解释变量的解释能力

IF 5.8

3区 管理学

Q1 BUSINESS, FINANCE

引用次数: 1

摘要

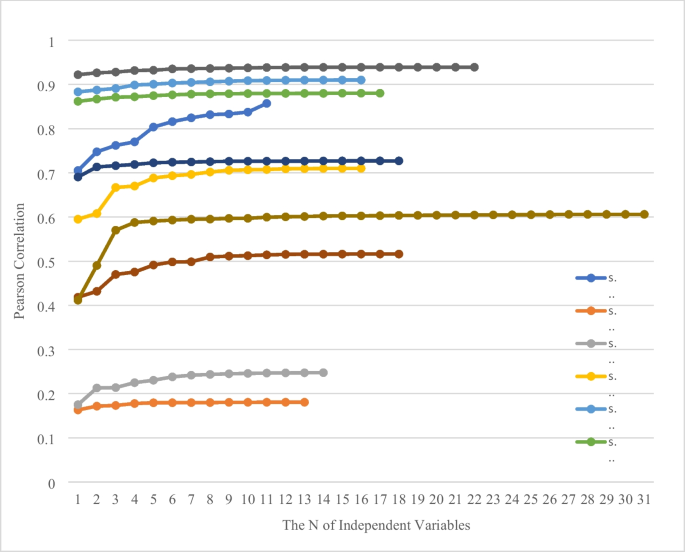

摘要本文考察了当前实证会计的研究范式。我们的问题是:一般来说,估计的回归是否支持推广的叙述?我们关注回归模型的主要变量,并考虑它对因变量解释的贡献程度。我们重复了最近发表的10项会计研究,所有这些研究都依赖于显著的t统计量,每常规水平,声称拒绝零假设。我们的检验表明,在8项研究中,主要感兴趣变量所贡献的增量解释力实际上为零。对于剩下的两个,增量贡献最多是边际的。这些发现突出了对t统计量作为主要评价指标的明显过度依赖。对数据的仔细检查表明,产生的t统计量拒绝原假设主要是由于大量的观察值(N)。实证会计研究通常需要N >1万拒绝零假设。为了避免t统计量与N的联系的缺点,我们考虑使用标准化回归(SR)的含义。SR系数的大小直接反映了变量的相关性。实证分析表明,在不参考N或t统计量的情况下,变量的估计SR系数大小与其增量解释能力之间存在很强的相关性。本文章由计算机程序翻译,如有差异,请以英文原文为准。

The explanatory power of explanatory variables

Abstract This paper examines the current empirical accounting research paradigm. We ask: In general, do the estimated regressions support the promoted narratives? We focus on a regression model’s main variable of interest and consider the extent to which it contributes to the explanation of the dependent variable. We replicate 10 recently published accounting studies, all of which rely on significant t-statistics, per conventional levels, to claim rejection of the null hypothesis. Our examination shows that in eight studies, the incremental explanatory power contributed by the main variable of interest is effectively zero. For the remaining two, the incremental contribution is at best marginal. These findings highlight the apparent overreliance on t-statistics as the primary evaluation metric. A closer examination of the data shows that the t-statistics produced reject the null hypothesis primarily due to a large number of observations (N). Empirical accounting studies often require N > 10,000 to reject the null hypothesis. To avoid the drawback of t-statistics’ connection with N, we consider the implications of using Standardized Regressions (SR). The magnitude of SR coefficients indicates variables’ relevance directly. Empirical analyses establish a strong correlation between a variable’s estimated SR coefficient magnitude and its incremental explanatory power, without reference to N or t-statistics.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Review of Accounting Studies

BUSINESS, FINANCE-

CiteScore

7.90

自引率

7.10%

发文量

82

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: