Nobuyuki Hanaki, Cars Hommes, Dávid Kopányi, Anita Kopányi-Peuker, Jan Tuinstra

{"title":"预测收益而不是价格会加剧金融泡沫","authors":"Nobuyuki Hanaki, Cars Hommes, Dávid Kopányi, Anita Kopányi-Peuker, Jan Tuinstra","doi":"10.1007/s10683-023-09815-9","DOIUrl":null,"url":null,"abstract":"<p>Expectations of future returns are pivotal for investors’ trading decisions, and are therefore an important determinant of the evolution of actual returns. Evidence from individual choice experiments with exogenously given time series of returns suggests that subjects’ return forecasts are substantially affected by how they are elicited and by the format in which subjects receive information about past asset performance. In order to understand the impact of these effects found at the individual level on market dynamics, we consider a learning to forecast experiment where prices and returns are endogenously determined and depend directly upon subjects’ forecasts. We vary both the variable (prices or returns) subjects observe and the variable (prices or returns) they have to forecast, with the same underlying data generating process for each treatment. Although there is no significant effect of the presentation format of past information, we do find that markets are significantly more unstable when subjects have to forecast returns instead of prices. Our results therefore show that the elicitation format may exacerbate, or even create, bubbles and crashes in financial markets.</p>","PeriodicalId":47992,"journal":{"name":"Experimental Economics","volume":"123 4","pages":""},"PeriodicalIF":1.7000,"publicationDate":"2023-12-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Forecasting returns instead of prices exacerbates financial bubbles\",\"authors\":\"Nobuyuki Hanaki, Cars Hommes, Dávid Kopányi, Anita Kopányi-Peuker, Jan Tuinstra\",\"doi\":\"10.1007/s10683-023-09815-9\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Expectations of future returns are pivotal for investors’ trading decisions, and are therefore an important determinant of the evolution of actual returns. Evidence from individual choice experiments with exogenously given time series of returns suggests that subjects’ return forecasts are substantially affected by how they are elicited and by the format in which subjects receive information about past asset performance. In order to understand the impact of these effects found at the individual level on market dynamics, we consider a learning to forecast experiment where prices and returns are endogenously determined and depend directly upon subjects’ forecasts. We vary both the variable (prices or returns) subjects observe and the variable (prices or returns) they have to forecast, with the same underlying data generating process for each treatment. Although there is no significant effect of the presentation format of past information, we do find that markets are significantly more unstable when subjects have to forecast returns instead of prices. Our results therefore show that the elicitation format may exacerbate, or even create, bubbles and crashes in financial markets.</p>\",\"PeriodicalId\":47992,\"journal\":{\"name\":\"Experimental Economics\",\"volume\":\"123 4\",\"pages\":\"\"},\"PeriodicalIF\":1.7000,\"publicationDate\":\"2023-12-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Experimental Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10683-023-09815-9\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Experimental Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10683-023-09815-9","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

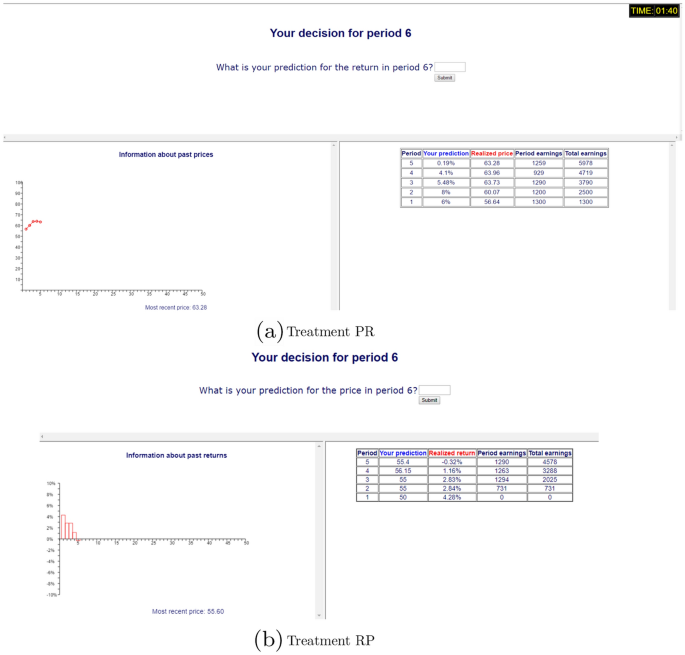

Forecasting returns instead of prices exacerbates financial bubbles

Expectations of future returns are pivotal for investors’ trading decisions, and are therefore an important determinant of the evolution of actual returns. Evidence from individual choice experiments with exogenously given time series of returns suggests that subjects’ return forecasts are substantially affected by how they are elicited and by the format in which subjects receive information about past asset performance. In order to understand the impact of these effects found at the individual level on market dynamics, we consider a learning to forecast experiment where prices and returns are endogenously determined and depend directly upon subjects’ forecasts. We vary both the variable (prices or returns) subjects observe and the variable (prices or returns) they have to forecast, with the same underlying data generating process for each treatment. Although there is no significant effect of the presentation format of past information, we do find that markets are significantly more unstable when subjects have to forecast returns instead of prices. Our results therefore show that the elicitation format may exacerbate, or even create, bubbles and crashes in financial markets.

期刊介绍:

Experimental methods are uniquely suited to the study of many phenomena that have been difficult to observe directly in naturally occurring economic contexts. For example, the ability to induce preferences and control information structures makes it possible to isolate the effects of alternate economic structures, policies, and market institutions.Experimental Economics is an international journal that serves the growing group of economists around the world who use experimental methods. The journal invites high-quality papers in any area of experimental research in economics and related fields (i.e. accounting, finance, political science, and the psychology of decision making). State-of-the-art theoretical work and econometric work that is motivated by experimental data is also encouraged. The journal will also consider articles with a primary focus on methodology or replication of controversial findings. We welcome experiments conducted in either the laboratory or in the field. The relevant data can be decisions or non-choice data such as physiological measurements. However, we only consider studies that do not employ deception of participants and in which participants are incentivized. Experimental Economics is structured to promote experimental economics by bringing together innovative research that meets professional standards of experimental method, but without editorial bias towards specific orientations. All papers will be reviewed through the standard, anonymous-referee procedure and all accepted manuscripts will be subject to the approval of two editors. Authors must submit the instructions that participants in their study received at the time of submission of their manuscript. Authors are expected to submit separate data appendices which will be attached to the journal''s web page upon publication. Officially cited as: Exp Econ

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: