{"title":"收益幻想:挑战高收益股票的说法","authors":"Yin Chen, Roni Israelov","doi":"10.1057/s41260-023-00340-1","DOIUrl":null,"url":null,"abstract":"<p>While stocks with high dividends have historically outperformed those with low dividends, we show that the difference can be completely explained by a set of well-known factors including value, quality and defensive. Applying a dividend filter to a portfolio of strategies having high exposure to these factors yields sub-optimal results. To test whether incorporating dividend yields can improve the performance of long-only factor portfolios, we construct a set of dividend-favored long-only factor portfolios with a heuristic rebalance algorithm and find that their after-tax net returns are lower than the dividend-agnostic counterparts. Collectively our results indicate that long-only active investors are better off loading directly on value, quality and defensive factors than purposely tilting their portfolios toward high-dividend stocks.</p>","PeriodicalId":45953,"journal":{"name":"Journal of Asset Management","volume":"15 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2023-12-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Income illusions: challenging the high yield stock narrative\",\"authors\":\"Yin Chen, Roni Israelov\",\"doi\":\"10.1057/s41260-023-00340-1\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>While stocks with high dividends have historically outperformed those with low dividends, we show that the difference can be completely explained by a set of well-known factors including value, quality and defensive. Applying a dividend filter to a portfolio of strategies having high exposure to these factors yields sub-optimal results. To test whether incorporating dividend yields can improve the performance of long-only factor portfolios, we construct a set of dividend-favored long-only factor portfolios with a heuristic rebalance algorithm and find that their after-tax net returns are lower than the dividend-agnostic counterparts. Collectively our results indicate that long-only active investors are better off loading directly on value, quality and defensive factors than purposely tilting their portfolios toward high-dividend stocks.</p>\",\"PeriodicalId\":45953,\"journal\":{\"name\":\"Journal of Asset Management\",\"volume\":\"15 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-12-13\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Asset Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1057/s41260-023-00340-1\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Asset Management","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41260-023-00340-1","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Income illusions: challenging the high yield stock narrative

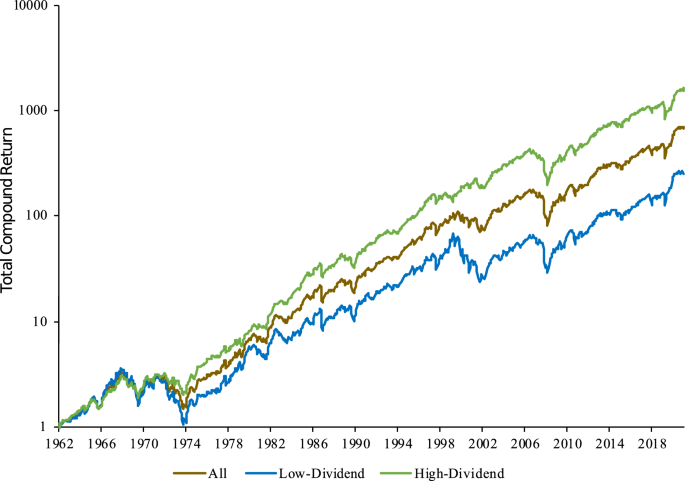

While stocks with high dividends have historically outperformed those with low dividends, we show that the difference can be completely explained by a set of well-known factors including value, quality and defensive. Applying a dividend filter to a portfolio of strategies having high exposure to these factors yields sub-optimal results. To test whether incorporating dividend yields can improve the performance of long-only factor portfolios, we construct a set of dividend-favored long-only factor portfolios with a heuristic rebalance algorithm and find that their after-tax net returns are lower than the dividend-agnostic counterparts. Collectively our results indicate that long-only active investors are better off loading directly on value, quality and defensive factors than purposely tilting their portfolios toward high-dividend stocks.

期刊介绍:

The Journal of Asset Management covers:new investment strategies, methodologies and techniquesnew products and trading developmentsimportant regulatory and legal developmentsemerging trends in asset managementUnder the guidance of its expert Editors and an eminent international Editorial Board, Journal of Asset Management has developed to provide an international forum for latest thinking, techniques and developments for the Fund Management Industry, from high-growth investment strategies to modelling and managing risk, from active management to index tracking. The Journal has established itself as a key bridge between applied academic research, commercial best practice and regulatory interests, globally.Each issue of Journal of Asset Management publishes detailed, authoritative briefings, analysis, research and reviews by leading experts in the field, to keep subscribers up to date with the latest developments and thinking in asset management.Journal of Asset Management covers:asset allocation hedge fund strategies risk definition and management index tracking performance measurement stock selection investment methodologies and techniques portfolio management and weighting product development and innovation active asset management style analysis strategies to match client profiles time horizons emerging markets alternative investments derivatives and hedging instruments pensions economics

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: