{"title":"序列依赖下的多变化点检测:野性对比度最大化和加普-施瓦茨算法","authors":"Haeran Cho, Piotr Fryzlewicz","doi":"10.1111/jtsa.12722","DOIUrl":null,"url":null,"abstract":"<p>We propose a methodology for detecting multiple change points in the mean of an otherwise stationary, autocorrelated, linear time series. It combines solution path generation based on the wild contrast maximisation principle, and an information criterion-based model selection strategy termed gappy Schwarz algorithm. The former is well-suited to separating shifts in the mean from fluctuations due to serial correlations, while the latter simultaneously estimates the dependence structure and the number of change points without performing the difficult task of estimating the level of the noise as quantified e.g. by the long-run variance. We provide modular investigation into their theoretical properties and show that the combined methodology, named WCM.gSa, achieves consistency in estimating both the total number and the locations of the change points. The good performance of WCM.gSa is demonstrated via extensive simulation studies, and we further illustrate its usefulness by applying the methodology to London air quality data.</p>","PeriodicalId":49973,"journal":{"name":"Journal of Time Series Analysis","volume":"45 3","pages":"479-494"},"PeriodicalIF":1.0000,"publicationDate":"2023-09-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jtsa.12722","citationCount":"0","resultStr":"{\"title\":\"Multiple change point detection under serial dependence: Wild contrast maximisation and gappy Schwarz algorithm\",\"authors\":\"Haeran Cho, Piotr Fryzlewicz\",\"doi\":\"10.1111/jtsa.12722\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We propose a methodology for detecting multiple change points in the mean of an otherwise stationary, autocorrelated, linear time series. It combines solution path generation based on the wild contrast maximisation principle, and an information criterion-based model selection strategy termed gappy Schwarz algorithm. The former is well-suited to separating shifts in the mean from fluctuations due to serial correlations, while the latter simultaneously estimates the dependence structure and the number of change points without performing the difficult task of estimating the level of the noise as quantified e.g. by the long-run variance. We provide modular investigation into their theoretical properties and show that the combined methodology, named WCM.gSa, achieves consistency in estimating both the total number and the locations of the change points. The good performance of WCM.gSa is demonstrated via extensive simulation studies, and we further illustrate its usefulness by applying the methodology to London air quality data.</p>\",\"PeriodicalId\":49973,\"journal\":{\"name\":\"Journal of Time Series Analysis\",\"volume\":\"45 3\",\"pages\":\"479-494\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2023-09-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jtsa.12722\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Time Series Analysis\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jtsa.12722\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Time Series Analysis","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jtsa.12722","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

Multiple change point detection under serial dependence: Wild contrast maximisation and gappy Schwarz algorithm

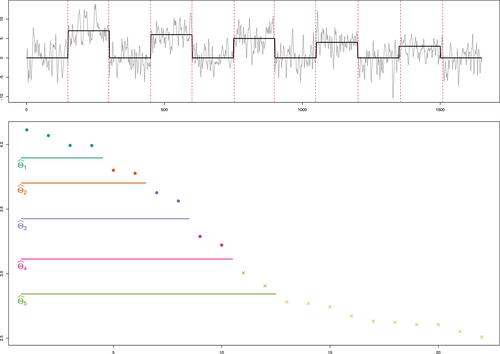

We propose a methodology for detecting multiple change points in the mean of an otherwise stationary, autocorrelated, linear time series. It combines solution path generation based on the wild contrast maximisation principle, and an information criterion-based model selection strategy termed gappy Schwarz algorithm. The former is well-suited to separating shifts in the mean from fluctuations due to serial correlations, while the latter simultaneously estimates the dependence structure and the number of change points without performing the difficult task of estimating the level of the noise as quantified e.g. by the long-run variance. We provide modular investigation into their theoretical properties and show that the combined methodology, named WCM.gSa, achieves consistency in estimating both the total number and the locations of the change points. The good performance of WCM.gSa is demonstrated via extensive simulation studies, and we further illustrate its usefulness by applying the methodology to London air quality data.

期刊介绍:

During the last 30 years Time Series Analysis has become one of the most important and widely used branches of Mathematical Statistics. Its fields of application range from neurophysiology to astrophysics and it covers such well-known areas as economic forecasting, study of biological data, control systems, signal processing and communications and vibrations engineering.

The Journal of Time Series Analysis started in 1980, has since become the leading journal in its field, publishing papers on both fundamental theory and applications, as well as review papers dealing with recent advances in major areas of the subject and short communications on theoretical developments. The editorial board consists of many of the world''s leading experts in Time Series Analysis.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: