{"title":"利用隐马尔可夫模型对井下钻压变化点进行贝叶斯预测","authors":"Ochuko Erivwo, Viliam Makis, Roy Kwon","doi":"10.1002/asmb.2835","DOIUrl":null,"url":null,"abstract":"<p>In the drilling of oil wells, the need to accurately detect downhole formation pressure transitions has long been established as critical for safety and economics. In this article, we examine the application of Hidden Markov Models (HMMs) to oilwell drilling processes with a focus on the real time evolution of downhole formation pressures in its partially observed state. The downhole drilling pressure system can be viewed as a nonlinear, non-degrading stochastic process whose optimum performance is in a region in its warning state prior to random failure in time. The differential pressure system <span></span><math>\n <semantics>\n <mrow>\n <mrow>\n <mo>(</mo>\n <mrow>\n <mo>∆</mo>\n <mi>P</mi>\n </mrow>\n <mo>)</mo>\n </mrow>\n </mrow>\n <annotation>$$ \\left(\\Delta P\\right) $$</annotation>\n </semantics></math> is modeled as a hidden 3 state continuous time Markov process. States 0 and 1 are not observable and represent the normally pressured (initiating <span></span><math>\n <semantics>\n <mrow>\n <mo>∆</mo>\n <mi>P</mi>\n </mrow>\n <annotation>$$ \\Delta P $$</annotation>\n </semantics></math>) and abnormally pressured or warning (reducing <span></span><math>\n <semantics>\n <mrow>\n <mo>∆</mo>\n <mi>P</mi>\n </mrow>\n <annotation>$$ \\Delta P $$</annotation>\n </semantics></math>) states respectively. State 2 is the observable failure state (from negative <span></span><math>\n <semantics>\n <mrow>\n <mo>∆</mo>\n <mi>P</mi>\n </mrow>\n <annotation>$$ \\Delta P $$</annotation>\n </semantics></math> and loss of well control). The signal process of the evolution of differential pressure <span></span><math>\n <semantics>\n <mrow>\n <mrow>\n <mo>(</mo>\n <mrow>\n <mo>∆</mo>\n <mi>P</mi>\n </mrow>\n <mo>)</mo>\n </mrow>\n </mrow>\n <annotation>$$ \\left(\\Delta P\\right) $$</annotation>\n </semantics></math> is identified in the changes in the observable rate of penetration (ROP) encoded in drilling performance data. The state and observation parameters of the HMM are estimated using the Expectation Maximization (EM) algorithm and we show, for a univariate system with a depth dependent time relationship, that the model parameter updates of the EM algorithm equation have explicit solutions. A Bayesian inference model, to determine the safety threshold of the system and early failure prediction at each sampling epoch, is thereafter proposed. The application of our stochastic model of the dynamic evolution of downhole pressures in operational time is illustrated with a hindcast case example. The analysis showed strong early indication of probable failure in real time and was validated in the field post drilling system failure that resulted in significant recovery costs. The potential to predict the differential pressure state transitions ahead of the bit represents a capability not currently available in the industry. This opens up significant opportunity for value creation from optimizing drilling operations to deliver substantial savings in well construction costs.</p>","PeriodicalId":55495,"journal":{"name":"Applied Stochastic Models in Business and Industry","volume":"40 3","pages":"772-790"},"PeriodicalIF":1.3000,"publicationDate":"2023-12-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/asmb.2835","citationCount":"0","resultStr":"{\"title\":\"Bayesian change point prediction for downhole drilling pressures with hidden Markov models\",\"authors\":\"Ochuko Erivwo, Viliam Makis, Roy Kwon\",\"doi\":\"10.1002/asmb.2835\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In the drilling of oil wells, the need to accurately detect downhole formation pressure transitions has long been established as critical for safety and economics. In this article, we examine the application of Hidden Markov Models (HMMs) to oilwell drilling processes with a focus on the real time evolution of downhole formation pressures in its partially observed state. The downhole drilling pressure system can be viewed as a nonlinear, non-degrading stochastic process whose optimum performance is in a region in its warning state prior to random failure in time. The differential pressure system <span></span><math>\\n <semantics>\\n <mrow>\\n <mrow>\\n <mo>(</mo>\\n <mrow>\\n <mo>∆</mo>\\n <mi>P</mi>\\n </mrow>\\n <mo>)</mo>\\n </mrow>\\n </mrow>\\n <annotation>$$ \\\\left(\\\\Delta P\\\\right) $$</annotation>\\n </semantics></math> is modeled as a hidden 3 state continuous time Markov process. States 0 and 1 are not observable and represent the normally pressured (initiating <span></span><math>\\n <semantics>\\n <mrow>\\n <mo>∆</mo>\\n <mi>P</mi>\\n </mrow>\\n <annotation>$$ \\\\Delta P $$</annotation>\\n </semantics></math>) and abnormally pressured or warning (reducing <span></span><math>\\n <semantics>\\n <mrow>\\n <mo>∆</mo>\\n <mi>P</mi>\\n </mrow>\\n <annotation>$$ \\\\Delta P $$</annotation>\\n </semantics></math>) states respectively. State 2 is the observable failure state (from negative <span></span><math>\\n <semantics>\\n <mrow>\\n <mo>∆</mo>\\n <mi>P</mi>\\n </mrow>\\n <annotation>$$ \\\\Delta P $$</annotation>\\n </semantics></math> and loss of well control). The signal process of the evolution of differential pressure <span></span><math>\\n <semantics>\\n <mrow>\\n <mrow>\\n <mo>(</mo>\\n <mrow>\\n <mo>∆</mo>\\n <mi>P</mi>\\n </mrow>\\n <mo>)</mo>\\n </mrow>\\n </mrow>\\n <annotation>$$ \\\\left(\\\\Delta P\\\\right) $$</annotation>\\n </semantics></math> is identified in the changes in the observable rate of penetration (ROP) encoded in drilling performance data. The state and observation parameters of the HMM are estimated using the Expectation Maximization (EM) algorithm and we show, for a univariate system with a depth dependent time relationship, that the model parameter updates of the EM algorithm equation have explicit solutions. A Bayesian inference model, to determine the safety threshold of the system and early failure prediction at each sampling epoch, is thereafter proposed. The application of our stochastic model of the dynamic evolution of downhole pressures in operational time is illustrated with a hindcast case example. The analysis showed strong early indication of probable failure in real time and was validated in the field post drilling system failure that resulted in significant recovery costs. The potential to predict the differential pressure state transitions ahead of the bit represents a capability not currently available in the industry. This opens up significant opportunity for value creation from optimizing drilling operations to deliver substantial savings in well construction costs.</p>\",\"PeriodicalId\":55495,\"journal\":{\"name\":\"Applied Stochastic Models in Business and Industry\",\"volume\":\"40 3\",\"pages\":\"772-790\"},\"PeriodicalIF\":1.3000,\"publicationDate\":\"2023-12-19\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/asmb.2835\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Applied Stochastic Models in Business and Industry\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/asmb.2835\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Applied Stochastic Models in Business and Industry","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/asmb.2835","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

Bayesian change point prediction for downhole drilling pressures with hidden Markov models

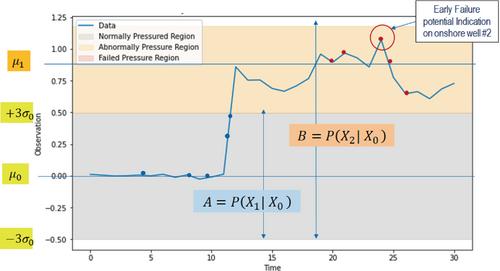

In the drilling of oil wells, the need to accurately detect downhole formation pressure transitions has long been established as critical for safety and economics. In this article, we examine the application of Hidden Markov Models (HMMs) to oilwell drilling processes with a focus on the real time evolution of downhole formation pressures in its partially observed state. The downhole drilling pressure system can be viewed as a nonlinear, non-degrading stochastic process whose optimum performance is in a region in its warning state prior to random failure in time. The differential pressure system is modeled as a hidden 3 state continuous time Markov process. States 0 and 1 are not observable and represent the normally pressured (initiating ) and abnormally pressured or warning (reducing ) states respectively. State 2 is the observable failure state (from negative and loss of well control). The signal process of the evolution of differential pressure is identified in the changes in the observable rate of penetration (ROP) encoded in drilling performance data. The state and observation parameters of the HMM are estimated using the Expectation Maximization (EM) algorithm and we show, for a univariate system with a depth dependent time relationship, that the model parameter updates of the EM algorithm equation have explicit solutions. A Bayesian inference model, to determine the safety threshold of the system and early failure prediction at each sampling epoch, is thereafter proposed. The application of our stochastic model of the dynamic evolution of downhole pressures in operational time is illustrated with a hindcast case example. The analysis showed strong early indication of probable failure in real time and was validated in the field post drilling system failure that resulted in significant recovery costs. The potential to predict the differential pressure state transitions ahead of the bit represents a capability not currently available in the industry. This opens up significant opportunity for value creation from optimizing drilling operations to deliver substantial savings in well construction costs.

期刊介绍:

ASMBI - Applied Stochastic Models in Business and Industry (formerly Applied Stochastic Models and Data Analysis) was first published in 1985, publishing contributions in the interface between stochastic modelling, data analysis and their applications in business, finance, insurance, management and production. In 2007 ASMBI became the official journal of the International Society for Business and Industrial Statistics (www.isbis.org). The main objective is to publish papers, both technical and practical, presenting new results which solve real-life problems or have great potential in doing so. Mathematical rigour, innovative stochastic modelling and sound applications are the key ingredients of papers to be published, after a very selective review process.

The journal is very open to new ideas, like Data Science and Big Data stemming from problems in business and industry or uncertainty quantification in engineering, as well as more traditional ones, like reliability, quality control, design of experiments, managerial processes, supply chains and inventories, insurance, econometrics, financial modelling (provided the papers are related to real problems). The journal is interested also in papers addressing the effects of business and industrial decisions on the environment, healthcare, social life. State-of-the art computational methods are very welcome as well, when combined with sound applications and innovative models.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: