Paolo Roffia, María Mar Benavides, Augustin Carrilero

{"title":"中小企业的成本会计实践:在动荡年代阻碍或迸发其实施的账龄责任和其他因素","authors":"Paolo Roffia, María Mar Benavides, Augustin Carrilero","doi":"10.1007/s11365-023-00938-2","DOIUrl":null,"url":null,"abstract":"<p>This study aimed to investigate the level of cost accounting (CA) implementation in small- and medium-sized enterprises (SMEs). CA is a management accounting tool whose application in small companies has always been difficult. Nevertheless, academicians and practitioners recommend CA implementation in SMEs, especially because of the deep market instability, competitive pressure, and margin erosion that have occurred following the COVID-19 pandemic and 2022 European war scenario. Company size influences CA implementation; however, it is not the only influencing factor and perhaps not even the most important. To investigate the barriers to the adoption of CA and which conditions or actions can remove these barriers, leveraging from the contingency theory, a questionnaire was sent out in July 2022 to limited liability SMEs operating in the manufacturing, construction, and distribution macro-sectors in Verona and Vicenza provinces (Italy). Respondents answered a set of questions regarding CA implementation in their SMEs as of July 2022. Using a multivariate regression model to analyze data from the 120 questionnaires received, we found that lack of resources, limited training and skills, firm age, and the presence of the founder in the firm had a negative influence on CA implementation in SMEs. The low level of CA implementation was also associated with its supposed inefficiency, uselessness, and unsuitability for business. The effect of company size on CA implementation was not statistically significant. Despite this study’s limitations regarding the sample and period considered, we believe that it contributes to both academic debates and practice by illustrating the limiting factors and ways in which CA implementation can be fostered in SMEs in turbulent years.</p>","PeriodicalId":48058,"journal":{"name":"International Entrepreneurship and Management Journal","volume":"27 1","pages":""},"PeriodicalIF":3.9000,"publicationDate":"2024-01-03","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Cost accounting practices in SMEs: liability of age and other factors that hinder or burst its implementation in turbulent years\",\"authors\":\"Paolo Roffia, María Mar Benavides, Augustin Carrilero\",\"doi\":\"10.1007/s11365-023-00938-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study aimed to investigate the level of cost accounting (CA) implementation in small- and medium-sized enterprises (SMEs). CA is a management accounting tool whose application in small companies has always been difficult. Nevertheless, academicians and practitioners recommend CA implementation in SMEs, especially because of the deep market instability, competitive pressure, and margin erosion that have occurred following the COVID-19 pandemic and 2022 European war scenario. Company size influences CA implementation; however, it is not the only influencing factor and perhaps not even the most important. To investigate the barriers to the adoption of CA and which conditions or actions can remove these barriers, leveraging from the contingency theory, a questionnaire was sent out in July 2022 to limited liability SMEs operating in the manufacturing, construction, and distribution macro-sectors in Verona and Vicenza provinces (Italy). Respondents answered a set of questions regarding CA implementation in their SMEs as of July 2022. Using a multivariate regression model to analyze data from the 120 questionnaires received, we found that lack of resources, limited training and skills, firm age, and the presence of the founder in the firm had a negative influence on CA implementation in SMEs. The low level of CA implementation was also associated with its supposed inefficiency, uselessness, and unsuitability for business. The effect of company size on CA implementation was not statistically significant. Despite this study’s limitations regarding the sample and period considered, we believe that it contributes to both academic debates and practice by illustrating the limiting factors and ways in which CA implementation can be fostered in SMEs in turbulent years.</p>\",\"PeriodicalId\":48058,\"journal\":{\"name\":\"International Entrepreneurship and Management Journal\",\"volume\":\"27 1\",\"pages\":\"\"},\"PeriodicalIF\":3.9000,\"publicationDate\":\"2024-01-03\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Entrepreneurship and Management Journal\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://doi.org/10.1007/s11365-023-00938-2\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Entrepreneurship and Management Journal","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s11365-023-00938-2","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS","Score":null,"Total":0}

引用次数: 0

摘要

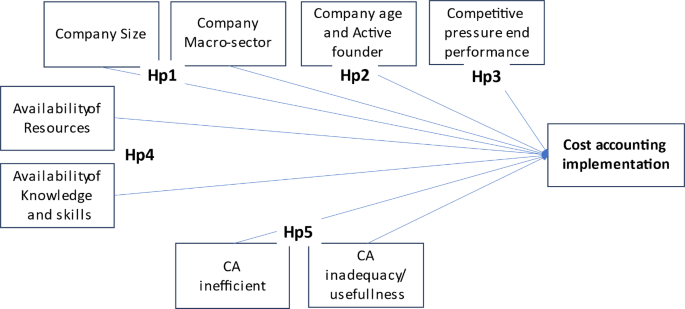

本研究旨在调查中小型企业(SMEs)实施成本会计(CA)的水平。成本会计是一种管理会计工具,在小型企业中的应用一直很困难。尽管如此,学术界和实务界仍建议中小企业实施成本会计,特别是因为 COVID-19 大流行和 2022 年欧洲战争之后,市场极不稳定,竞争压力大,利润被侵蚀。公司规模会影响 CA 的实施,但它不是唯一的影响因素,甚至可能不是最重要的影响因素。为了调查采用 CA 的障碍,以及哪些条件或行动可以消除这些障碍,我们利用权变理论,于 2022 年 7 月向维罗纳省和维琴察省(意大利)从事制造业、建筑业和分销业的有限责任中小企业发出了一份调查问卷。受访者回答了一系列有关截至 2022 年 7 月其中小企业实施 CA 的问题。我们使用多元回归模型对收到的 120 份问卷中的数据进行了分析,发现缺乏资源、培训和技能有限、企业年龄以及企业创始人的存在对中小企业实施 CA 有负面影响。CA实施水平低还与CA的低效、无用和不适合业务有关。公司规模对 CA 实施的影响在统计上并不显著。尽管这项研究在样本和研究时间方面存在局限性,但我们相信,它通过说明限制因素以及在动荡年代促进中小型企业实施 CA 的方法,为学术讨论和实践做出了贡献。

Cost accounting practices in SMEs: liability of age and other factors that hinder or burst its implementation in turbulent years

This study aimed to investigate the level of cost accounting (CA) implementation in small- and medium-sized enterprises (SMEs). CA is a management accounting tool whose application in small companies has always been difficult. Nevertheless, academicians and practitioners recommend CA implementation in SMEs, especially because of the deep market instability, competitive pressure, and margin erosion that have occurred following the COVID-19 pandemic and 2022 European war scenario. Company size influences CA implementation; however, it is not the only influencing factor and perhaps not even the most important. To investigate the barriers to the adoption of CA and which conditions or actions can remove these barriers, leveraging from the contingency theory, a questionnaire was sent out in July 2022 to limited liability SMEs operating in the manufacturing, construction, and distribution macro-sectors in Verona and Vicenza provinces (Italy). Respondents answered a set of questions regarding CA implementation in their SMEs as of July 2022. Using a multivariate regression model to analyze data from the 120 questionnaires received, we found that lack of resources, limited training and skills, firm age, and the presence of the founder in the firm had a negative influence on CA implementation in SMEs. The low level of CA implementation was also associated with its supposed inefficiency, uselessness, and unsuitability for business. The effect of company size on CA implementation was not statistically significant. Despite this study’s limitations regarding the sample and period considered, we believe that it contributes to both academic debates and practice by illustrating the limiting factors and ways in which CA implementation can be fostered in SMEs in turbulent years.

期刊介绍:

The International Entrepreneurship and Management Journal (IEMJ) publishes high quality manuscripts dealing with entrepreneurship, broadly defined, and the management of entrepreneurial organizations. The journal will expand the study of entrepreneurship and management by publishing innovative articles based on different perspectives using a variety of methodological approaches and showing the practical implications of the research for its readership. IEMJ is unique; providing a multi-disciplinary forum for researchers, scholars, consultants, entrepreneurs, businessmen, managers and practitioners in the field of entrepreneurship. The journal covers the relationship between management and entrepreneurship including both conceptual and empirical papers, leading to an improvement in the understanding of international entrepreneurial perspectives of the organisations concerned. Entrepreneurial studies are important in creating new economic activity that in turn increases innovation, employment, economic wealth and growth. The journal focuses on the diverse and complex characteristics of entrepreneurship in SMEs and large companies in local, regional, national or international markets that lead to competitiveness in the face of the effects of globalization. Though preference will be given to manuscripts that are international in scope, papers focused on domestic contexts and issues are welcome also, in order to facilitate the sharing of knowledge and potential generalizability of findings worldwide. IEMJ will publish original papers which contribute to the advancement of the field of entrepreneurship and the interface between management and entrepreneurship, as well as articles on business corporate strategy and government economic policy. On occasions, the journal will also feature case studies of successful firms or other cases having important practical implications. The journal places great emphasis on the quality of the papers it publishes. Submission of a paper will imply that it contains original unpublished work and is not being submitted for publication elsewhere. Officially cited as: Int Entrep Manag J

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: