隐含波动率浮出水面:使用5亿期权价格的综合分析

IF 0.9

4区 经济学

Q4 BUSINESS, FINANCE

引用次数: 0

摘要

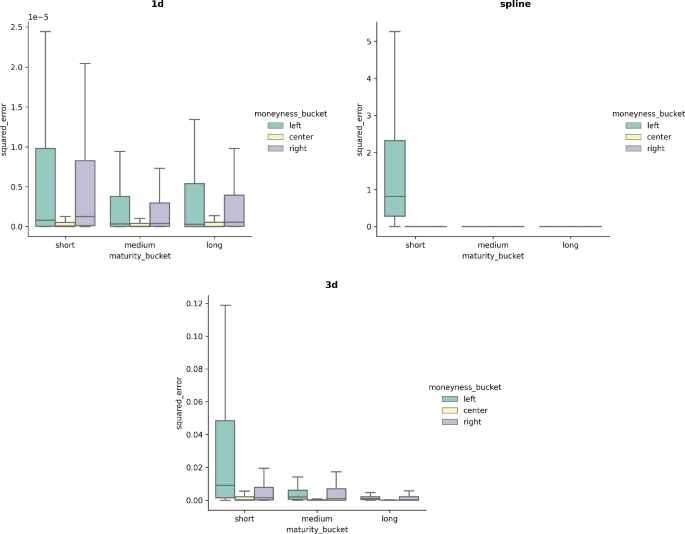

摘要本文探讨了股票波动面准确估计的关键问题,这是期权定价、风险管理和经验资产定价不可或缺的任务。利用499只美国个股和标准普尔500指数期权的5亿次每日价格观察组成的综合数据集,该研究调查了构建波动面的各种方法的准确性。OptionMetrics (IvyDB US文件和数据参考手册,5.2版,Rev. 01/27/2022, Computer software manual, New York, 2022)与Figlewski的半参数样条(in: Robert F. Engle (ed))估算隐含风险中性密度的比较评价。波动性和时间序列计量经济学:荣誉论文,牛津大学出版社,牛津,2008年),和一个完善的一维核平滑显示了后者的明显优势。这种方法在所有货币性、成熟性和流动性类别中始终优于其对应方法,并且误差指标明显较低。该研究进一步揭示了Bakshi等人(Rev financial Stud 16:10 3 - 143,2003)的矩和偏度跨越在提取过程中的显著扭曲,这些扭曲是由注入噪声的三维核平滑引起的,可能会误导衍生品的定价和交易决策。这些发现为交易员、风险管理人员、投资者和研究人员提供了有价值的见解,为制定更准确、噪音更小的波动性预测提供了一种强大的、一刀切的方法。该研究促进了我们对期权隐含信息、其提取以及对金融市场的更广泛影响的理解。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Implied volatility surfaces: a comprehensive analysis using half a billion option prices

Abstract This study delves into the critical aspect of accurately estimating single stock volatility surfaces, a task indispensable for option pricing, risk management, and empirical asset pricing. Utilizing a comprehensive dataset consisting of half a billion daily price observations for options on 499 US individual stocks and the S&P 500, the research investigates the accuracy of diverse methods for constructing volatility surfaces. The comparative evaluation of the three-dimensional kernel smoother by OptionMetrics (IvyDB US file and data reference manual, version 5.2, Rev. 01/27/2022, Computer software manual, New York, 2022), the semi-parametric spline by Figlewski (in: Robert F. Engle (ed) Estimating the implied risk neutral density. Volatility and time series econometrics: Essays in honor, Oxford University Press, Oxford, 2008), and a refined one-dimensional kernel smoother reveals the distinct superiority of the latter. This method consistently outperforms its counterparts across all moneyness, maturity, and liquidity categories, with markedly lower error metrics. The study further uncovers significant distortions in the extraction of Bakshi et al. (Rev Financ Stud 16:101–143, 2003) moments and skewness spanning induced by the noise-infused three-dimensional kernel smoother, which could potentially mislead derivative pricing and trading decisions. The findings offer valuable insights to traders, risk managers, investors, and researchers, suggesting a robust, one-size-fits-all method for crafting more accurate and less noisy volatility predictions. The research advances our understanding of option-implied information, its extraction, and broader implications for financial markets.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Review of Derivatives Research

Multiple-

CiteScore

1.40

自引率

0.00%

发文量

8

期刊介绍:

The proliferation of derivative assets during the past two decades is unprecedented. With this growth in derivatives comes the need for financial institutions, institutional investors, and corporations to use sophisticated quantitative techniques to take full advantage of the spectrum of these new financial instruments. Academic research has significantly contributed to our understanding of derivative assets and markets. The growth of derivative asset markets has been accompanied by a commensurate growth in the volume of scientific research. The Review of Derivatives Research provides an international forum for researchers involved in the general areas of derivative assets. The Review publishes high-quality articles dealing with the pricing and hedging of derivative assets on any underlying asset (commodity, interest rate, currency, equity, real estate, traded or non-traded, etc.). Specific topics include but are not limited to: econometric analyses of derivative markets (efficiency, anomalies, performance, etc.) analysis of swap markets market microstructure and volatility issues regulatory and taxation issues credit risk new areas of applications such as corporate finance (capital budgeting, debt innovations), international trade (tariffs and quotas), banking and insurance (embedded options, asset-liability management) risk-sharing issues and the design of optimal derivative securities risk management, management and control valuation and analysis of the options embedded in capital projects valuation and hedging of exotic options new areas for further development (i.e. natural resources, environmental economics. The Review has a double-blind refereeing process. In contrast to the delays in the decision making and publication processes of many current journals, the Review will provide authors with an initial decision within nine weeks of receipt of the manuscript and a goal of publication within six months after acceptance. Finally, a section of the journal is available for rapid publication on `hot'' issues in the market, small technical pieces, and timely essays related to pending legislation and policy. Officially cited as: Rev Deriv Res

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: