基于加权条件高矩的时间序列模糊聚类

IF 1.4

4区 数学

Q3 STATISTICS & PROBABILITY

引用次数: 0

摘要

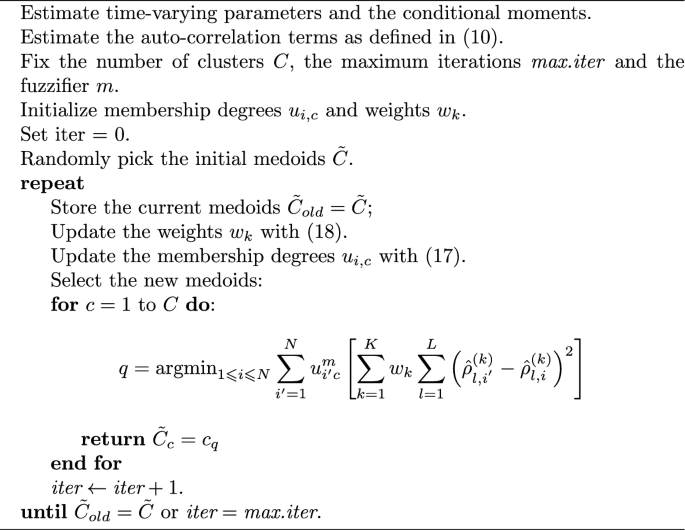

摘要提出了一种基于条件高阶矩不相似性的时间序列模糊聚类方法。在定义聚类时,权重系统说明了每个条件时刻的相关性。通过使用在条件高矩上定义的距离度量的适当指数变换扩展上述聚类方法,还考虑了对异常值的鲁棒性。为了证明所提出方法的有效性,我们对FTSEMIB 30指数中包含的股票时间序列进行了模拟数据研究和实证应用。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Fuzzy clustering of time series based on weighted conditional higher moments

Abstract This paper proposes a new approach to fuzzy clustering of time series based on the dissimilarity among conditional higher moments. A system of weights accounts for the relevance of each conditional moment in defining the clusters. Robustness against outliers is also considered by extending the above clustering method using a suitable exponential transformation of the distance measure defined on the conditional higher moments. To show the usefulness of the proposed approach, we provide a study with simulated data and an empirical application to the time series of stocks included in the FTSEMIB 30 Index.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Computational Statistics

数学-统计学与概率论

CiteScore

2.90

自引率

0.00%

发文量

122

审稿时长

>12 weeks

期刊介绍:

Computational Statistics (CompStat) is an international journal which promotes the publication of applications and methodological research in the field of Computational Statistics. The focus of papers in CompStat is on the contribution to and influence of computing on statistics and vice versa. The journal provides a forum for computer scientists, mathematicians, and statisticians in a variety of fields of statistics such as biometrics, econometrics, data analysis, graphics, simulation, algorithms, knowledge based systems, and Bayesian computing. CompStat publishes hardware, software plus package reports.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: