在基于树的失效管理策略中包括个体客户生命周期价值和竞争风险

IF 1.6

Q4 BUSINESS, FINANCE

引用次数: 0

摘要

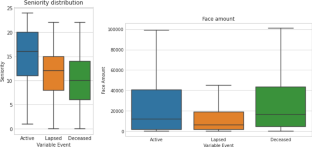

基于开明失效模型的保留策略对寿险公司来说是一个强大的盈利杠杆。一些机器学习模型在预测失效方面表现出色,但从保险公司的角度来看,预测哪些投保人可能失效还不足以设计保留策略。在我们的论文中,我们定义了一个失效管理框架,并基于客户生命周期价值和盈利能力定义了一个适当的验证度量。我们通过参数模型和基于树的模型中的竞争风险考虑将死亡风险纳入研究,并表明现有方法的进一步个性化可以提高性能。我们表明,基于生存树的模型优于参数方法,精算文献可以显著受益于它们。然后,我们比较了真实数据,该框架如何导致人寿保险公司的预测收益增加,并讨论了我们的模型在商业和战略决策方面的好处。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Including individual customer lifetime value and competing risks in tree-based lapse management strategies

A retention strategy based on an enlightened lapse model is a powerful profitability lever for a life insurer. Some machine learning models are excellent at predicting lapse, but from the insurer’s perspective, predicting which policyholder is likely to lapse is not enough to design a retention strategy. In our paper, we define a lapse management framework with an appropriate validation metric based on Customer Lifetime Value and profitability. We include the risk of death in the study through competing risks considerations in parametric and tree-based models and show that further individualization of the existing approaches leads to increased performance. We show that survival tree-based models outperform parametric approaches and that the actuarial literature can significantly benefit from them. Then, we compare, on real data, how this framework leads to increased predicted gains for a life insurer and discuss the benefits of our model in terms of commercial and strategic decision-making.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

European Actuarial Journal

BUSINESS, FINANCE-

CiteScore

2.30

自引率

8.30%

发文量

35

期刊介绍:

Actuarial science and actuarial finance deal with the study, modeling and managing of insurance and related financial risks for which stochastic models and statistical methods are available. Topics include classical actuarial mathematics such as life and non-life insurance, pension funds, reinsurance, and also more recent areas of interest such as risk management, asset-and-liability management, solvency, catastrophe modeling, systematic changes in risk parameters, longevity, etc. EAJ is designed for the promotion and development of actuarial science and actuarial finance. For this, we publish original actuarial research papers, either theoretical or applied, with innovative applications, as well as case studies on the evaluation and implementation of new mathematical methods in insurance and actuarial finance. We also welcome survey papers on topics of recent interest in the field. EAJ is the successor of six national actuarial journals, and particularly focuses on links between actuarial theory and practice. In order to serve as a platform for this exchange, we also welcome discussions (typically from practitioners, with a length of 1-3 pages) on published papers that highlight the application aspects of the discussed paper. Such discussions can also suggest modifications of the studied problem which are of particular interest to actuarial practice. Thus, they can serve as motivation for further studies.Finally, EAJ now also publishes ‘Letters’, which are short papers (up to 5 pages) that have academic and/or practical relevance and consist of e.g. an interesting idea, insight, clarification or observation of a cross-connection that deserves publication, but is shorter than a usual research article. A detailed description or proposition of a new relevant research question, short but curious mathematical results that deserve the attention of the actuarial community as well as novel applications of mathematical and actuarial concepts are equally welcome. Letter submissions will be reviewed within 6 weeks, so that they provide an opportunity to get good and pertinent ideas published quickly, while the same refereeing standards as for other submissions apply. Both academics and practitioners are encouraged to contribute to this new format. Authors are invited to submit their papers online via http://euaj.edmgr.com.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: