{"title":"无保险市场和广泛劳动力供给反应经济中的最优劳动收入税和资产分配","authors":"Takao Kataoka, Yoshihiro Takamatsu","doi":"10.1007/s10797-023-09819-4","DOIUrl":null,"url":null,"abstract":"<p>We examine the effects of stationary nonlinear labor income tax rules in a dynamic economy, considering extensive marginal labor-leisure choices and uninsured idiosyncratic shocks on labor productivity and labor disutility. The labor income tax rule has significant implications for households’ savings behavior and asset distribution over the long-run. We derive a optimal stationary tax rules as a natural extension of optimal participation tax rule in the static models. Through numerical simulations, two main findings emerge: (i) The current optimal tax rule, aimed at maximizing welfare based on the present asset distribution level, supports in-work benefits for low-income workers as a static extensive margin model. While this policy temporarily enhances welfare, it leads to a decline in capital accumulation and a decrease in average utility flow over time. (ii) The long-run optimal tax rule, optimizing welfare when the asset distribution reaches a stationary state, exhibits less progressivity and initially worsens welfare temporarily. However, it eventually improves the average utility flow in the long-run. The long-term consequences of households’ saving behavior and asset distribution mitigate the attractiveness of in-work benefit policies. By shedding light on the trade-offs between short-term welfare gains and long-term utility improvements, this study provides insights into designing effective labor income tax policies in a dynamic economic context.</p>","PeriodicalId":47518,"journal":{"name":"International Tax and Public Finance","volume":"28 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2024-01-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Optimal labor income taxation and asset distribution in an economy with no insurance market and extensive labor supply responses\",\"authors\":\"Takao Kataoka, Yoshihiro Takamatsu\",\"doi\":\"10.1007/s10797-023-09819-4\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We examine the effects of stationary nonlinear labor income tax rules in a dynamic economy, considering extensive marginal labor-leisure choices and uninsured idiosyncratic shocks on labor productivity and labor disutility. The labor income tax rule has significant implications for households’ savings behavior and asset distribution over the long-run. We derive a optimal stationary tax rules as a natural extension of optimal participation tax rule in the static models. Through numerical simulations, two main findings emerge: (i) The current optimal tax rule, aimed at maximizing welfare based on the present asset distribution level, supports in-work benefits for low-income workers as a static extensive margin model. While this policy temporarily enhances welfare, it leads to a decline in capital accumulation and a decrease in average utility flow over time. (ii) The long-run optimal tax rule, optimizing welfare when the asset distribution reaches a stationary state, exhibits less progressivity and initially worsens welfare temporarily. However, it eventually improves the average utility flow in the long-run. The long-term consequences of households’ saving behavior and asset distribution mitigate the attractiveness of in-work benefit policies. By shedding light on the trade-offs between short-term welfare gains and long-term utility improvements, this study provides insights into designing effective labor income tax policies in a dynamic economic context.</p>\",\"PeriodicalId\":47518,\"journal\":{\"name\":\"International Tax and Public Finance\",\"volume\":\"28 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2024-01-08\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Tax and Public Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10797-023-09819-4\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Tax and Public Finance","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10797-023-09819-4","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Optimal labor income taxation and asset distribution in an economy with no insurance market and extensive labor supply responses

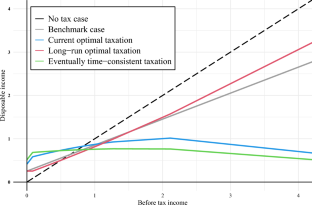

We examine the effects of stationary nonlinear labor income tax rules in a dynamic economy, considering extensive marginal labor-leisure choices and uninsured idiosyncratic shocks on labor productivity and labor disutility. The labor income tax rule has significant implications for households’ savings behavior and asset distribution over the long-run. We derive a optimal stationary tax rules as a natural extension of optimal participation tax rule in the static models. Through numerical simulations, two main findings emerge: (i) The current optimal tax rule, aimed at maximizing welfare based on the present asset distribution level, supports in-work benefits for low-income workers as a static extensive margin model. While this policy temporarily enhances welfare, it leads to a decline in capital accumulation and a decrease in average utility flow over time. (ii) The long-run optimal tax rule, optimizing welfare when the asset distribution reaches a stationary state, exhibits less progressivity and initially worsens welfare temporarily. However, it eventually improves the average utility flow in the long-run. The long-term consequences of households’ saving behavior and asset distribution mitigate the attractiveness of in-work benefit policies. By shedding light on the trade-offs between short-term welfare gains and long-term utility improvements, this study provides insights into designing effective labor income tax policies in a dynamic economic context.

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: