基于神经网络的广义线性模型交互变量检测

IF 1.6

Q4 BUSINESS, FINANCE

引用次数: 0

摘要

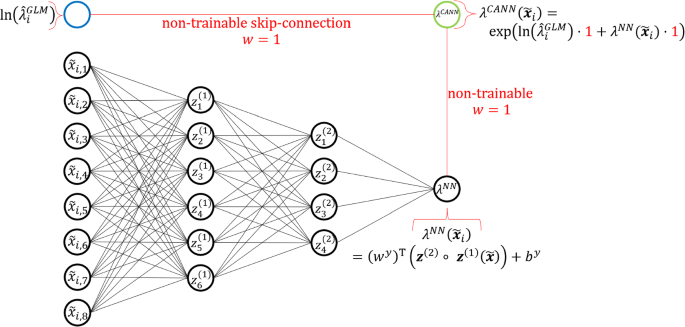

保险公司经常使用的广义线性模型(GLMs)的质量取决于相互作用变量的选择。寻找相互作用非常耗时,特别是对于具有大量变量的数据集,这在很大程度上取决于精算师的专家判断,并且通常依赖于视觉性能指标。因此,我们提出了一种方法来自动化寻找应该添加到glm中的交互过程,以提高其预测能力。我们的方法依赖于神经网络和特定模型的交互检测方法,该方法的计算速度比传统方法(如Friedman的H-Statistic或SHAP值)快。在数值研究中,我们对人工生成的数据和开源数据提供了我们的方法的结果。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Detection of interacting variables for generalized linear models via neural networks

Abstract The quality of generalized linear models (GLMs), frequently used by insurance companies, depends on the choice of interacting variables. The search for interactions is time-consuming, especially for data sets with a large number of variables, depends much on expert judgement of actuaries, and often relies on visual performance indicators. Therefore, we present an approach to automating the process of finding interactions that should be added to GLMs to improve their predictive power. Our approach relies on neural networks and a model-specific interaction detection method, which is computationally faster than the traditionally used methods like Friedman’s H-Statistic or SHAP values. In numerical studies, we provide the results of our approach on artificially generated data as well as open-source data.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

European Actuarial Journal

BUSINESS, FINANCE-

CiteScore

2.30

自引率

8.30%

发文量

35

期刊介绍:

Actuarial science and actuarial finance deal with the study, modeling and managing of insurance and related financial risks for which stochastic models and statistical methods are available. Topics include classical actuarial mathematics such as life and non-life insurance, pension funds, reinsurance, and also more recent areas of interest such as risk management, asset-and-liability management, solvency, catastrophe modeling, systematic changes in risk parameters, longevity, etc. EAJ is designed for the promotion and development of actuarial science and actuarial finance. For this, we publish original actuarial research papers, either theoretical or applied, with innovative applications, as well as case studies on the evaluation and implementation of new mathematical methods in insurance and actuarial finance. We also welcome survey papers on topics of recent interest in the field. EAJ is the successor of six national actuarial journals, and particularly focuses on links between actuarial theory and practice. In order to serve as a platform for this exchange, we also welcome discussions (typically from practitioners, with a length of 1-3 pages) on published papers that highlight the application aspects of the discussed paper. Such discussions can also suggest modifications of the studied problem which are of particular interest to actuarial practice. Thus, they can serve as motivation for further studies.Finally, EAJ now also publishes ‘Letters’, which are short papers (up to 5 pages) that have academic and/or practical relevance and consist of e.g. an interesting idea, insight, clarification or observation of a cross-connection that deserves publication, but is shorter than a usual research article. A detailed description or proposition of a new relevant research question, short but curious mathematical results that deserve the attention of the actuarial community as well as novel applications of mathematical and actuarial concepts are equally welcome. Letter submissions will be reviewed within 6 weeks, so that they provide an opportunity to get good and pertinent ideas published quickly, while the same refereeing standards as for other submissions apply. Both academics and practitioners are encouraged to contribute to this new format. Authors are invited to submit their papers online via http://euaj.edmgr.com.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: