Lorella Fatone, Francesca Mariani, Francesco Zirilli

{"title":"在 \"现实世界 \"中校准部分指定的随机波动模型","authors":"Lorella Fatone, Francesca Mariani, Francesco Zirilli","doi":"10.1002/fut.22461","DOIUrl":null,"url":null,"abstract":"<p>We study the “real world” calibration of a partially specified stochastic volatility model, where the analytic expressions of the asset price drift rate and of the stochastic variance drift are not specified. The model is calibrated matching the observed asset log returns and the priors assigned by the investor. No option price data are used in the calibration. The priors chosen for the asset price drift rate and for the stochastic variance drift are those suggested by the Heston model. For this reason, the model presented can be considered as an “enhanced” Heston model. The calibration problem is formulated as a stochastic optimal control problem and solved using the dynamic programming principle. The model presented and the Heston model are calibrated using synthetic and Standard & Poor 500 (S&P500) data. The calibrated models are used to produce 6, 12, and 24 months in the future synthetic and S&P500 forecasts.</p>","PeriodicalId":15863,"journal":{"name":"Journal of Futures Markets","volume":"44 1","pages":"75-102"},"PeriodicalIF":1.8000,"publicationDate":"2023-10-03","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22461","citationCount":"0","resultStr":"{\"title\":\"Calibration in the “real world” of a partially specified stochastic volatility model\",\"authors\":\"Lorella Fatone, Francesca Mariani, Francesco Zirilli\",\"doi\":\"10.1002/fut.22461\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We study the “real world” calibration of a partially specified stochastic volatility model, where the analytic expressions of the asset price drift rate and of the stochastic variance drift are not specified. The model is calibrated matching the observed asset log returns and the priors assigned by the investor. No option price data are used in the calibration. The priors chosen for the asset price drift rate and for the stochastic variance drift are those suggested by the Heston model. For this reason, the model presented can be considered as an “enhanced” Heston model. The calibration problem is formulated as a stochastic optimal control problem and solved using the dynamic programming principle. The model presented and the Heston model are calibrated using synthetic and Standard & Poor 500 (S&P500) data. The calibrated models are used to produce 6, 12, and 24 months in the future synthetic and S&P500 forecasts.</p>\",\"PeriodicalId\":15863,\"journal\":{\"name\":\"Journal of Futures Markets\",\"volume\":\"44 1\",\"pages\":\"75-102\"},\"PeriodicalIF\":1.8000,\"publicationDate\":\"2023-10-03\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22461\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Futures Markets\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/fut.22461\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Futures Markets","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/fut.22461","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Calibration in the “real world” of a partially specified stochastic volatility model

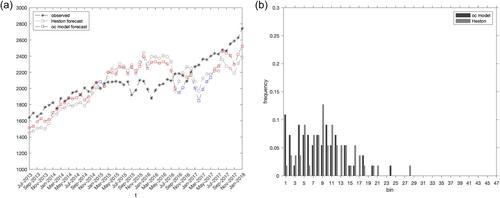

We study the “real world” calibration of a partially specified stochastic volatility model, where the analytic expressions of the asset price drift rate and of the stochastic variance drift are not specified. The model is calibrated matching the observed asset log returns and the priors assigned by the investor. No option price data are used in the calibration. The priors chosen for the asset price drift rate and for the stochastic variance drift are those suggested by the Heston model. For this reason, the model presented can be considered as an “enhanced” Heston model. The calibration problem is formulated as a stochastic optimal control problem and solved using the dynamic programming principle. The model presented and the Heston model are calibrated using synthetic and Standard & Poor 500 (S&P500) data. The calibrated models are used to produce 6, 12, and 24 months in the future synthetic and S&P500 forecasts.

期刊介绍:

The Journal of Futures Markets chronicles the latest developments in financial futures and derivatives. It publishes timely, innovative articles written by leading finance academics and professionals. Coverage ranges from the highly practical to theoretical topics that include futures, derivatives, risk management and control, financial engineering, new financial instruments, hedging strategies, analysis of trading systems, legal, accounting, and regulatory issues, and portfolio optimization. This publication contains the very latest research from the top experts.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: