{"title":"使用随机森林的时间序列量化回归","authors":"Hiroshi Shiraishi, Tomoshige Nakamura, Ryotato Shibuki","doi":"10.1111/jtsa.12731","DOIUrl":null,"url":null,"abstract":"<p>We discuss an application of Generalized Random Forests (GRF) proposed to quantile regression for time series data. We extended the theoretical results of the GRF consistency for i.i.d. data to time series data. In particular, in the main theorem, based only on the general assumptions for time series data and trees, we show that the tsQRF (time series Quantile Regression Forest) estimator is consistent. Compare with existing article, different ideas are used throughout the theoretical proof. In addition, a simulation and real data analysis were conducted. In the simulation, the accuracy of the conditional quantile estimation was evaluated under time series models. In the real data using the Nikkei Stock Average, our estimator is demonstrated to capture volatility more efficiently, thus preventing underestimation of uncertainty.</p>","PeriodicalId":49973,"journal":{"name":"Journal of Time Series Analysis","volume":"45 4","pages":"639-659"},"PeriodicalIF":1.0000,"publicationDate":"2024-01-02","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jtsa.12731","citationCount":"0","resultStr":"{\"title\":\"Time Series Quantile Regression Using Random Forests\",\"authors\":\"Hiroshi Shiraishi, Tomoshige Nakamura, Ryotato Shibuki\",\"doi\":\"10.1111/jtsa.12731\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We discuss an application of Generalized Random Forests (GRF) proposed to quantile regression for time series data. We extended the theoretical results of the GRF consistency for i.i.d. data to time series data. In particular, in the main theorem, based only on the general assumptions for time series data and trees, we show that the tsQRF (time series Quantile Regression Forest) estimator is consistent. Compare with existing article, different ideas are used throughout the theoretical proof. In addition, a simulation and real data analysis were conducted. In the simulation, the accuracy of the conditional quantile estimation was evaluated under time series models. In the real data using the Nikkei Stock Average, our estimator is demonstrated to capture volatility more efficiently, thus preventing underestimation of uncertainty.</p>\",\"PeriodicalId\":49973,\"journal\":{\"name\":\"Journal of Time Series Analysis\",\"volume\":\"45 4\",\"pages\":\"639-659\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2024-01-02\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jtsa.12731\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Time Series Analysis\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jtsa.12731\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Time Series Analysis","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jtsa.12731","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

Time Series Quantile Regression Using Random Forests

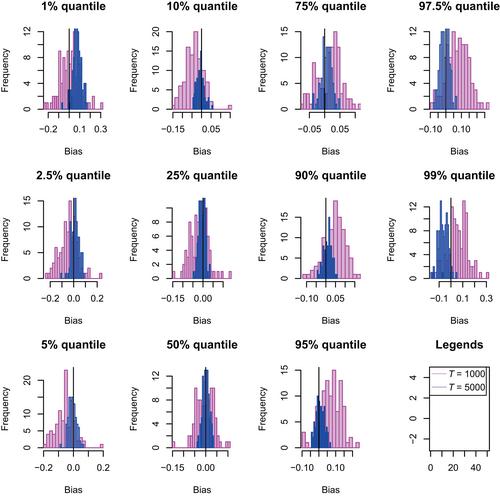

We discuss an application of Generalized Random Forests (GRF) proposed to quantile regression for time series data. We extended the theoretical results of the GRF consistency for i.i.d. data to time series data. In particular, in the main theorem, based only on the general assumptions for time series data and trees, we show that the tsQRF (time series Quantile Regression Forest) estimator is consistent. Compare with existing article, different ideas are used throughout the theoretical proof. In addition, a simulation and real data analysis were conducted. In the simulation, the accuracy of the conditional quantile estimation was evaluated under time series models. In the real data using the Nikkei Stock Average, our estimator is demonstrated to capture volatility more efficiently, thus preventing underestimation of uncertainty.

期刊介绍:

During the last 30 years Time Series Analysis has become one of the most important and widely used branches of Mathematical Statistics. Its fields of application range from neurophysiology to astrophysics and it covers such well-known areas as economic forecasting, study of biological data, control systems, signal processing and communications and vibrations engineering.

The Journal of Time Series Analysis started in 1980, has since become the leading journal in its field, publishing papers on both fundamental theory and applications, as well as review papers dealing with recent advances in major areas of the subject and short communications on theoretical developments. The editorial board consists of many of the world''s leading experts in Time Series Analysis.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: