Judite Gonçalves, Roxanne Merenda, João Pereira dos Santos

{"title":"不那么甜蜜:汽水税对生产商的影响","authors":"Judite Gonçalves, Roxanne Merenda, João Pereira dos Santos","doi":"10.1007/s10797-023-09808-7","DOIUrl":null,"url":null,"abstract":"<p>Portugal introduced a sugar-sweetened beverages (SSB) tax in 2017. This study uses unique administrative accounting data for all SSB producers/importers in Portugal, and an event study design with bottled water firms as the primary comparison group, to assess the causal impacts of the tax on multiple firm-level outcomes. We find a 6.8% average decrease in domestic SSB sales, relative to bottled water. The soda tax hindered SSB firms’ financial health, namely net income, ability to convert receivables into cash, and liabilities. SSB producers/importers did not decrease wages, cut jobs, or modify their workforce toward higher R&D capacity. Forgone corporate income tax appears negligible compared to the government revenue generated by the tax itself.</p>","PeriodicalId":47518,"journal":{"name":"International Tax and Public Finance","volume":"32 12","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2023-11-22","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Not so sweet: impacts of a soda tax on producers\",\"authors\":\"Judite Gonçalves, Roxanne Merenda, João Pereira dos Santos\",\"doi\":\"10.1007/s10797-023-09808-7\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Portugal introduced a sugar-sweetened beverages (SSB) tax in 2017. This study uses unique administrative accounting data for all SSB producers/importers in Portugal, and an event study design with bottled water firms as the primary comparison group, to assess the causal impacts of the tax on multiple firm-level outcomes. We find a 6.8% average decrease in domestic SSB sales, relative to bottled water. The soda tax hindered SSB firms’ financial health, namely net income, ability to convert receivables into cash, and liabilities. SSB producers/importers did not decrease wages, cut jobs, or modify their workforce toward higher R&D capacity. Forgone corporate income tax appears negligible compared to the government revenue generated by the tax itself.</p>\",\"PeriodicalId\":47518,\"journal\":{\"name\":\"International Tax and Public Finance\",\"volume\":\"32 12\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-11-22\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Tax and Public Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10797-023-09808-7\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Tax and Public Finance","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10797-023-09808-7","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

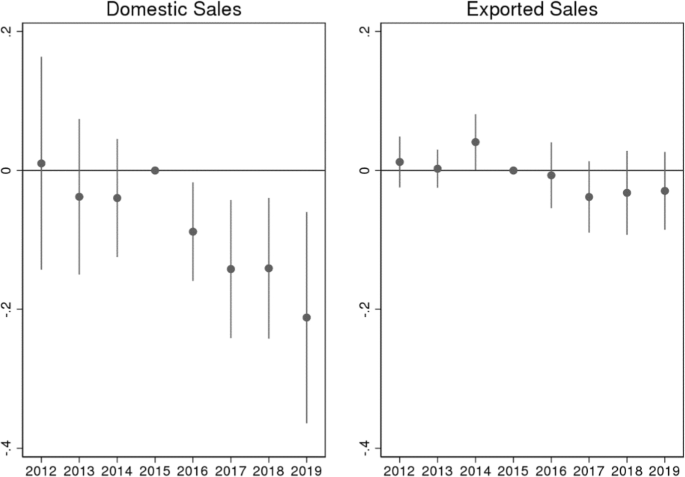

Portugal introduced a sugar-sweetened beverages (SSB) tax in 2017. This study uses unique administrative accounting data for all SSB producers/importers in Portugal, and an event study design with bottled water firms as the primary comparison group, to assess the causal impacts of the tax on multiple firm-level outcomes. We find a 6.8% average decrease in domestic SSB sales, relative to bottled water. The soda tax hindered SSB firms’ financial health, namely net income, ability to convert receivables into cash, and liabilities. SSB producers/importers did not decrease wages, cut jobs, or modify their workforce toward higher R&D capacity. Forgone corporate income tax appears negligible compared to the government revenue generated by the tax itself.

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: