company is subsequently acquired, particularly if that acquisition is legally contested. Using a sample of 721 merger and acquisition (M&A) offers for US VC-backed IPO companies, announced between 1996 and 2018, we find that a takeover bid that occurs in the presence of the lead VC commands a higher target firm valuation and is less likely to be legally contested than a bid for a company from which the lead VC has already exited. In addition, companies in which the lead VC is present enjoy higher stock-price returns in response to M&A announcements. Our results provide new evidence regarding VC certification and monitoring – including its role as a litigation deterrent – long after the IPO.

期刊介绍:

The British Journal of Management provides a valuable outlet for research and scholarship on management-orientated themes and topics. It publishes articles of a multi-disciplinary and interdisciplinary nature as well as empirical research from within traditional disciplines and managerial functions. With contributions from around the globe, the journal includes articles across the full range of business and management disciplines. A subscription to British Journal of Management includes International Journal of Management Reviews, also published on behalf of the British Academy of Management.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: