{"title":"利用信贷和股票期权市场的价格进行投资组合风险管理","authors":"Jean-François Bégin, Mathieu Boudreault, Mathieu Thériault","doi":"10.1002/fut.22465","DOIUrl":null,"url":null,"abstract":"<p>This study presents a firm-specific methodology for extracting implied default intensities and recovery rates jointly from unit recovery claim prices—backed by out-of-the-money put options—and credit default swap premiums, therefore providing time-varying and market-consistent views of credit risk at the individual level. We apply the procedure to about 400 firms spanning different sectors of the US economy between 2003 and 2019. The main determinants of default intensities and recovery rates are analyzed with statistical and machine learning methods linking default risk and credit losses to market, sector, and individual variables. Consistent with the literature, we find that individual volatility, leverage, and corporate bond market determinants are key factors explaining the implied default intensities and recovery rates. Then, we apply the framework in the context of credit risk management in applications, like, market-consistent credit value-at-risk calculation and stress testing.</p>","PeriodicalId":15863,"journal":{"name":"Journal of Futures Markets","volume":"44 1","pages":"122-147"},"PeriodicalIF":1.8000,"publicationDate":"2023-10-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22465","citationCount":"1","resultStr":"{\"title\":\"Leveraging prices from credit and equity option markets for portfolio risk management\",\"authors\":\"Jean-François Bégin, Mathieu Boudreault, Mathieu Thériault\",\"doi\":\"10.1002/fut.22465\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study presents a firm-specific methodology for extracting implied default intensities and recovery rates jointly from unit recovery claim prices—backed by out-of-the-money put options—and credit default swap premiums, therefore providing time-varying and market-consistent views of credit risk at the individual level. We apply the procedure to about 400 firms spanning different sectors of the US economy between 2003 and 2019. The main determinants of default intensities and recovery rates are analyzed with statistical and machine learning methods linking default risk and credit losses to market, sector, and individual variables. Consistent with the literature, we find that individual volatility, leverage, and corporate bond market determinants are key factors explaining the implied default intensities and recovery rates. Then, we apply the framework in the context of credit risk management in applications, like, market-consistent credit value-at-risk calculation and stress testing.</p>\",\"PeriodicalId\":15863,\"journal\":{\"name\":\"Journal of Futures Markets\",\"volume\":\"44 1\",\"pages\":\"122-147\"},\"PeriodicalIF\":1.8000,\"publicationDate\":\"2023-10-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22465\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Futures Markets\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/fut.22465\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Futures Markets","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/fut.22465","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Leveraging prices from credit and equity option markets for portfolio risk management

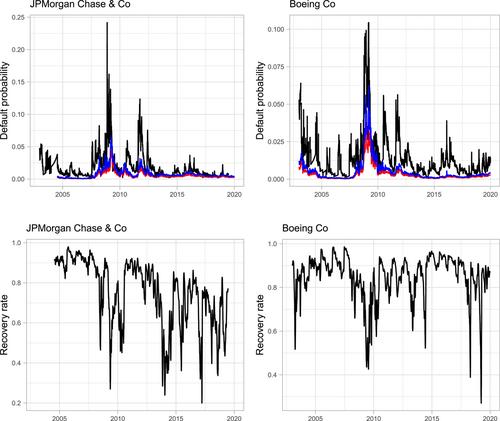

This study presents a firm-specific methodology for extracting implied default intensities and recovery rates jointly from unit recovery claim prices—backed by out-of-the-money put options—and credit default swap premiums, therefore providing time-varying and market-consistent views of credit risk at the individual level. We apply the procedure to about 400 firms spanning different sectors of the US economy between 2003 and 2019. The main determinants of default intensities and recovery rates are analyzed with statistical and machine learning methods linking default risk and credit losses to market, sector, and individual variables. Consistent with the literature, we find that individual volatility, leverage, and corporate bond market determinants are key factors explaining the implied default intensities and recovery rates. Then, we apply the framework in the context of credit risk management in applications, like, market-consistent credit value-at-risk calculation and stress testing.

期刊介绍:

The Journal of Futures Markets chronicles the latest developments in financial futures and derivatives. It publishes timely, innovative articles written by leading finance academics and professionals. Coverage ranges from the highly practical to theoretical topics that include futures, derivatives, risk management and control, financial engineering, new financial instruments, hedging strategies, analysis of trading systems, legal, accounting, and regulatory issues, and portfolio optimization. This publication contains the very latest research from the top experts.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: