波动率调整的研究

IF 0.7

Q3 SOCIAL SCIENCES, MATHEMATICAL METHODS

引用次数: 0

摘要

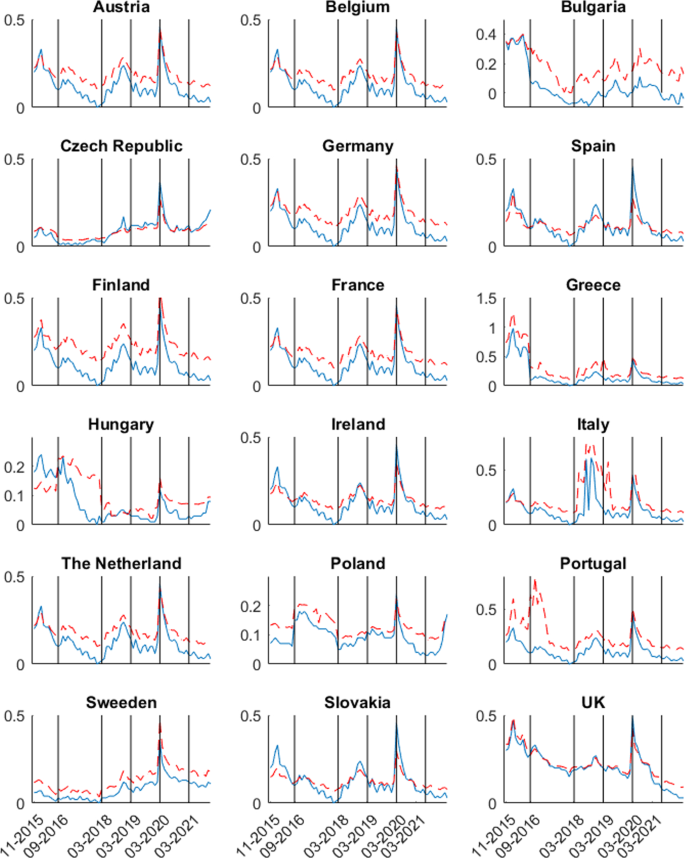

摘要本文利用市场数据重构不同国家的波动性调整,波动性调整是偿付能力II框架的一个组成部分,旨在减轻市场风险对保险负债的影响。我们观察到,波动率调整,尤其是拟议的新机制,不受信贷质量、债券流动性不足和投资者风险偏好的影响,而是受金融市场动荡和股市表现的影响,这一点与监管规定部分一致。我们还表明,EIOPA提出的新机制与撰写当前论文时有效的机制表现不同,产生更高和更平滑的值,并在偿付能力II资本要求方面为保险公司提供了救济。本文章由计算机程序翻译,如有差异,请以英文原文为准。

An investigation of the Volatility Adjustment

Abstract We use market data to reconstruct the volatility adjustment, a component of the Solvency II framework designed to mitigate the impact of market risk on insurance liabilities, of different countries on a monthly basis. Only partially in agreement with the regulation, we observe that the volatility adjustment, especially the proposed new mechanism, is not affected by credit quality, illiquidity of bonds, and investors’ risk appetite, but by turbulence in financial markets and equity market performance. We also show that the new mechanism proposed by EIOPA performs differently with respect to the one in force at the time of writing the current paper, yielding higher and smoother values and providing a relief to insurance companies on the Solvency II capital requirement front.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Decisions in Economics and Finance

SOCIAL SCIENCES, MATHEMATICAL METHODS-

CiteScore

2.50

自引率

9.10%

发文量

10

期刊介绍:

Decisions in Economics and Finance: A Journal of Applied Mathematics is the official publication of the Association for Mathematics Applied to Social and Economic Sciences (AMASES). It provides a specialised forum for the publication of research in all areas of mathematics as applied to economics, finance, insurance, management and social sciences. Primary emphasis is placed on original research concerning topics in mathematics or computational techniques which are explicitly motivated by or contribute to the analysis of economic or financial problems.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: