{"title":"家庭住房价格结构模型中的贝叶斯推论","authors":"Gian Maria Tomat","doi":"10.1007/s40797-023-00259-x","DOIUrl":null,"url":null,"abstract":"<p>We review the implications of an intertemporal representative consumer model for the analysis of housing prices, describing the choice between non-housing and housing consumption, and provide an explanation for the excess return of housing over the riskless rate based on weakly separable preferences. Further considerations are presented regarding the role of liquidity constraints. A Bayesian structural vector autoregression predicts relations between real rent growth, interest rates and housing prices consistently with the representative consumer model. The orthogonalized impulse response functions show, that housing prices are relatively unresponsive to shocks to fundamental value. The logarithmic rent/price ratio increases or does not significantly change following shocks to the real rent growth and relative bill rates. The dynamics of housing prices over the business cycle is mainly determined by financial factors. A shock to the natural logarithm of the rent/price ratio does not have significant predictive properties for subsequent real rent growth and relative bill rates. Moreover, the logarithmic rent/price ratio is a highly persistent variable displaying momentum and long term reversal.</p>","PeriodicalId":43048,"journal":{"name":"Italian Economic Journal","volume":"162 1","pages":""},"PeriodicalIF":1.2000,"publicationDate":"2024-01-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Bayesian Inference in a Structural Model of Family Home Prices\",\"authors\":\"Gian Maria Tomat\",\"doi\":\"10.1007/s40797-023-00259-x\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We review the implications of an intertemporal representative consumer model for the analysis of housing prices, describing the choice between non-housing and housing consumption, and provide an explanation for the excess return of housing over the riskless rate based on weakly separable preferences. Further considerations are presented regarding the role of liquidity constraints. A Bayesian structural vector autoregression predicts relations between real rent growth, interest rates and housing prices consistently with the representative consumer model. The orthogonalized impulse response functions show, that housing prices are relatively unresponsive to shocks to fundamental value. The logarithmic rent/price ratio increases or does not significantly change following shocks to the real rent growth and relative bill rates. The dynamics of housing prices over the business cycle is mainly determined by financial factors. A shock to the natural logarithm of the rent/price ratio does not have significant predictive properties for subsequent real rent growth and relative bill rates. Moreover, the logarithmic rent/price ratio is a highly persistent variable displaying momentum and long term reversal.</p>\",\"PeriodicalId\":43048,\"journal\":{\"name\":\"Italian Economic Journal\",\"volume\":\"162 1\",\"pages\":\"\"},\"PeriodicalIF\":1.2000,\"publicationDate\":\"2024-01-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Italian Economic Journal\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s40797-023-00259-x\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Italian Economic Journal","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s40797-023-00259-x","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Bayesian Inference in a Structural Model of Family Home Prices

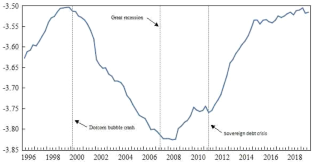

We review the implications of an intertemporal representative consumer model for the analysis of housing prices, describing the choice between non-housing and housing consumption, and provide an explanation for the excess return of housing over the riskless rate based on weakly separable preferences. Further considerations are presented regarding the role of liquidity constraints. A Bayesian structural vector autoregression predicts relations between real rent growth, interest rates and housing prices consistently with the representative consumer model. The orthogonalized impulse response functions show, that housing prices are relatively unresponsive to shocks to fundamental value. The logarithmic rent/price ratio increases or does not significantly change following shocks to the real rent growth and relative bill rates. The dynamics of housing prices over the business cycle is mainly determined by financial factors. A shock to the natural logarithm of the rent/price ratio does not have significant predictive properties for subsequent real rent growth and relative bill rates. Moreover, the logarithmic rent/price ratio is a highly persistent variable displaying momentum and long term reversal.

期刊介绍:

Italian Economic Journal (ItEJ) is the official peer-reviewed journal of the Italian Economic Association. ItEJ publishes scientific articles in all areas of economics and economic policy, providing a scholarly, international forum for all methodological approaches and schools of thought. In particular, ItEJ aims at encouraging and disseminating high-quality research on the Italian and the European economy. To fulfill this aim, the journal welcomes applied, institutional and theoretical papers on relevant and timely issues concerning the European and Italian economic debate.ItEJ merges the Rivista Italiana degli Economisti (RIE), the journal founded by the Italian Economic Association in 1996, with the Giornale degli Economisti (GdE), founded in 1875 and enriched by contributions from renowned economists, including Amoroso, Black, Barone, De Viti de Marco, Edgeworth, Einaudi, Modigliani, Pantaleoni, Pareto, Slutsky, Tinbergen and Walras.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: