利用电子账单信息检测信封工资

IF 1.4

4区 经济学

Q3 ECONOMICS

引用次数: 0

摘要

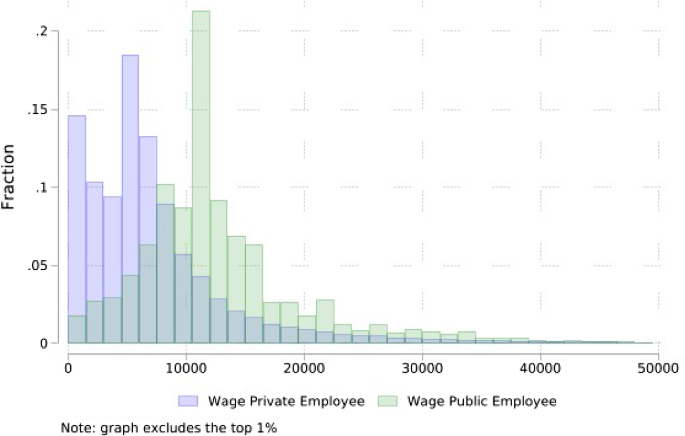

我们利用电子账单系统提供的信息来估算私营部门雇员少报收入的情况。我们采用基于支出的方法,利用公共部门和私营部门雇员的消费水平来估算类似的报告收入水平。我们发现,厄瓜多尔私营部门雇员少报了 7% 至 9% 的收入。少报差距的大小与公司员工人数呈负相关,这与小公司和大公司 "信封工资 "的风险和管理成本不同是一致的。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Detecting envelope wages with e-billing information

We use information from the electronic billing system to estimate the underreporting of income of private sector employees. We follow an expenditure-based methodology using the consumption of public and private sector employees for similar levels of reported income. We find that private sector employees underreport between 7 and 9% of their income in Ecuador. The size of the underreporting gap is negatively correlated with the number of employees at the firm, consistent with different risks and administrative costs of ‘envelope wages’ in small versus large firms.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

International Tax and Public Finance

ECONOMICS-

CiteScore

2.40

自引率

10.00%

发文量

56

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: