{"title":"基于广义双曲分布的非参数模态回归带宽选择新方法","authors":"Hongpeng Yuan, Sijia Xiang, Weixin Yao","doi":"10.1007/s00180-023-01435-4","DOIUrl":null,"url":null,"abstract":"<p>As a complement to standard mean and quantile regression, nonparametric modal regression has been broadly applied in various fields. By focusing on the most likely conditional value of Y given x, the nonparametric modal regression is shown to be resistant to outliers and some forms of measurement error, and the prediction intervals are shorter when data is skewed. However, the bandwidth selection is critical but very challenging, since the traditional least-squares based cross-validation method cannot be applied. We propose to select the bandwidth by applying the asymptotic global optimal bandwidth and the flexible generalized hyperbolic (GH) distribution as the distribution of the error. Unlike the plug-in method, the new method does not require preliminary parameters to be chosen in advance, is easy to compute by any statistical software, and is computationally efficient compared to the existing kernel density estimator (KDE) based method. Numerical studies show that the GH based bandwidth performs better than existing bandwidth selector, in terms of higher coverage probabilities. Real data applications also illustrate the superior performance of the new bandwidth.</p>","PeriodicalId":55223,"journal":{"name":"Computational Statistics","volume":"22 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2023-11-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"A new bandwidth selection method for nonparametric modal regression based on generalized hyperbolic distributions\",\"authors\":\"Hongpeng Yuan, Sijia Xiang, Weixin Yao\",\"doi\":\"10.1007/s00180-023-01435-4\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>As a complement to standard mean and quantile regression, nonparametric modal regression has been broadly applied in various fields. By focusing on the most likely conditional value of Y given x, the nonparametric modal regression is shown to be resistant to outliers and some forms of measurement error, and the prediction intervals are shorter when data is skewed. However, the bandwidth selection is critical but very challenging, since the traditional least-squares based cross-validation method cannot be applied. We propose to select the bandwidth by applying the asymptotic global optimal bandwidth and the flexible generalized hyperbolic (GH) distribution as the distribution of the error. Unlike the plug-in method, the new method does not require preliminary parameters to be chosen in advance, is easy to compute by any statistical software, and is computationally efficient compared to the existing kernel density estimator (KDE) based method. Numerical studies show that the GH based bandwidth performs better than existing bandwidth selector, in terms of higher coverage probabilities. Real data applications also illustrate the superior performance of the new bandwidth.</p>\",\"PeriodicalId\":55223,\"journal\":{\"name\":\"Computational Statistics\",\"volume\":\"22 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-11-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Computational Statistics\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://doi.org/10.1007/s00180-023-01435-4\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Statistics","FirstCategoryId":"100","ListUrlMain":"https://doi.org/10.1007/s00180-023-01435-4","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

A new bandwidth selection method for nonparametric modal regression based on generalized hyperbolic distributions

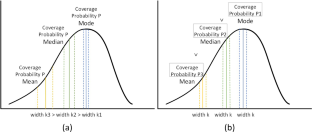

As a complement to standard mean and quantile regression, nonparametric modal regression has been broadly applied in various fields. By focusing on the most likely conditional value of Y given x, the nonparametric modal regression is shown to be resistant to outliers and some forms of measurement error, and the prediction intervals are shorter when data is skewed. However, the bandwidth selection is critical but very challenging, since the traditional least-squares based cross-validation method cannot be applied. We propose to select the bandwidth by applying the asymptotic global optimal bandwidth and the flexible generalized hyperbolic (GH) distribution as the distribution of the error. Unlike the plug-in method, the new method does not require preliminary parameters to be chosen in advance, is easy to compute by any statistical software, and is computationally efficient compared to the existing kernel density estimator (KDE) based method. Numerical studies show that the GH based bandwidth performs better than existing bandwidth selector, in terms of higher coverage probabilities. Real data applications also illustrate the superior performance of the new bandwidth.

期刊介绍:

Computational Statistics (CompStat) is an international journal which promotes the publication of applications and methodological research in the field of Computational Statistics. The focus of papers in CompStat is on the contribution to and influence of computing on statistics and vice versa. The journal provides a forum for computer scientists, mathematicians, and statisticians in a variety of fields of statistics such as biometrics, econometrics, data analysis, graphics, simulation, algorithms, knowledge based systems, and Bayesian computing. CompStat publishes hardware, software plus package reports.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: