{"title":"杠杆指数和 ETF 的长期回报估算","authors":"Hayden Brown","doi":"10.1007/s11408-023-00440-3","DOIUrl":null,"url":null,"abstract":"<p>Daily leveraged exchange traded funds amplify gains and losses of their underlying benchmark indexes on a daily basis. The result of going long in a daily leveraged ETF for more than one day is less clear. Here, bounds are given for the log-returns of a daily leveraged ETF when going long for more than just one day. The bounds are quadratic in the daily log-returns of the underlying benchmark index, and they are used to find sufficient conditions for outperformance and underperformance of a daily leveraged ETF in relation to its underlying benchmark index. Of note, results show promise for a 2x daily leveraged S&P 500 ETF. If the average annual log-return of the S&P 500 index continues to be at least .0658, as it has been in the past, and the standard deviation of daily S&P 500 log-returns is under .0125, then a 2x daily leveraged S&P 500 ETF will perform at least as well as the S&P 500 index in the long-run.</p>","PeriodicalId":44895,"journal":{"name":"Financial Markets and Portfolio Management","volume":"27 1","pages":""},"PeriodicalIF":1.8000,"publicationDate":"2023-12-16","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Long-term returns estimation of leveraged indexes and ETFs\",\"authors\":\"Hayden Brown\",\"doi\":\"10.1007/s11408-023-00440-3\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Daily leveraged exchange traded funds amplify gains and losses of their underlying benchmark indexes on a daily basis. The result of going long in a daily leveraged ETF for more than one day is less clear. Here, bounds are given for the log-returns of a daily leveraged ETF when going long for more than just one day. The bounds are quadratic in the daily log-returns of the underlying benchmark index, and they are used to find sufficient conditions for outperformance and underperformance of a daily leveraged ETF in relation to its underlying benchmark index. Of note, results show promise for a 2x daily leveraged S&P 500 ETF. If the average annual log-return of the S&P 500 index continues to be at least .0658, as it has been in the past, and the standard deviation of daily S&P 500 log-returns is under .0125, then a 2x daily leveraged S&P 500 ETF will perform at least as well as the S&P 500 index in the long-run.</p>\",\"PeriodicalId\":44895,\"journal\":{\"name\":\"Financial Markets and Portfolio Management\",\"volume\":\"27 1\",\"pages\":\"\"},\"PeriodicalIF\":1.8000,\"publicationDate\":\"2023-12-16\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Financial Markets and Portfolio Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s11408-023-00440-3\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Financial Markets and Portfolio Management","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11408-023-00440-3","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Long-term returns estimation of leveraged indexes and ETFs

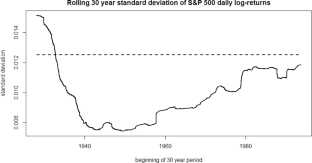

Daily leveraged exchange traded funds amplify gains and losses of their underlying benchmark indexes on a daily basis. The result of going long in a daily leveraged ETF for more than one day is less clear. Here, bounds are given for the log-returns of a daily leveraged ETF when going long for more than just one day. The bounds are quadratic in the daily log-returns of the underlying benchmark index, and they are used to find sufficient conditions for outperformance and underperformance of a daily leveraged ETF in relation to its underlying benchmark index. Of note, results show promise for a 2x daily leveraged S&P 500 ETF. If the average annual log-return of the S&P 500 index continues to be at least .0658, as it has been in the past, and the standard deviation of daily S&P 500 log-returns is under .0125, then a 2x daily leveraged S&P 500 ETF will perform at least as well as the S&P 500 index in the long-run.

期刊介绍:

The journal Financial Markets and Portfolio Management invites submissions of original research articles in all areas of finance, especially in – but not limited to – financial markets, portfolio choice and wealth management, asset pricing, risk management, and regulation. Its principal objective is to publish high-quality articles of innovative research and practical application. The readers of Financial Markets and Portfolio Management are academics and professionals in finance and economics, especially in the areas of asset management. FMPM publishes academic and applied research articles, shorter ''Perspectives'' and survey articles on current topics of interest to the financial community, as well as book reviews. All article submissions are subject to a double-blind peer review. http://www.fmpm.org

Officially cited as: Financ Mark Portf Manag

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: