{"title":"基于残差的非参数方差比无协整检验","authors":"Karsten Reichold","doi":"10.1111/jtsa.12734","DOIUrl":null,"url":null,"abstract":"<p>It is prominently stated in the literature that local asymptotic power properties serve as a useful indicator for the performance of residual-based no-cointegration tests in finite samples. However, this article comes to an opposing conclusion. In particular, we show that Breitung's (2002, Journal of Econometrics 108, 343–363) nonparameteric variance ratio unit root test applied to regression residuals serves as a no-cointegration test but is inferior to its competitors from a local asymptotic power perspective. Nevertheless, in finite samples, the variance ratio test has good size properties, competitive power, and the convenience of being tuning parameter free. In general, we find that short-run dynamics in the error process can have considerably larger detrimental effects on the performance of residual-based no-cointegration tests in finite samples than changes in the only nuisance parameter affecting local asymptotic power of the tests. The results serve as a warning for practitioners and lead to interesting directions for future research.</p>","PeriodicalId":49973,"journal":{"name":"Journal of Time Series Analysis","volume":"45 5","pages":"847-856"},"PeriodicalIF":1.0000,"publicationDate":"2024-02-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jtsa.12734","citationCount":"0","resultStr":"{\"title\":\"A residual-based nonparametric variance ratio no-cointegration test\",\"authors\":\"Karsten Reichold\",\"doi\":\"10.1111/jtsa.12734\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>It is prominently stated in the literature that local asymptotic power properties serve as a useful indicator for the performance of residual-based no-cointegration tests in finite samples. However, this article comes to an opposing conclusion. In particular, we show that Breitung's (2002, Journal of Econometrics 108, 343–363) nonparameteric variance ratio unit root test applied to regression residuals serves as a no-cointegration test but is inferior to its competitors from a local asymptotic power perspective. Nevertheless, in finite samples, the variance ratio test has good size properties, competitive power, and the convenience of being tuning parameter free. In general, we find that short-run dynamics in the error process can have considerably larger detrimental effects on the performance of residual-based no-cointegration tests in finite samples than changes in the only nuisance parameter affecting local asymptotic power of the tests. The results serve as a warning for practitioners and lead to interesting directions for future research.</p>\",\"PeriodicalId\":49973,\"journal\":{\"name\":\"Journal of Time Series Analysis\",\"volume\":\"45 5\",\"pages\":\"847-856\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2024-02-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jtsa.12734\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Time Series Analysis\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jtsa.12734\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Time Series Analysis","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jtsa.12734","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

A residual-based nonparametric variance ratio no-cointegration test

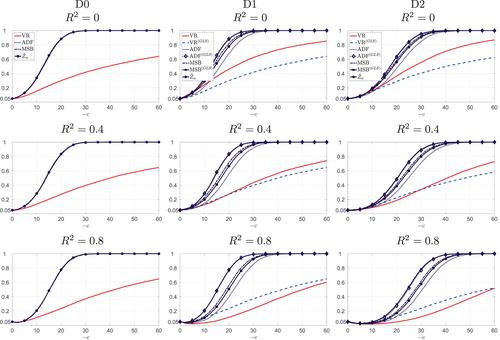

It is prominently stated in the literature that local asymptotic power properties serve as a useful indicator for the performance of residual-based no-cointegration tests in finite samples. However, this article comes to an opposing conclusion. In particular, we show that Breitung's (2002, Journal of Econometrics 108, 343–363) nonparameteric variance ratio unit root test applied to regression residuals serves as a no-cointegration test but is inferior to its competitors from a local asymptotic power perspective. Nevertheless, in finite samples, the variance ratio test has good size properties, competitive power, and the convenience of being tuning parameter free. In general, we find that short-run dynamics in the error process can have considerably larger detrimental effects on the performance of residual-based no-cointegration tests in finite samples than changes in the only nuisance parameter affecting local asymptotic power of the tests. The results serve as a warning for practitioners and lead to interesting directions for future research.

期刊介绍:

During the last 30 years Time Series Analysis has become one of the most important and widely used branches of Mathematical Statistics. Its fields of application range from neurophysiology to astrophysics and it covers such well-known areas as economic forecasting, study of biological data, control systems, signal processing and communications and vibrations engineering.

The Journal of Time Series Analysis started in 1980, has since become the leading journal in its field, publishing papers on both fundamental theory and applications, as well as review papers dealing with recent advances in major areas of the subject and short communications on theoretical developments. The editorial board consists of many of the world''s leading experts in Time Series Analysis.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: